Market Recap – Week ending Jan. 27

Encouraging GDP, Inflation Data Push Stocks Higher

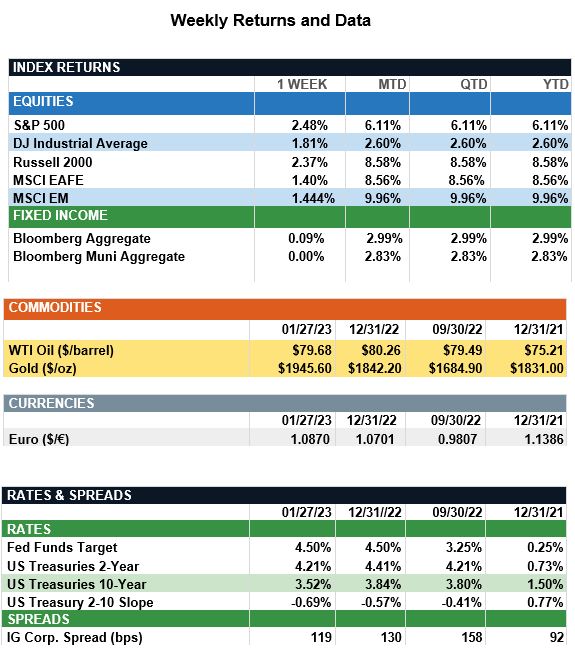

Overview: Stocks were higher across the globe last week, led by GDP and inflation data in the U.S. that supports a resilient economy with lessening price pressures on the inflation front. The S&P 500 index finished the week up 2.5%, and now is up about 6% through the first four weeks of 2023. The technology sector led the broad indices higher with the tech-heavy Nasdaq Composite index up 4.3% on the week. In the bond markets, yields mostly were unchanged with the 2-year and 10-year Treasury notes ending the week at a yield of 4.21% and 3.52%, respectively. Declining yields over the first month of the year have translated into a strong start for the bond market indices with the Bloomberg taxable and municipal bond benchmarks up around 3% so far in 2023. Economic data was encouraging, with U.S. gross domestic product (GDP) for the fourth quarter of 2022 rising at an annual rate of 2.9%, better than expectations. Investors are hoping growth is slowing enough to continue to bring down inflation while avoiding a recession. The Federal Reserve’s preferred measure of inflation, the core personal consumption expenditure (PCE) price index, increased at 4.4% year-over-year in December, a significant improvement from the November report of 4.7%. Upcoming this week is the first Federal Reserve meeting of 2023, where it is widely expected the Fed will raise the funds rate by 0.25% (25bp). The markets now are anticipating the Fed will slow the pace of tightening with the expectation for one more 25bp hike at the March meeting. In addition to the Fed meeting outcome, it will be a critical week for earnings, with about 20% of the S&P 500 companies schedule to report earnings this week. Key earnings reports will include McDonald’s and General Motors on Tuesday followed by technology heavyweights Apple, Meta, Amazon and Alphabet (Google) later in the week.

Wage Increases and Inflation (from JP Morgan): A one-time acceleration due to state minimum wage increases in January should not be interpreted as a sign the Fed is losing its battle with inflation. While the federal minimum wage likely will remain unchanged from $7.25/hour, 27 states and D.C. planned state minimum wage increases for 2023. On Jan. 1, 2023, increases went into effect that could drive wage growth higher in January’s jobs report. The increases thus far have raised the U.S. population-weighted average minimum wage to $10.87 from $10.45, a 4.0% increase. Once the remaining increases are carried out, that average wage will rise to $10.96 for a total increase of 4.8%. Regionally, scheduled increases vary: the Northeast will experience the fastest growth compared to last year of 6.1%, while the South, with only four states and D.C. raising their minimum wages, will experience the slowest growth of 3.4%. The West and Midwest will experience increases roughly in line with the national average. These increases could exert upward pressure on wages more broadly, even for those workers earning above the minimum wage. Wage growth has been a critical data point to the Fed as a signal of inflationary pressure, particularly in the services industries. Average hourly earnings have rolled over in the last four jobs reports and a one-time acceleration due to state minimum wage increases in January should not be interpreted as a sign the Fed is losing its battle with inflation. The broader dynamic of slower wage growth and moderating inflation is still intact, supporting a smaller 0.25% rate hike at the FOMC meeting this week.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.