Market Recap – Week Ending April 26

Strong Earnings Push Stocks Higher; Fed Meeting This Week

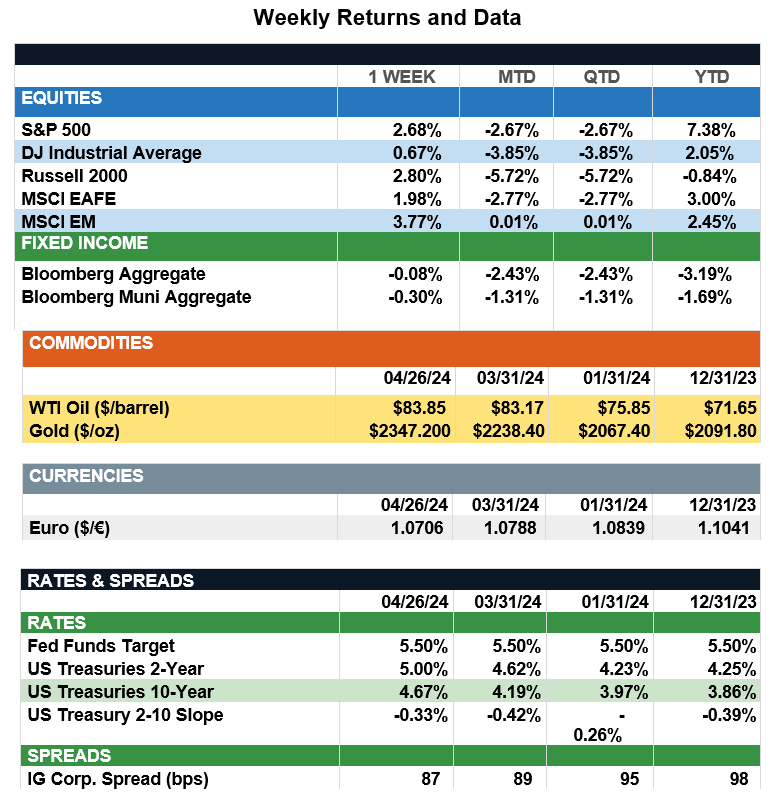

Overview: Stocks rose across the globe last week as strong earnings in the U.S. overcame a slowdown in economic growth in the first quarter. For the week, the S&P 500 index was higher by 2.7%, with international developed stocks (MSCI EAFE) up 2.0%, and emerging markets (MSCI EM) moving higher by 3.8% on the week. In bonds, Treasury yields rose last week as the Federal Reserve’s preferred measure of inflation, core personal consumption (PCE), increased 2.8% year-over-year in March, above expectations. The data reinforced investor concerns that sticky inflation may force the Fed to delay rate cuts this year with Fed Watch data now expecting one or two rate cuts for 2024. The 2-year and 10-year Treasury notes finished the week at yields of 5.00% and 4.67%, respectively, and yields for both notes are now about 75 basis points (0.75%) higher year-to-date. In other economic data, U.S. real Gross Domestic Product (GDP) grew at a 1.6% annualized pace in the first quarter, well below consensus expectations, as the Fed continues to monitor growth and inflation. The Fed will hold their next policy meeting this Tuesday and Wednesday, with the Fed expected to keep interest rates unchanged as investors will follow the news conference following the meeting for any clues to future central bank policy. Away from the Fed meeting this week, corporate earnings will continue to be in focus. The first-quarter earnings season has been strong so far with about 80% of the S&P 500 companies that have reported earnings beating expectations (Factset). In addition, the employment report for March will be released on Friday May 3, with expectation for 230,000 new payroll jobs and unemployment to remain at 3.8%. Included in the jobs report will be a key inflation metric, the average hourly earnings, which is expected to fall from 4.1% to 4.0% on an annualized basis.

Update on Economic Growth (from JP Morgan): Last week's initial estimates of 1Q24 GDP revealed a complex picture. At the start of the year, expectations were set for gradual declines in growth and inflation. However, the data showed a sharp deceleration in headline growth while inflation, as measured by the Personal Consumption Expenditures (PCE) price index, accelerated on a quarter-to-quarter basis. This has raised concerns about potential stagflation and its implications on interest rates and markets. Looking at the details, first-quarter real GDP grew at an annualized rate of 1.6%, roughly half the pace of the previous quarter and below the Fed’s forecasts for 2024 and the longer term. However, volatile components like trade and inventories, which often swing up and down in consecutive quarters, significantly impacted this slowdown. Excluding those components, the economy grew at a healthy 3.1% rate – slightly above last year's average. This growth was supported by a strong labor market, evident from fewer jobless claims, which in turn bolstered consumer spending – rising by 2.5%, nearly aligning with its 20-year trend. This suggests concerns over economic stagnation may be exaggerated, as the headline figure masked the underlying strength. However, while recent reports remain consistent with falling inflation, it has turned into a very slow decline, tempering market expectations for rate cuts this year. The FOMC statement will be pivotal in revealing whether the Fed also is leaning toward reducing its rate-cut projections. Such a shift could pressure the multiple expansion, which fueled much of the equity market gains in the first quarter.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg, Factset, CNBC.

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.