News

Avantax adds $250M married duo from Edward Jones

The Lockhart, Texas-based advisor couple join the tax-focused wealth planning network with years of experience at a family-owned practice.

Read More

Avantax Welcomes Financial Advisors Heidi and Nicholas Irwin, Longtime Fixtures of the Lockhart, Texas, Community

Having been part of a family-owned business for many years, personal relationships are key to Heidi and Nic, and they said they’ve seen that reflected in the culture of the Avantax Community.

Read More

Avantax president accounts for a brand-new era

While the firm is best known for its tax expertise, Todd Mackay is talking about relationships and creating connections.

Read More

AdvisorHub Q&A: Avantax’s Emily Millsap, CFP®

AdvisorHub asked executives from top firms their thoughts on the wealth management industry. Here is how Emily Millsap CFP®, Manager, Financial Planning at Avantax Wealth Management responded.

Read More

Advisors, don’t overlook these items during tax season

The Tax Relief for American Families and Workers Act has been slowly moving through Congress, and there’s confusion whether it’s better to file now or wait. Some taxpayers will be significantly impacted by this legislation, and the longer we wait, the more compressed tax season becomes.

Read More

Taxes + wealth: 2 connected but still (for now) distinct fields are merging

"It really begins at identifying the needs of the client," Mackay said. "That's when you get truly comprehensive, tax-intelligent financial planning is when you're looking at it through the entire lifecycle and journey of a client. And that's really what Avantax Financial Professionals do best."

