Market Recap – Week ending Nov. 11

U.S. Stocks Rally; Inflation Data Below Expectations

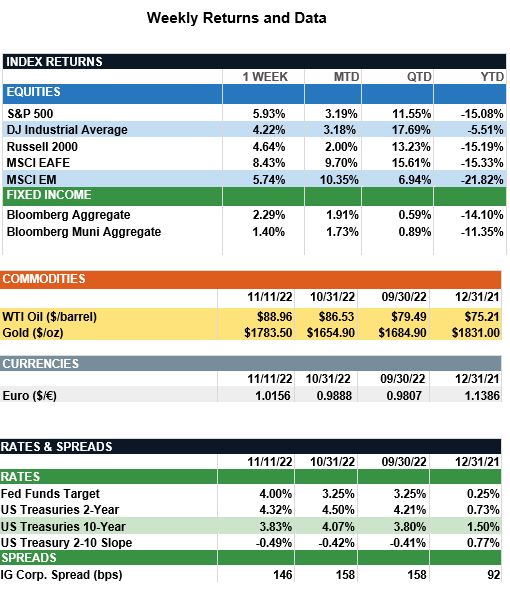

Overview: Stocks around the globe were sharply higher last week after the U.S. October Consumer Price Index (CPI) report showed inflation well below expectations. In the U.S., the S&P 500 rallied 5.93% while international developed stocks (MSCI EAFE) and emerging markets (MSCI EM) had positive 8.43% and 5.74% returns, respectively. Weakness in the U.S. dollar helped bolster international stocks, as the U.S. Dollar Index fell by more than 4% last week. Consumer prices (CPI) were expected to increase 8.0% year-over-year, down from an 8.2% reading in September, but last week the United States saw its lowest level of headline inflation since January, a welcomed sign for investors. October core CPI rose 0.27% month-over-month and fell to 6.3% year-over-year. In bonds, yields fell during the holiday-shortened trading week as both inflation data and U.S. midterms drove the 10-year Treasury yield below 4% for the first time since last month. For the week ahead, investors will keep a close eye on third-quarter earnings results. Many of the market's largest retailers are set to report earnings this week, including Home Depot (HD), Walmart (WMT), and Target (TGT).

Update on Inflation (from JP Morgan): After peaking at 9.1% y/y in June, inflation has slowly been receding. The October CPI report confirmed this trajectory as headline CPI surprised to the downside at 7.7% y/y – its smallest y/y increase since January. Core CPI also moderated to 6.3% y/y, down from 6.6% y/y in September. We are seeing gathering evidence of disinflationary forces at play, the most notable being a cooling economy and improving supply chains. First, the Fed’s aggressive rate hikes appear to be working and October’s CPI report should give the Fed confidence to slow to 50 bps in December. Second, easing supply chains are acting as disinflationary tailwinds for core goods. The Global PMI suppliers’ delivery time index has returned to its pre-covid norm as 1) inventories have matched more evenly with demand and 2) demand has cooled modestly due to higher rates. Global PMI input and output prices have also moderated, down 7.7 pts and 8.1 pts from their springtime peaks, respectively. Beyond PMIs, port congestion also has improved. In January 2022, there were 100-plus ships waiting to get into the Port of Los Angeles. Now, it hovers below 10 – a welcome sign of collapsing bottlenecks. As such, further improvements in supply chains should continue to act as a dampener on core goods inflation, albeit on a lag. In October, core goods inflation came in at 5.1% y/y, down from 6.7% y/y in September and its smallest y/y increase since April 2021. We expect this trend to continue as supply chains retreat to status quo. While inflation is finally moving away from its firmest period, risks for Fed overtightening still linger. Against this backdrop, investors should continue remaining defensive with well-diversified portfolios at this time.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.