Market Recap – Week Ending April 5

Down Week for Stocks; CPI, PPI Releases This Week

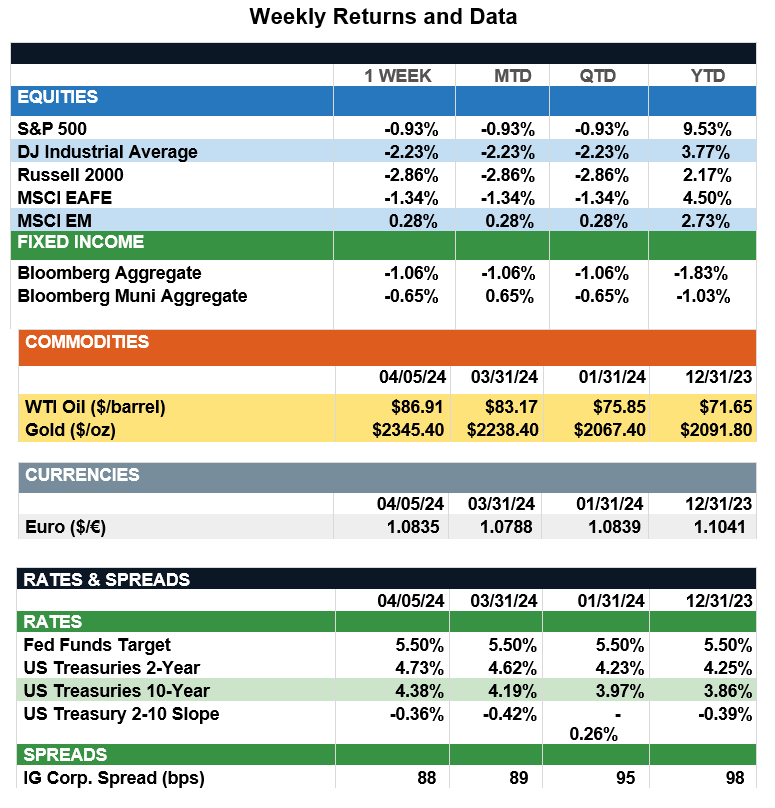

Overview: U.S. stocks began the quarter with negative returns last week as the S&P 500 index recorded its biggest weekly loss since early January, down 0.9%. Despite the down week, the S&P 500 is up about 9.5% year-to-date as the index finished the first quarter with more than a 10% gain, the best first quarter since 2019. Markets ended the week on a positive note, as an above-consensus jobs report on Friday supported hopes for a continuing strong economy and positive corporate earnings growth, even against the backdrop of higher interest rates. In bonds, 2-year and 10-year Treasury yields rose to 4.73% and 4.38%, respectively, on the week, and yields have now risen about 50 basis points (0.50%) across the curve since the beginning of the year. Market participants continue to monitor the expected future course of the funds rate as FedWatch data now shows about a 50/50 chance of a first rate cut in June with 2-3 cuts now expected for the year. In comments last week, Fed Chair Jerome Powell stressed the committee would continue to be dependent on economic data, and needs greater confidence that inflation is coming down to their 2.0% target before taking action on rates. Key inflation data will be released this week with the March consumer (CPI) and producer (PPI) prices due out Wednesday and Thursday, respectively. Core CPI is expected to fall from 3.8% to 3.7% on an annualized basis as investors look for further progress on the inflation front.

Update on Gold Prices (from JP Morgan): Last week, gold prices broke above $2,300 per ounce for the first time. Gold prices have been climbing for a number of reasons, among which might be more hope for a soft landing and upcoming rate cuts in the U.S. This is because the opportunity cost of investing in gold, which is not an income-producing asset, decreases when interest rates fall. Recent dovish messaging from the Fed has increased investor demand for gold ahead of expected rate cuts this summer. Also, gold may be attracting investors concerned about ongoing global conflicts, as it is widely considered a safe-haven asset. Lastly, China’s real estate crisis has pushed more domestic investors toward gold. Should long-term investors buy gold? Over the past 46 years, gold has had worse performance and similar volatility compared to both U.S. and developed market equities. Unlike equities anchored by earnings or bonds that pay coupons, gold and other precious metals are largely determined by speculation on where prices are headed. Therefore, precious metals are inherently a more tactical asset class with limited utility in long-term portfolios. It still is important to understand the driving forces behind gold and other commodity prices to gauge investor sentiment and broader market trends. However, for investors looking to hedge risk and diversify, focusing on quality fixed income, equities and more fundamentally based alternatives may be a better strategy.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg, CNBC

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results. Neither diversification nor asset allocation assure or guarantee better performance and cannot eliminate the risk of investment losses.