Read More

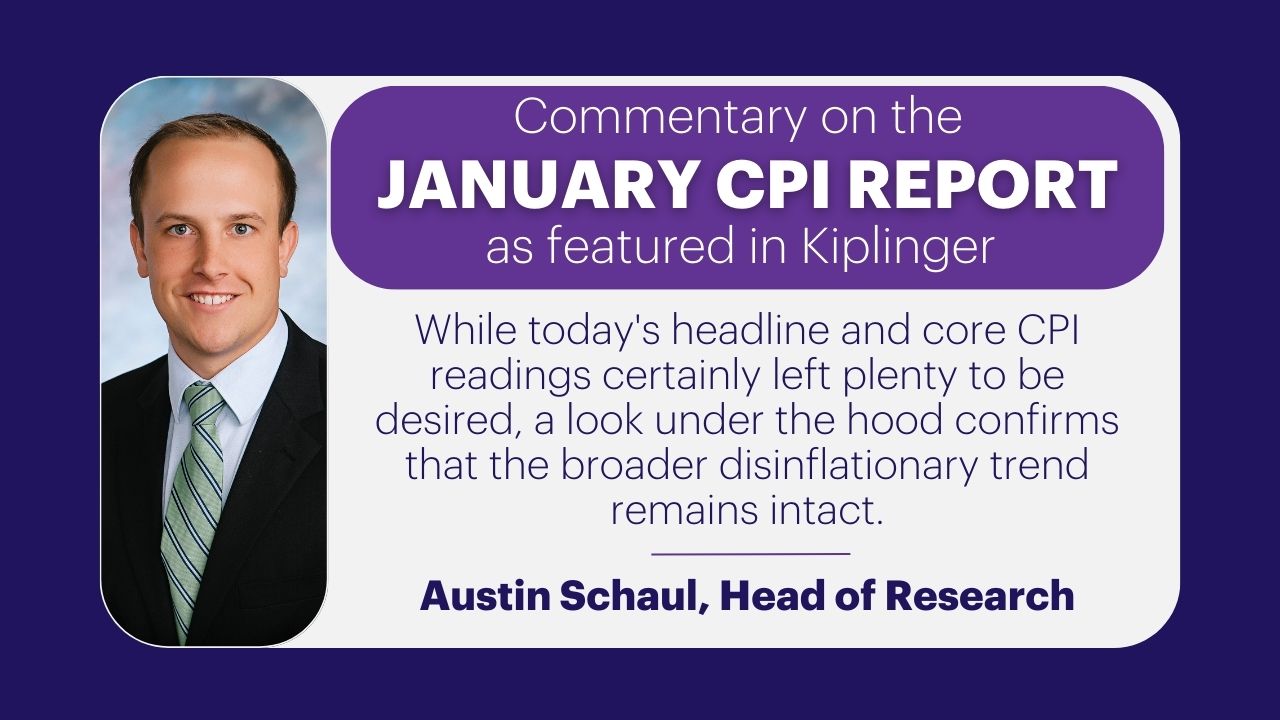

January CPI Report: What the Experts Are Saying About Inflation

Inflation came in a little bit hotter than expected last month, the January Consumer Price Index (CPI) report revealed Tuesday, all but ensuring that the Federal Reserve won't enact as many interest rate cuts this year as the market had hoped.

Read More

December CPI Report: What the Experts Are Saying About Inflation

With the December CPI report now a matter of record, we turned to economists, strategists and other experts for their thoughts on what the data means for markets, macroeconomics and monetary policy going forward.

Read More

New Year’s Resolutions Financial Advisors Wish Clients Would Make

What if advisors could create New Year’s resolutions for their clients? Avantax's Emily Millsap explores the impact of emotions on the financial decisions we make.

Read More

Avantax Brand Isn't Going Anywhere: Cetera's Durbin

Now that Cetera Financial Group has completed its $1.2 billion acquisition of tax-focused Avantax, what’s next? Assimilation. But not integration.

Read More

Avantax Welcomes Stephen Whyte and his Four-Generation Tax and Wealth Management Firm with Over $100 Million in Total Client Assets

Tax-focused Financial Professional transferred from Crown Capital Securities to leverage Avantax’s tax-intelligent tools, technology and Home Office’s 40 years of experience supporting tax professionals

Read More

Jobs Growth Beats Expectations in November: What the Experts Are Saying

A better-than-expected November jobs report appears to keep the economy on path for a so-called soft landing, experts say, but also lowers the odds that the central bank will start cutting rates in the first quarter of 2024.

Read More

Tax-Efficient Charitable Giving Strategies For Year-End Planning

Advisors Can Support Clients’ Holiday Charitable Giving With Innovative Tax Strategies That Maximize Gift Values, Reduce Taxes And More

Read More

Cetera Holdings Announces Close of Avantax Acquisition

Avantax to operate as a unique community within Cetera Holdings, bringing more than 3,100 financial professionals and over $82 billion in assets to Cetera

Read More

Avantax Welcomes Financial Advisors Joshua Heims and Alan Gnoinski with Nearly $100 Million in Total Client Assets

Focused on growth and expanding partnerships with tax professionals, Heims and Gnoinski bring their New York-based Lincoln Sparrow Advisors team to Avantax from SagePoint Financial

Read More

Avantax Hosts its Largest-Ever National Conference as Attendees Gather in Chicago, Showcasing the Peer-to-Peer Power of the Avantax Community

The event’s “Profound Approach, Enduring Impact” theme reflects how independent Avantax Financial Professionals’ tax-intelligent approach to financial planning changes clients’ lives.

Read More

October CPI Report: What the Experts Are Saying About Inflation

Inflation slowed markedly last month on both a headline and underlying basis, the October Consumer Price Index (CPI) showed Tuesday, giving support to the view that the Federal Reserve is done hiking interest rates this cycle, experts say.

Read More

Avantax Posts Record Newly Recruited Assets as Advisor Appetite for Joining the Tax-Focused Avantax Community Keeps Growing

Nearly $564 million in third quarter newly recruited assets more than doubles the year-ago quarter.

Read More

Jobs Growth Slowed Sharply in October: What the Experts Are Saying

A soft October jobs report gives the Federal Reserve cover to keep interest rates unchanged at the next Fed meeting, experts say. Just remember that the "data dependent" central bank will see one more jobs report – and two inflation readings – before it convenes for the last time in 2023, they add.

Read More

Bond Market Experts Offer Road Map for What Lies Ahead

To help gauge the level of risk and opportunities spreading across the fixed-income markets, etf.com gathered perspectives from seven bond market professionals on what the near-term future looks like for investors.

