Market Recap – Week ending Mar. 3

Stocks Rebound, Key Jobs Data This Week

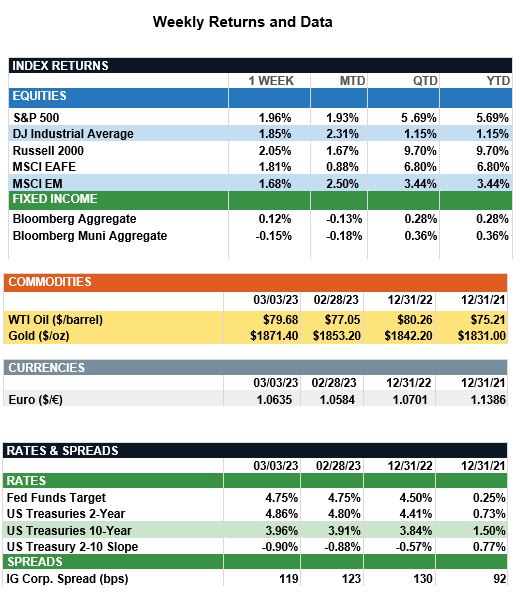

Overview: Global stocks moved higher last week as investors digested the prior week’s inflation reports and the potential impacts on monetary policy. In the U.S., the S&P 500 snapped a streak of three consecutive down weeks and rallied 1.96%. In Europe, the STOXX 600 index gained 1.50% despite a number of higher-than-expected readings on inflation. In China, the Hang Seng index jumped more than 3% following the release of much stronger-than-expected manufacturing data. As China continues to recover from COVID shutdowns, the official China purchasing managers index (PMI) rose to 52.6 in February, the highest level in more than 10 years.

In bonds, commentary from several key Fed officials caused interest rates to continue their march higher. The yield on the 10-year U.S. Treasury breached 4% for the first time since last fall as markets now expect a higher for longer rate environment. Looking ahead to this week, investors will be focused on employment data this week with the ADP employment report due out Wednesday, followed by the U.S. nonfarm payrolls report on Friday where economists are expecting the U.S. labor market to have added approximately 200,000 jobs in February.

Update on Central Bank Policy (from JP Morgan): Recent unexpectedly strong economic data have caused U.S. investors to reassess their outlook on U.S. monetary policy. After February’s Federal Open Market Committee (FOMC) meeting, federal funds futures were pricing in a terminal rate of 4.9% and a year-end rate of 4.4%, implying two rate cuts by the end of 2023. However, continued labor market momentum, surging retail sales and strong CPI and PCE prints released in February suggest the economy and inflation may prove more resilient than initially anticipated. Markets now are more hawkish, pricing at a terminal rate of 5.4% and no cuts until 2024. This implies three hikes with the possibility of a fourth at the July meeting. Notably, persistent inflation fears have materialized in Europe, as well, and markets now expect the European Central Bank to hike to a terminal rate of 3.9%.In February, markets suffered as investors grappled with the prospect of higher rates for longer. The S&P 500 fell 2.6%, while the 2-year Treasury yield recently climbed to a cycle high of 4.9% and the 10-year yield breached 4%. Looking ahead, we remain cautious toward equities. Although valuations have improved after February’s sell-off, the S&P’s forward P/E ratio remains slightly above average levels, indicating equities may come under further pressure due to higher rates. However, despite the recent back-up in yields, we expect the economy will eventually slow, inflation will fall, and monetary policy will become looser. Therefore, bonds look attractive at current valuations and once again offer investors income and diversification benefits.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s , Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.