Market Recap – Week ending Feb. 3

S&P 500 Records Five-Month High, Jobs Market Remains Strong

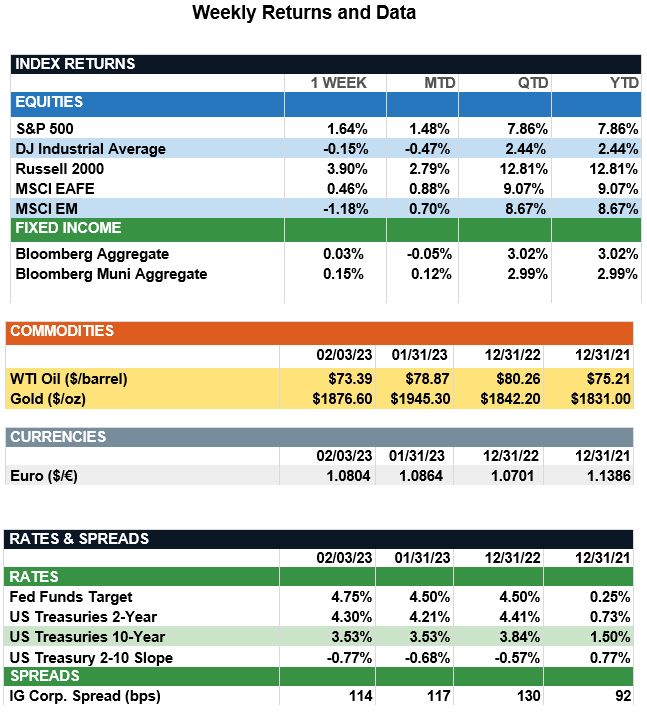

Overview: Global stocks were mostly higher last week as improving investor sentiment helped overcome rate hikes from central banks around the world. In the U.S., the S&P 500 index recorded a five-month high, up 1.6% on the week. The gains came on the heels of the latest Federal Reserve meeting, where the Fed raised the funds rate by 0.25%, as expected, while acknowledging signs of easing inflation. International developed stocks (MSCI EAFE) were higher as well, up 0.5%, as investors bet global rate hikes are nearing the end of the cycle. In the bond markets, yields initially traded lower as markets priced in a lower terminal funds rate, but reversed course later in the week after a strong employment report fueled concerns additional rate hikes may be necessary. The 2-year and 10-year U.S. Treasury yields ended the week at 4.30% and 3.53%, respectively. Meanwhile, Friday’s monthly employment report showed that despite consensus expectations for a slowdown, the jobs market remains robust. Nonfarm payrolls grew by 517,000, well above expectations, and the unemployment rate fell to 3.4% in January, the lowest level since 1969. This suggests a still strong labor market despite ongoing recession concerns and corporate layoffs.

Update on Earnings (from JP Morgan): With about half of market capitalization reporting, our current estimate for 4Q22 S&P 500 operating earnings (EPS) is $50.48, representing a y/y decline of 11.0% and a q/q increase of 0.3%. Commentary accompanying results released thus far suggests the year-over-year contraction in earnings is due to higher labor costs, a deterioration in consumer confidence, a stronger U.S. dollar, constrained supply chains and geopolitical tensions. However, despite the considerable set of headwinds, margins in aggregate have remained steady at 11.2%, with robust nominal growth continuing to boost revenues. Last week, we received notable results at the sector and industry level. While the consumer discretionary sector seems set for a tough quarter of earnings, the auto industry continues to be a bright spot. The positive results were primarily due to improved inventories and higher prices, but margins within the industry did narrow considerably, indicating demand has begun to normalize. In contrast to consumer discretionary, the information technology sector is currently tracking a solid year-over-year gain in earnings; however, reported results have varied within the sector at the industry level. For example, software earnings have stayed much more resilient relative to those in hardware, with management teams noting a sharp drop-off in the demand for PCs and gaming consoles. Finally, communication services, similar to many of the hardware tech names, had a difficult quarter as the sector is levered to discretionary sources of spending. While margins have stayed strong, guidance for the year ahead has indicated the worst is yet to come, particularly as inflation continues to decelerate and revenue growth subsides. As such, it is unsurprising 2023 has kicked off with a flurry of job cut announcements, particularly in those sectors that experienced rapid growth during the pandemic and responded by increasing the number of workers they employ.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.