Read More

Financial Advisor Aaron Watson Returns to Avantax, Joined by Public Accounting Partner Lee MacBay Hamilton & Associates, LLC

One year after transferring to Cambridge Investment Research, Inc., Watson rejoins Avantax to regain the benefits of its tax-centric platform, technology and Home Office

Read More

Avantax Welcomes Financial Advisor Bob Ervolina and his New York-based Lifetime Wealth Management Group

25-year industry veteran advisor attracted by close-knit Avantax Community, ease of doing business, and opportunities to partner with CPAs in the Avantax network.

Read More

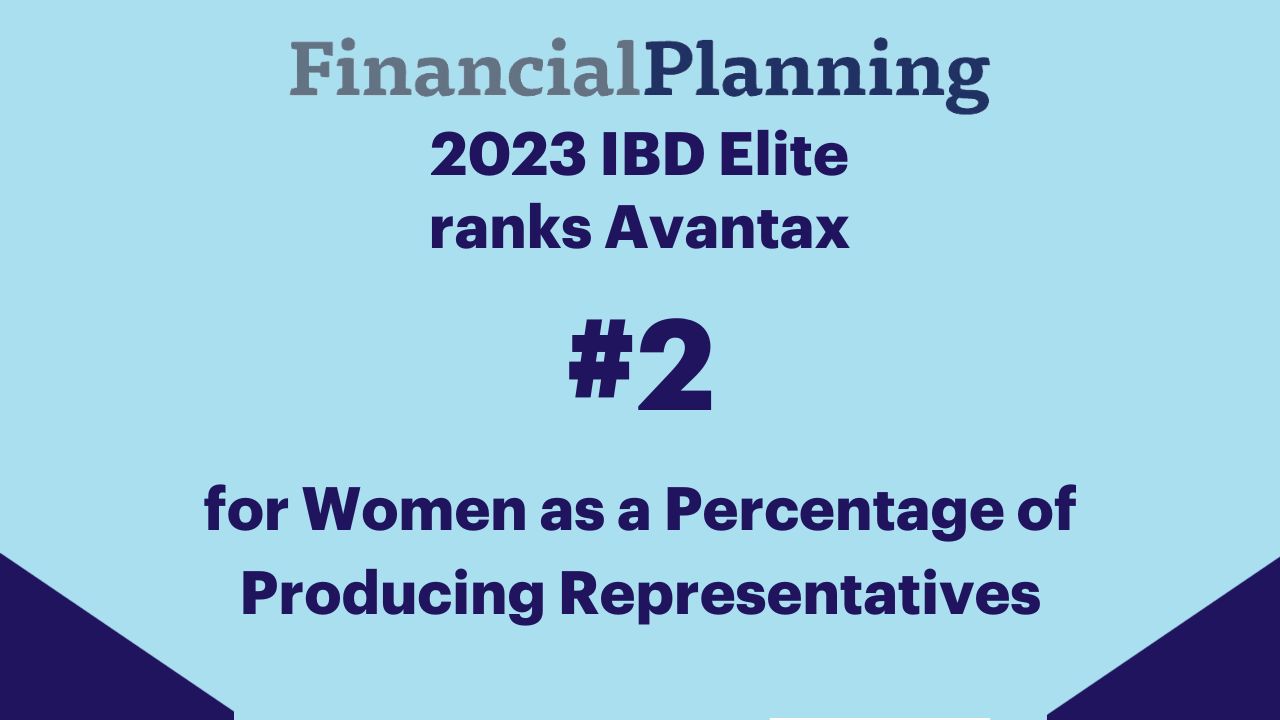

IBD Elite 2023: The 10 firms with the largest percentage of women among their financial advisors

In wealth management, the act of simply disclosing the number of women who are financial advisors within a firm represents differentiation from the competition.

Read MoreAvantax Has Second-Highest Ratio of Women Advisors Among Broker-Dealers in Financial Planning’s IBD Elite 2023 Study

Avantax’s ratio of women Financial Professionals also compares favorably to the industry average of 18%.

Read More

IBD Elite: The 15 largest independent brokerages in wealth management

The independent brokerages participating in Financial Planning's 38th annual IBD Elite study reported that their businesses grew 6% in 2022 to a combined $41.13 billion in revenue.

