Market Recap – Week ending Dec. 9

Stocks in U.S. Lower Last Week; Fed Meeting Dec. 13-14

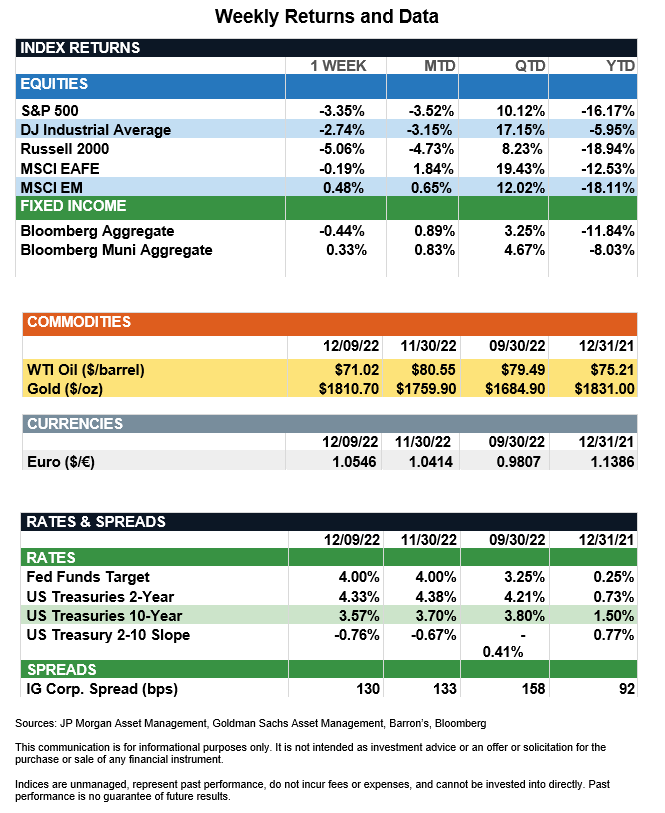

Overview: Stock markets in the U.S. ended broadly lower last week as investors look forward to the last Federal Reserve meeting of 2022 on this week (Dec. 13-14) of this week. The Fed is widely expected to slow the pace of rate hikes to 0.50% at the meeting (see details below). Concerns over the need for continued monetary policy tightening to fight inflation and recession fears weighed on the markets with the S&P 500 index down 3.4% for the week. International stocks fared better, led by emerging markets (MSCI EM), up 0.50% over the past week. The MSCI EM index was buoyed by a 6.6% return in China’s Hang Seng Index as the country continues its path toward economic reopening. In bonds, yields rose as a stronger-than-expected producer prices (PPI) report fueled worries inflation is not slowing as much as expected. Headline PPI fell from 8.0% to 7.4% for November, but the reading was above the 7.2% consensus for the month. The 2-year and 10-year Treasury notes finished the week at a yield of 4.33% and 3.57%, respectively. This week, the focus will be on the consumer price (CPI) report due out Tuesday, Dec. 13, where headline CPI is expected to fall year-over-year from 7.7% in October to 7.3% in November.

Update on Inflation and the Fed (from JP Morgan): While the labor market typically is the last to turn in an economic cycle, we expect data soon will reflect this softness and signal further moderation in services inflation. This week, investors will gain further clarity on whether the recent inflation downtrend is sticking and the Fed’s timing on a policy pivot. The November CPI report will be out on Tuesday and market expectations are for a 0.3% increase in both the headline and core measures, which would bring the year-over-year inflation rates to 7.3% and 6.1%, respectively. We expect core goods inflation will continue its decline given further contraction in the Manheim used vehicle index, softening consumer spending on durable goods, easing supply-chain constraints and retail discounting during the holiday season. Lower gas and oil prices also will help drive moderation in the headline measure. However, Federal Reserve Chair Jerome Powell has highlighted services inflation excluding rent as a key inflation measure for the Fed. While this measure turned negative in October, breaking a long streak of monthly increases, its pathway to normalization will be primarily determined by labor market dynamics. The November jobs report showed a mixed picture of labor market tightness, with hotter-than-expected wages but weakness in the household survey. However, other high-frequency data suggest the labor market is still cooling, with initial jobless claims and layoff announcements rising in recent weeks. On Wednesday, the Federal Reserve will conclude its last meeting of the year and we expect they still will slow their pace of rate hikes to 50bps. While they likely will maintain higher-for-longer policy messaging, economic normalization and receding inflation pressures should allow them to pause their tightening program in the first quarter.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.