Market Recap – Week ending Feb. 24

Stocks Lower After Release of Fed Minutes, PCE Report

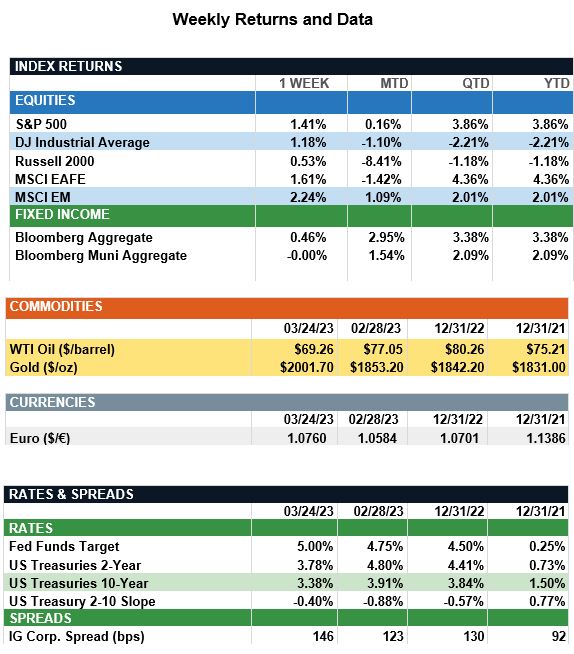

Overview: Global stocks fell last week as markets digested higher interest rates and a report that showed a reversal in the moderation of inflation. In the U.S., the core personal consumption expenditures (PCE) price index rose 4.7% year-over-year in January, well above the consensus expectations of 4.3%. In addition, minutes from the latest February Federal Reserve meeting suggested additional rate hikes are needed to bring down inflation. In the U.S., the S&P 500 Index finished lower by 2.7%, with international developed stocks (MSCI EAFE) down 2.4% and emerging markets (MSCI EM) lower by 2.7% on the week. In bonds, yields on the 2-year and 10-year Treasury notes rose by 0.18% and 0.12%, to end the week at 4.80% and 3.95%, respectively. Yields across the Treasury curve now are about 50 basis points (0.50%) higher since the beginning of the month, resulting in negative returns for both taxable and municipal indices of between 2-3% for February. The minutes from the February Fed meeting noted all Fed members anticipate “ongoing” rate hikes would be appropriate going forward, language which has influenced the recent weakness in stocks and increased interest rates.

Update on Earnings and the Consumer (from JP Morgan): With more than 90% of the S&P 500’s market cap reported, we are tracking 4Q22 operating earnings per share (EPS) of $49.37, representing y/y and q/q declines of 13.0% and 1.9%, respectively. Furthermore, S&P 500 operating margins are sitting at 10.8%, down from 13.4% in 4Q21 and 11.3% in 3Q22. At the sector level, energy and utilities have led the pack this earnings season due to higher oil and gas prices. At the same time, industrials are set to record another quarter of y/y growth due to resilient spending on services offsetting softening manufacturing demand. However, consumer discretionary, communication services and information technology – all of which are levered to non-core spending – had another tough quarter, as higher labor costs and souring consumer confidence weighed on profits. While results diverged from sector to sector, forward guidance among most companies is pointing toward a softer economic environment as demand slows and inflation remains persistent. Although the corporate outlook has deteriorated, the economy has continued to hum along in 2023. Last Friday’s January personal income and outlays report indicated personal income increased 0.6% m/m and consumer spending increased 1.8% m/m, with the personal saving rate rising to 4.7%. However, much of the boost in personal income and personal saving was driven by the 8.7% Social Security cost-of-living adjustment and higher compensation, which should wane as wage growth moderates. Additionally, while consumer spending remains strong, the steep increase in credit card debt highlights the degree to which spending is being supported by borrowed money. The consumer’s increasing reliance on borrowing should make further increases in consumer spending unsustainable, suggesting, similar to management commentary, that a slowdown may be lurking around the corner.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.