Read More

Avantax Enters into Definitive Agreement to be Acquired by Cetera Holdings

Avantax Financial Professionals and Accounting Firms to Expand and Enhance Cetera’s Wealth Management Group Ecosystem

Read More

Avantax Adds Burbank Octet with $230M in Assets

Avantax added an eight-person team in Burbank, Calif., with more than $230 million in client assets.

Read More

Avantax Welcomes Anna Luke and Her Comprehensive Financial Services Team with over $230 Million in Total Client Assets

30-year-old, California-based wealth management firm attracted by opportunities to partner with CPAs across the Avantax Community to deliver unified services to clients.

Read More

RIA Roundup: Avantax Adds Two Firms, $450M in Assets

Avantax, a publicly traded, tax-focused wealth management firm with more than $83 billion in client assets, added two firms this week, totally approximately $450 million in brokerage and advisory assets.

Read More

Boost your tax practice's bottom line with a wealth manager

The process may seem too daunting, but by combining their expertise and embracing a holistic approach, tax professionals and financial advisors have the opportunity to enhance their services, boost their respective practices' profitability and further deepen the tax professional's client relationships.

Read More

Avantax Adds $330M Wealth Management Firm

Summit Wealth Advocates, founded in 2010 by Bruce Primeau and managing about $330 million in total client assets as of the end of June, has joined Avantax.

Read More

Avantax Welcomes CFR Capital with $120 Million in Total Client Assets

Scottsdale-based firm attracted by Avantax’s technology, tax-focus and collaborative community.

Read More

Avantax Named Finalist in Service Excellence Category at the 2023 WealthManagement.com “Wealthies” Industry Awards

Firm's proactive service journey and subsequent results earn nod from notable industry awards.

Read More

Avantax Acquires Summit Wealth Advocates Adding 7-person Team and $330 Million in Total Client Assets to Avantax’s Employee-based Model

Avantax® has acquired Summit Wealth Advocates (Summit), a Minnesota-based wealth management firm with approximately $330 million in total client assets as of June 30, 2023.

Read More

Avantax Recruiting Outlook Remains Strong as Tax and Financial Professionals Seek Faster Growth and Superior Service

More than 100 independent Financial Professionals have joined Avantax this year through the second quarter as they seek better support, resources and more collaboration on tax-intelligent planning.

Read More

July CPI Report: What the Experts Are Saying About Inflation

With the July CPI report now in the books, we turned to economists, strategists, investment officers and other experts to get their takes on what the inflation data means for markets, macroeconomics and monetary policy going forward.

Read More

10 Long-Term Investing Strategies That Work

U.S. News asked experts to weigh in on some of the soundest investing strategies to use throughout your life. Here's a look at 10 of the best long-term investment strategies.

Read More

Avantax Earns 2023 Great Place to Work Certification

Avantax®, a leader in tax-focused financial planning and wealth management, announced it has earned the Great Place to Work certification.

Read More

Avantax Promotes Jennifer Hutchins to Co-Chief Investment Officer

Hutchins and Co-CIO Ivan Gruhl will further enhance impact of research and investment management for Avantax’s independent Financial Professionals and accounting firms.

Read More

Avantax Expands Business Development Team with Veteran Financial Services Recruiters, each with More than 30 Years of Experience

Bruce Tuckey and Dave Renko bring decades of experience to their roles at Avantax and will help expand the Avantax Community of accounting firms and tax-focused Financial Professionals.

Read More

Avantax Reports Robust Recruiting Pipeline as Prospects Continue to See Tax-Advantaged Wealth Management as a Preferred Growth Pathway

Avantax reports more than $228 million in newly recruited assets during 2023’s first quarter with continued interest from growth-minded independent financial professionals and accounting firms.

