Market Recap – Week ending Feb. 17

Stocks Unchanged, Consumer Price Index Above Expectations

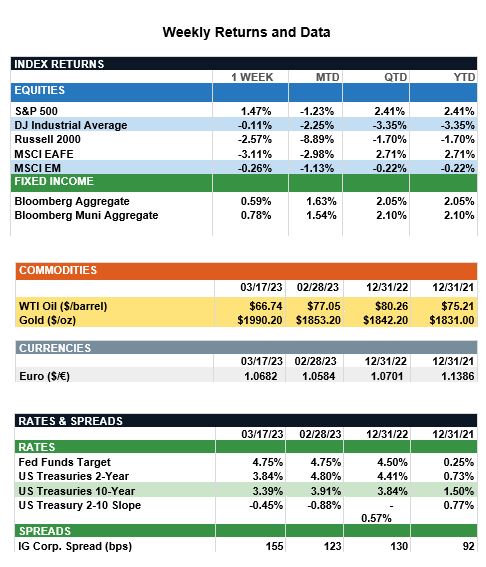

Global stocks were largely unchanged last week as investors continue to decipher monetary policy and inflation. In the U.S., the S&P 500 index finished the week lower by 0.2%, but still is up 6.5% for the year. In the bond markets, yields were higher in the U.S. as strong retail sales and above consensus releases for inflation data led to a higher expected terminal funds rate. Consumer prices (CPI) and producer prices (PPI) both came in above expectations, and retails sales reported an increase of 3.0% for the month of January, well above consensus estimates of a 1.7% increase (see details below). Futures markets, according to Fed Watch data, now are expecting a peak Fed Funds rate of 5.25%-5.5% this summer, implying three more 25 basis point hikes from the current level of 4.5%-4.75%. The one-year Treasury yield traded above 5% for the first time in 15 years, with the 2-year and 10-year Treasury yields closing the week at 4.62% and 3.83%, respectively. Rates across the Treasury curve are higher by 0.3%-0.4% since the end of January, reflecting the higher peak expectation for the funds rate. As investors continue to monitor inflation, key data will come this Friday when the personal income and outlays report is released. This report includes the PCE price index, which is closely watched by the Fed. The annualized core PCE price index for January is expected to fall to 4.3% from 4.4% the previous month, as markets hope price pressures continue to fall.

Update on Consumer Spending (from JP Morgan): U.S. retail sales rebounded sharply in January, exceeding expectations, and signaling the American consumer continues to spend. After consecutive months of decline into the end of 2022, nominal retail sales jumped by 3% m/m in January. Although seasonal factors and the largest cost-of-living adjustment to Social Security since 1981 may have played a role in this surge, the increase in sales was broad-based. Vehicle sales were the largest contributor to growth, and food services – a proxy for services spending – rose by 7.2%, the most since March 2021. With growth better than expected and inflation proving to be sticky, markets have gravitated toward a new narrative of “no landing." The retail sales report is important for assessing the state of the consumer, which matters because consumption is nearly 70% of GDP. However, the sustainability of this spending should be assessed in light of a declining household savings rate and climbing credit card balances. At the beginning of February, the market had priced a terminal federal funds rate below the Federal Open Market Committee (FOMC) projection; however, in the wake of strong jobs, inflation and retail sales reports, markets quickly repriced the terminal rate more in line with the median projection. While it is good to see market and Fed expectations better aligned, stronger economic growth suggests it may take longer for inflation to come back to levels that are consistent with the FOMC’s mandate.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.