Market Recap – Week Ending 02.18.22

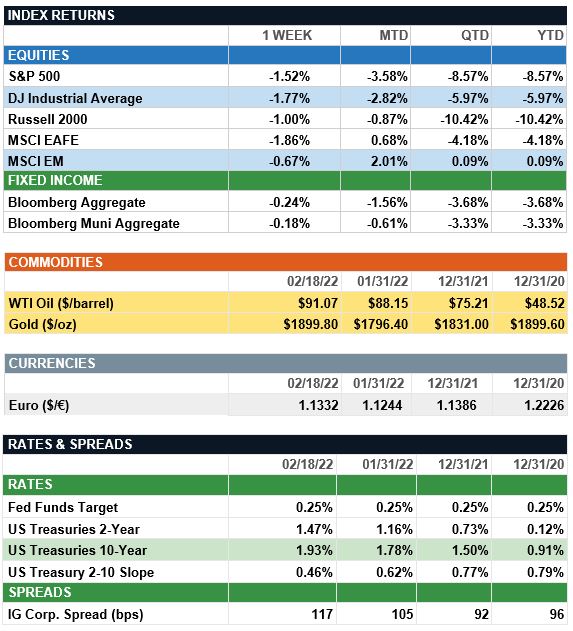

Overview: Global stocks were lower last week as investors moved into safe assets amid rising tensions in Ukraine. The S&P 500 ended 1.5% lower, as geopolitical concerns dominated encouraging earnings releases. Inflation continues to be at the forefront of investor concerns, as headline producer prices (PPI) rose 1.0% in January and 9.7% on an annualized basis. Excluding food and energy prices, U.S. core PPI increased by 8.3% year-over-year. Meanwhile, U.S. retail sales rose in January, beating consensus estimates. Better-than-expected sales reflected seasonal post-holiday increases in motor vehicle, online shopping, and furniture sales. In the U.S., 10-Year Treasury yields ended the week at a yield of 1.93% after trading as high as 2.06% during the week, as markets reacted to the Russia-Ukraine standoff with a flight-to-quality posture late week.

Earnings: U.S. earnings results have so far proved resilient for the final quarter of 2021, outpacing consensus estimates. With 84% of companies having reported, 52% have beaten earnings estimates by more than one standard deviation, above the historical average of 47%. In the view of Goldman Sachs, earnings growth will continue to normalize, but stay supportive of valuations, and deliver 8% EPS growth for 2022.

A Note on Inflation (from JP Morgan): As investors and consumers mull the implications of persistently high inflation, soaring energy prices are a concern. Energy prices are up a striking 27% y/y in the CPI basket and contributed 2.5% points alone to the 7.5% y/y January CPI reading. Strong demand and tight supply have sent prices higher in commodities markets. Normally, commodity futures markets are in “contango”, meaning current spot prices are lower than futures prices due to the storage and depreciation costs of holding the asset over a period of time. Today, spot prices for the top eight constituents in the Bloomberg Commodity Index (BCOM) are running an average 6% higher than their one-year forward price. This condition is known as “backwardation” in futures markets, and commodities backwardation has been hovering around a 15-year high since early 2021. One silver lining, however, is that lower prices for futures contracts imply expectations for a decline in commodity prices by next year, as the pandemic hopefully fades, and supply chains catch up.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s , Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.