Read More

Avantax Welcomes Walter Pardo and His New Jersey-based Wealth Financial Partners Team

A successful and growth-minded financial advisor, Pardo chose Avantax for its tax-focused approach to wealth management, specialized Home Office support teams, and deep network of CPAs and tax professionals

Read More

Avantax Launches its Women’s Advisor Forum to Further Empower Female Financial Professionals

Growth-minded Financial Professionals want the competitive advantage of Avantax’s tax-focused wealth management, service excellence and close-knit Avantax community of like-minded Financial Professionals

Read More

Broker/Dealers Must Optimize for Service to Move Past Stagnation

Let’s be blunt. Broker/dealers aren’t the darlings of the wealth management industry they once were, having struggled to adapt to external forces and the onset of discount brokerages that have made investing accessible for millions.

Read More

Avantax Sets Record with Approximately $1.7 Billion in Full-Year 2022 Newly Recruited Assets, up Approximately 79% from the Prior Year

Avantax continued its record-breaking recruiting results during the fourth quarter of 2022, contributing to full-year 2022 newly recruited assets of approximately $1.7 billion, an increase of approximately 79% over 2021.

Read More

Retirement Roundtable – Growth Opportunities With SECURE 2.0

News of the many changes in the SECURE 2.0 Act, signed by President Biden on Dec. 29, 2022, has circulated to every corner of America’s financial world.

Read More

Avantax Appoints Melissa Loner as Chief Compliance Officer

“I am pleased to welcome Melissa who joins an energized Avantax leadership team committed to creating value for our Financial Professionals, CPA firms, Home Office staff, and investors,” said Chris Walters, CEO of Avantax, Inc.

Read More

Q&A with AdvisorHub CEO Tony Sirianni and Avantax Wealth Management’s President, Todd Mackay

We ask a series of top Wealth Management CEOs the same set of questions and let you, our audience, get a sense of how different leaders address the same challenges, and try to get a glimpse into their unique world view.

Read More

What To Do When Your Client Is Retiring In 2023

As we turn the page into a new year, we talk about resolutions, plans and strategies for making 2023 the year we finally achieve a long-standing dream or goal, and for many, that goal is retirement.

Read More

It's Time to Counsel Clients on Critical Year-end Tax Considerations

It's time to schedule year-end tax conversations with clients — before the coming holidays consume their schedules and yours.

Read More

Avantax Wealth Management Hosts 1,100 Affiliates, Educational Partners and Home Office Staff at National Conference in Atlanta

“Power of Community” themed event showcases success of the Avantax Community, and the company’s focus on helping Financial Professionals grow their businesses

Read More

20 Acquisitions in 20 Months Fuel Significant Growth of Avantax’s Employee-Based RIA Model

A series of acquisitions has helped the Avantax® employee-based model to significantly grow total client assets and its geographic footprint.

Read More

Avantax Attracted 74 Indie Advisers in Third Quarter

Seventy-four financial professionals switched their broker-dealer affiliation to Avantax in the third quarter, the Dallas-based wealth management firm said.

Read More

Avantax Recruiting Success Continues During Third Quarter, Driving Year-to-Date Newly Recruited Assets to Approximately $1.3 Billion

Financial Professionals transferring to Avantax to access its deep network of CPAs and tax pros; recruits also looking to leverage Avantax’s tax-smart investing tools to better serve clients

Read MorePublic Accounting Firm Topel Forman Affiliates with Avantax Planning Partners for Wealth Management and Financial Planning Services

120-person firm chooses Avantax for its proven model, successful track record partnering with accounting firms

Read More

Avantax President Todd Mackay Joins Jay Coulter on “The Resilient Advisor Show”

Todd Mackay, President of Avantax Wealth Management, discusses why tax-centric financial advisors are uniquely positioned amid market volatility.

Read MoreAvantax Reports Newly Recruited Total Client Assets Exceeding $1 Billion During First Half of 2022, Surpassing the Firm’s Full-Year 2021 Results

Growth-minded Financial Professionals want the competitive advantage of Avantax’s tax-focused wealth management, service excellence and close-knit Avantax community of like-minded Financial Professionals

Read MoreVeteran Financial Advisor Jeffrey Steinberg Joins Avantax’s Employee-based RIA, Expanding Avantax RIA Footprint to Florida

20-year financial services veteran leverages flexible Avantax affiliation models to create a future focused on consistent client service and growth opportunities

Read MoreAvantax Planning Partners Recognizes Affiliate Accomplishments During National Conference

Annual Elevate Conference showcases highest performing individuals and firms

Read MoreAvantax Planning Partners Recognizes Affiliate Accomplishments During Largest-ever National Conference

Avantax Planning Partners Recognizes Affiliate Accomplishments During Largest-ever National Conference. Annual Elevate Conference showcases high-performance individuals and firms.

