Market Recap – Week Ending 03.04.22

Market Recap – Week ended March 4

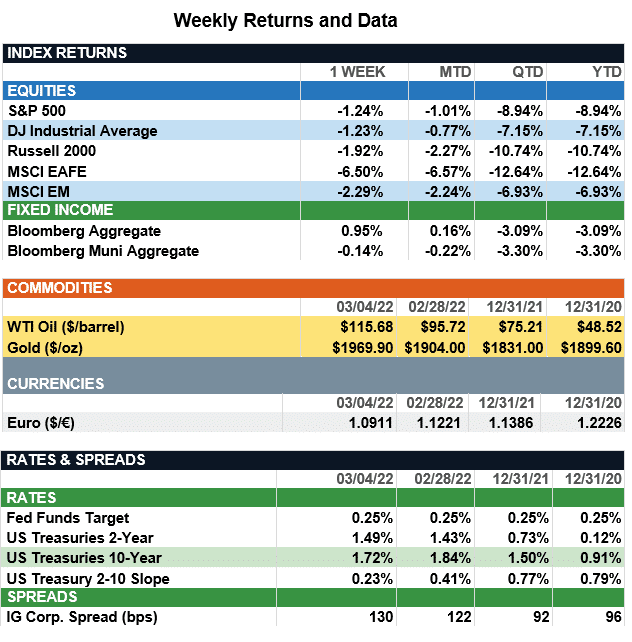

Overview: The effects of the intensifying Russia-Ukraine conflict continued to drive global stocks lower last week. International stocks were hit the hardest, with international developed (MSCI EAFE) and emerging markets (MSCI EM) down 5.5% and 2.3%, respectively, on the week. In the U.S., the S&P 500 index was down 1.2% in a volatile week of trading, with losses tempered after testimony from Federal Reserve Chair Jerome Powell, who indicated the Fed would be gradual and data dependent in its policy of raising interest rates. In energy markets, fears of a supply crunch led oil prices to surge last week, with WTI crude oil finishing the week at $115.68 per barrel, driving the average price of regular gas to more than $4 per gallon in the U.S. In the bond markets, the 10-year Treasury yield fell 12 basis points (0.12%) to 1.72%, as investors sought safe-haven assets. In economic news, February U.S. nonfarm payrolls reported a rise of 678,000 jobs, well above expectations of 390,000. Strong job growth pushed the unemployment rate down to a post-pandemic low of 3.8%.

A Note on the Consumer (from JP Morgan): When it comes to economic growth in the United States, the consumer is key, accounting for nearly 70% of gross domestic product (GDP). Following the initial pandemic shock in early 2020, the consumer came back with a vengeance, as stimulus checks and enhanced unemployment benefits stabilized balance sheets across the U.S. and spending on goods accelerated meaningfully. However, with food and energy prices rising, there is a risk that the composition of consumer spending will begin to shift. Looking at energy spending as a percentage of total spending, we are able to model a scenario in which crude oil prices rise to $120 per barrel. In aggregate, however, the model forecasts energy spending would increase to 5.0%, which is only slightly above the 2021 average of 4.8%.

That said, the devil is in the details. To an extent, economic growth has been solid and inflation has been elevated due to stimulus that lined the pockets of lower-income individuals. This group has a much higher marginal propensity to consume – put differently, if they have extra money in their pocket, they are more likely to spend than save. This cuts both ways. If oil prices spike to $120, energy spending may rise to 13.9% of total spending compared to an average of 10.1% in 2021 for the lowest-earning individuals, limiting their ability to consume other items. This could in turn lead to slower economic growth than expected, but also a more rapid decline in core inflation. While we still expect the Federal Reserve (Fed) will hike interest rates at its March meeting, this dynamic may allow the Fed to tighten more gradually than markets currently expect.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s , Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.