Market Recap – Week Ending 02.10.23

Stocks lower; CPI Report due Tuesday

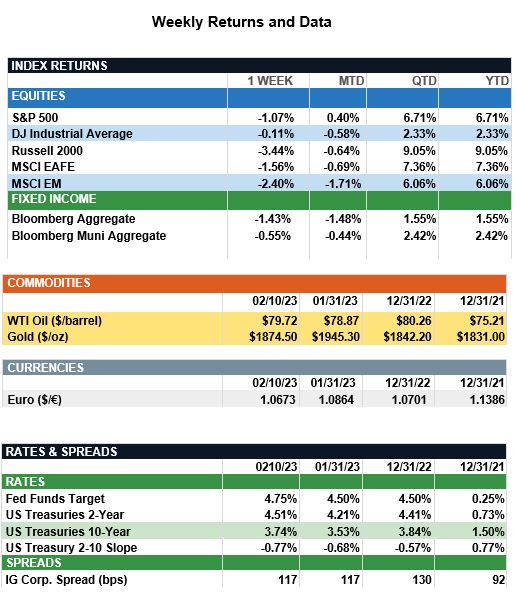

Overview: Stocks were lower around the world in volatile trade last week with international developed stocks (MSCI EAFE) down 1.6% and emerging markets (MSCI EM) lower by 2.4%. In the U.S., investors continued to evaluate the implications of monetary policy and mixed corporate earnings, as the S&P 500 index fell 1.1% on the week. Market focus remains on actions by the Federal Reserve, as Fed Chairman Jerome Powell reiterated getting inflation under control remains a top priority. Powell stated that despite the disinflationary process already underway, continued interest rate increases will likely be necessary. He repeated a focus on making decisions one meeting at a time while evaluating economic growth and inflation data. U.S. Treasury yields ended the week higher, as Powell’s commentary suggested the potential for higher rates. The 10-Year U.S. Treasury yield increased from 3.53% to 3.74% on the week, and the 2-Year yield hit a two-month high, finishing the week at 4.51%. Focus this week will be on the January Consumer Price Index (CPI), to be released on Tuesday, Feb. 14, where headline annualized inflation is expected to fall from 6.5% to 6.2%. Last week, the widely followed University of Michigan 1-Year Inflation expectations increased from 3.9% to 4.2%, while the 5-Year Inflation expectations stayed flat relative to the prior month at 2.9%. Feedback from the survey suggested uncertainty remains elevated for both inflation and rising unemployment in the labor markets.

Update on Inflation (from JP Morgan): Improving global PMIs and a much better-than-expected employment report recently have given investors new confidence the economy can avert a near-term recession, boosting market sentiment and stock prices. Meanwhile, the Fed has remained mostly steadfast in its hawkish messaging, raising the likelihood of additional 0.25% rate hikes in both March and May. This week, attention shifts to a slew of inflation data for January. After a string of months of promising disinflation progress, January's CPI likely will show a bounce in headline inflation due to higher energy prices and persistent owners' equivalent rent inflation. Manheim data last week also showed used car prices spiked in January, breaking a trend of sharply falling auction prices and warning of a turn in a major contributor to lower core inflation in recent months. However, while the data may signal some plateauing in used car disinflation in the coming months, higher auto inventories and bloated dealers’ margins in the context of softening consumer demand still point to a need for further declines in new and used vehicle prices. Other data also show price pressures unwinding convincingly. Pricing indicators from the manufacturing and services PMI surveys have declined sharply since mid-2022, down to a combined value of 56 from a peak of 85 last March. We think the disinflationary wave has room to run, but progress won’t be linear and inflation data in the very near term could plateau or even turn higher. Still, gathering evidence on a broad weakening of economic growth and inflation should soon lead the Fed to reverse course. For investors, it’s also important to take a longer-term view amidst choppy economic data and position portfolios for the eventual return to a slow-growth and low-inflation economy.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.