Market Recap – Week Ending Feb. 9

Earning Reports Data; CPI Release on Tuesday

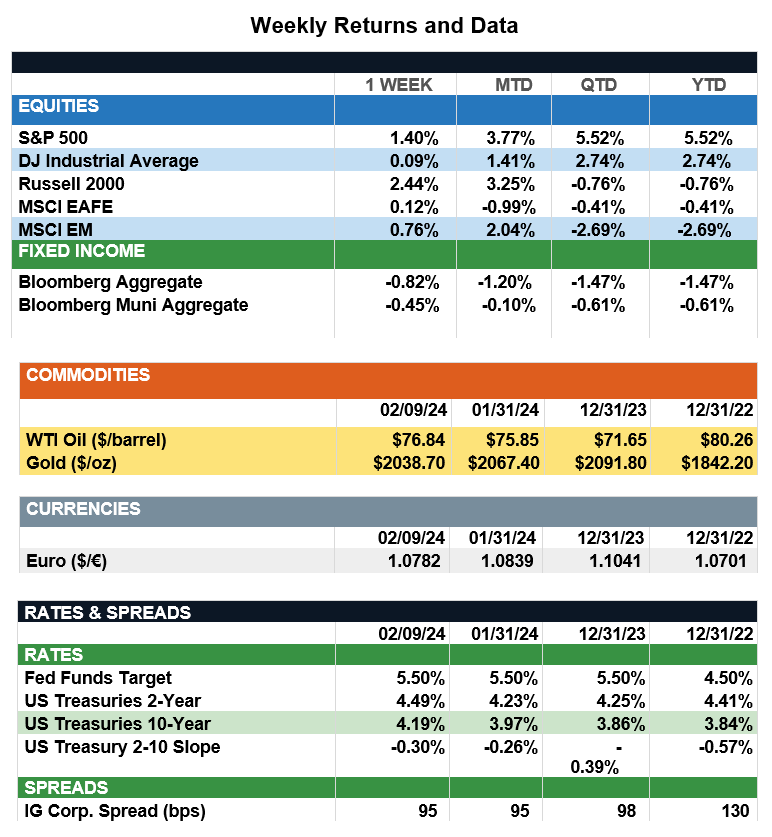

Overview: Stocks extended their global rally last week as the S&P 500 index continued to lead the way, finishing the week 1.4% higher. In a quiet data week, investor focus was on earnings with companies generally reported strong results. According to data from FactSet (as of Feb. 9), 67% of S&P 500 companies have now reported 2023 fourth-quarter earnings with 75% having reported earnings above consensus expectations and 65% reporting a positive revenue surprise. Earnings reports continue in the week ahead, including companies such as Coca-Cola, Kraft Heinz, and Hasbro, as investors evaluate the health and outlook for consumer spending. In bonds, yields rose last week as Federal Reserve Chair Jerome Powell suggested in a “60 Minutes” interview that rate cuts may begin later than markets are currently expecting. In bonds, yields were about 0.15% higher for the week with the 2-Year and 10-Year U.S. Treasury yields finishing the week at 4.49% and 4.19%, respectively. In addition to earnings, this week’s focus will be on the Consumer Price Index (CPI) report due out Tuesday, where headline CPI is expected to fall from 3.4% to 3.0% on a year-over-year basis.

Update on Inflation (from JP Morgan): Inflation is often feared to be a self-fulfilling prophecy, as consumers and businesses expect higher prices may inadvertently fuel inflationary pressures themselves. For example, consumers may ask for a raise or accelerate purchases to front-run rising prices, while businesses may hike prices in anticipation of higher input costs. To maintain price stability, the Federal Reserve closely monitors long-term inflation expectations and aims to keep them anchored at levels consistent with its inflation mandate. For investors, understanding the different measures of inflation expectations is critical for assessing the outlook for inflation and policy. This week, we look at inflation expectations for the next five years from consumers, professional forecasters and financial markets. After spiking in 2022, inflation expectations have steadily trended back to normal. In fact, professional forecasters surveyed by the Philadelphia Fed and investors trading 5-year break-evens both expect annual CPI inflation of 2.3%, consistent with the Fed reaching and maintaining its 2% PCE inflation target through 2028. Consumers, likely burdened by negative headlines, have a more pessimistic outlook as those surveyed by the University of Michigan anticipate annual inflation of 2.9%. However, not only have consumers’ expectations historically settled above others, but also move more slowly and rarely deviate from their long-term average, suggesting financial markets and professionals may offer more valuable insights in real time. Despite geopolitical tensions and resilient economic activity, well-anchored inflation expectations should help keep inflation on its downward trend, opening the door for policy easing from the Fed later this year. Indeed, the January CPI report could show the disinflationary momentum established in 2023 continued into 2024.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg, CNBC, FactSet

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.