Market Recap – Week Ending 02.25.22

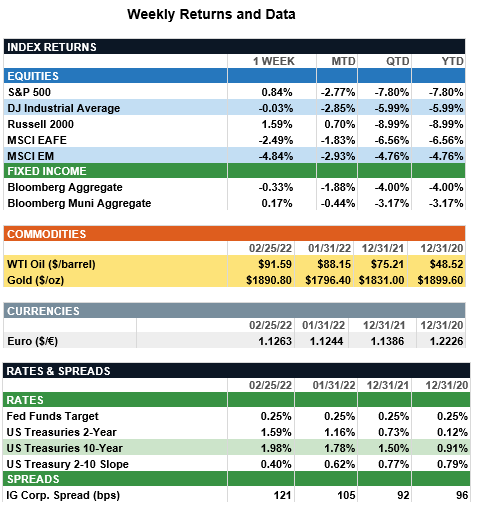

Overview: Global stocks sold off sharply mid-week as Russia invaded Ukraine, with uncertain ramifications causing investors to move to safe haven assets. In the U.S., the S&P 50 index rallied on Friday to finish the week 0.8% higher, while international stocks finished in negative territory for the week. Volatility remains elevated, as investors are concerned that supply disruptions could fuel additional inflation, and that the Russia/Ukraine conflict could escalate. Oil prices rose, with WTI crude oil finishing the week up over $3 per barrel at $91.59, over concerns of supply disruptions from sanctions and the possibility of Russia restricting exports. In bonds, yields were steady, as the 10-year Treasury finished the week at a yield of 1.98%. In economic news, U.S. core personal consumption expenditures (PCE) inflation rose to 5.2% year-over year last month, the highest annual increase since 1983. The question now is how the Federal Reserve will act over the next couple of weeks to address high inflation in this environment of increased geopolitical risk. Fed Chair Powell will give his semiannual monetary policy testimony on Wednesday, leading up to the next Fed meeting on March 15-16, where the FOMC is expected to begin raising interest rates. Further clarity on the pace of interest rate increases, along with balance sheet reduction, will be watched closely by the markets.

Russia Update: (from JP Morgan) Following Russia’s invasion into Ukraine, markets saw a sharp sell-off in risk assets, while safe-haven assets (i.e. Treasuries, USD and gold) outperformed. Russia-linked commodities popped with European natural gas +60% and Brent prices crossing $100/barrel. However, by the end of Thursday, markets largely reversed their course with only minimal moves to the 10Y (-1bps) and WTI (+$1). Looking ahead, markets will be sensitive to sanctions and Russia’s counter response to them. This is a balancing act as the West wants to punish Russia, but not at the expense of other economies. It is further complicated by the fact that Russia is the second largest producer of oil and natural gas and a major commodities supplier (i.e. fertilizer, wheat, aluminum). As of Friday, sanctions have involved Russian oligarchs, new Russian sovereign debt, Russia banks and Nord Stream 2. but, they have not yet involved Russia’s use of SWIFT or Russian oil and gas.

For U.S. consumers, this crisis is likely to dampen sentiment and has the potential to delay peak inflation. Despite these headwinds, Americans are coming into this at a fundamentally healthy position – consumer demand has been robust (i.e. January retail sales surprised to the upside despite Omicron concerns) and consumer balance sheets have been strong. While we might see price pressure on energy and food in the near term, they do not have the same capacity to shock as they once did. Energy and food spending now represents much less of Americans’ overall wallet share – 12% of total spending vs. an average of 23% throughout the 60s/70s. Furthermore, America has a greater degree of energy independence and the luxury of natural resources that Europe does not, which should also soften the blow. In terms of investment implications, remember that staying invested in a diversified, goals-aligned portfolio has paid off through countless geopolitical crises and should continue to do so. Ultimately, portfolios should benefit from quality stocks with durable profits and fixed income for portfolio ballast. We are not advocating for broad rebalancing at this time, but rather are seeking balance between value vs. growth and U.S. vs. international. Diversification will remain key as we ride out volatility.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.