Read MoreAvantax Welcomes ATS Advanced Trustee Strategies with Over $400 Million in Total Client Assets

Highly successful veteran advisor Sandeep Varma chooses Avantax to access its vast network of CPAs, tax pros and accounting firms, and for direct access to Avantax senior leadership.

Read MoreAvantax Posts Record-setting Recruiting Results During the First Quarter of 2022 with approximately $529 Million in Recruited Assets

Financial Professionals are transferring to Avantax for better service levels, enhanced technology and products, direct access to senior Avantax leadership, and a strong sense of community.

Read MoreAvantax Adds Veteran Business Development Leader Elvis Medica as Success Grows Recruiting Highly Productive Financial Professionals

Medica’s experience includes leadership roles with Cetera Financial Group, a large LPL-affiliated OSJ, and several other national sales positions for brokerage and mutual fund companies

Read MoreAvantax Welcomes Sullivan Financial Services, Inc., with More Than $200 Million in Total Client Assets

Thomas Sullivan chooses Avantax for its responsiveness, product lineup, and strong network of accounting firms to further enhance growth opportunities in Las Vegas

Read MoreAvantax Acquires Gene Bell & Associates, Expanding Employee-based RIA Footprint to the Northwest

Well-known tax expert and Financial Professional Gene Bell joins Avantax, further strengthening the firm’s value to CPAs and tax pros serving clients at the intersection of tax and financial planning

Read MoreAvantax President Todd Mackay to Open Annual FSI OneVoice Conference

Several Avantax leaders slated as featured speakers on FSI OneVoice panels in Dallas

Read MoreAvantax Works with the SEC to Settle 1st Global Regulatory Matter

Avantax® reported today that it has entered into a settlement with the U.S. Securities and Exchange Commission (SEC) on behalf of 1st Global Advisors, Inc., which was acquired by Avantax’s parent in May 2019.

Read MoreAvantax Acquires Warner Finance, with $258 Million in Client Assets, Further Expanding Northeast Footprint of Avantax’s Employee-based RIA

Avantax®, a leader in tax-focused financial planning, has acquired Pennsylvania-based Warner Finance, with approximately $258 million in total client assets as of Oct. 11, 2021.

Read MoreAvantax Completes Acquisition of Headquarters Advisory Group, LLC

Avantax℠, a leader in tax-focused financial planning, has closed its acquisition of New Jersey-based Headquarters Advisory Group, LLC, with approximately $1.1 billion in total client assets as of June 30, 2021.

Read MoreAvantax Agrees to Acquire Headquarters Advisory Group, LLC, with $1.1 Billion in Client Assets, which would Expand Avantax’s In-house RIA to Northeast

Transaction would enable independent affiliate to monetize its firm, shift administrative tasks to Avantax, and fully focus on growth and superior end-client service

Read MoreAvantax President Todd Mackay to Open FSI OneVoice Conference in Orlando with Other Avantax Leaders Attending as Featured Panelists

FSI annual conference brings together independent financial services firm executives to share critical insights on the most important issues affecting their businesses

Read MoreAvantax Expands Presence at AICPA Engage 2021 to Share How Integrating Financial Planning Services Helps Accounting Firms Drive Growth

From in-person meetings at Booth #225, to hosting a session on developing a business succession plan, Avantax will show how offering holistic financial services enhances accounting firm value

Read MoreAvantax Wealth Management Hosts Nearly 1,000 Affiliates, Partners and Home Office Staff at National Conference in Dallas

In-person meetings, collaboration and celebration of affiliates’ successes launch Avantax and its unique community of Financial Professionals into the second half of 2021 and beyond

Read More