Market Recap – Week ended May 20

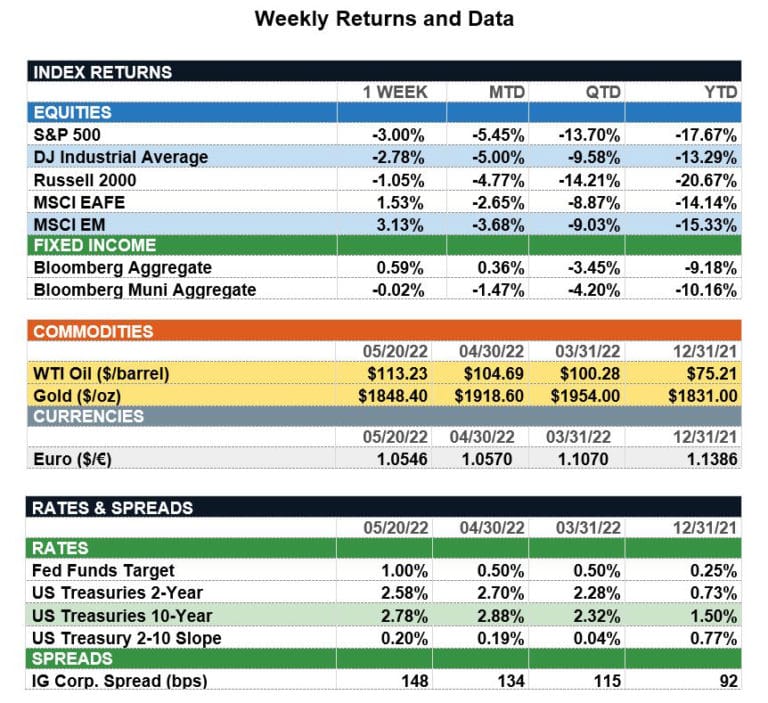

Overview: Stocks were mixed across the world last week as investors evaluated softer consumer demand, persistent inflation, and slowing economic growth. In the U.S., the S&P 500 index fell 3.0%, declining for the seventh week in a row. International stocks fared better, with international developed stocks (MSCI EAFE) and emerging market stocks (MSCI EM) up by 1.5% and 3.1%, respectively. In bonds, Federal Reserve Chair Powell affirmed the Fed’s resolve to get inflation down toward their 2% target, while at the same time acknowledging price stability may cause some economic pain. In a broad flight-to-safety trade, yields were lower, with the 10-year Treasury finishing the week 15 basis points (0.15%) lower at 2.78%. There was some good news on the economic data front, as core retail sales increased 1.0% for the prior month, above the consensus of 0.7%. This week, markets will be focused on the personal income and outlays data due out on Friday, May 27. This report includes the personal consumption expenditures (PCE price index) indicator that is the Fed’s preferred measure of inflation. The headline PCE price index is expected to fall from 6.6% to 6.3% for April, with the core PCE expected to improve from 5.2% to 4.9%. Investors will look at these numbers for indications inflation may be heading lower, which would be a welcome sign for the markets.

Update on Performance (from JP Morgan): Equity markets have seen a volatile start to the year, with the S&P 500 down 19% from its early January peak. A sharp move higher in interest rates on the back of a more hawkish Federal Reserve has pressured valuations, and subsequently left the index trading in-line with pre-pandemic levels and below its 25-year average. The re-rating in valuations has been particularly acute across growth stocks, as more defensive, value names have outperformed. Inflation should cool and lead the Federal Reserve to provide greater clarity on their outlook for monetary policy. This should translate into lower interest rate – and broader capital market – volatility. A narrower distribution of outcomes and continued growth in earnings will allow equity markets to stabilize, and in time, begin moving higher. Furthermore, consumer sentiment is at recessionary levels, which has historically coincided with strong equity returns over the next 12 months. The chart of the week highlights the returns investors stand to enjoy as the market moves back to its all-time highs; forward returns are looking far more attractive than was the case at the start of the year, even if new all-time highs are not set in the short-term. While painful, this year’s sell-off has created an opportunity for investors to rebalance portfolios and ensure they are appropriately positioned for the coming macro environment. At the same time, this higher volatility environment has supported stock pickers, with the greatest share of large cap core managers outperforming in more than a decade.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s , Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.