Market Recap – Week ending Mar. 10

Markets React to Fed Chair Comments, Bank Concerns

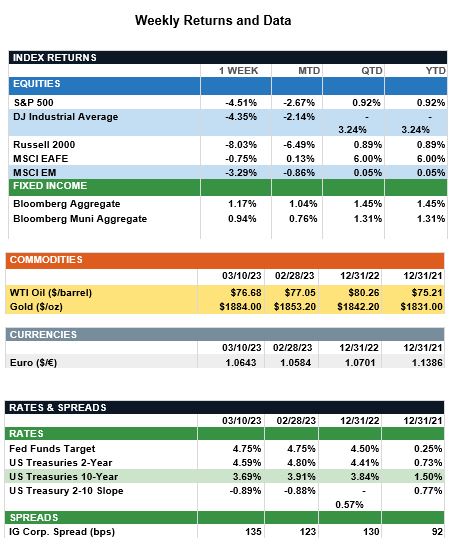

Overview: Stocks were lower across the globe last week with selling Friday exacerbated by the failure of Silicon Valley Bank (SVB) and the potential concerns around other regional banks. In the U.S., the S&P 500 index fell 4.5%, reacting not only to concerns in the banking system but also to remarks from Federal Reserve Chair Jerome Powell to Congress. Last week, during his testimony to the Senate Banking Committee, Powell stated the terminal federal funds rate was “likely to be higher than previously anticipated” given recent growth and inflation data. He added the Fed would be “prepared to increase the pace of rate hikes” if needed. In economic data, the labor market remains resilient with nonfarm payrolls exceeding consensus expectations for the 11th consecutive month. New jobs rose 311,000 in February, versus consensus expectations for a 225,000 increase. The unemployment rate increased from 3.4% to 3.6% largely as a result of an increase in the size of the labor force. In the bond markets. the 10-Year U.S. Treasury yield fell 0.22% last week to 3.69% as the Bloomberg Aggregate and Muni bond indexes both returned about 1% for the week. Meanwhile, the 2-Year U.S. Treasury yield topped 5% mid-week, the highest level since 2007, but ended the week lower at 4.59% following concerns surrounding the health of regional banks. Yields continued to fall over the weekend, and as of Monday morning March 13, the 2-year and 10-year Treasury notes were trading at yields of 4.14% and 3.50%, respectively. This week, markets will get a read on the Consumer Price Index (CPI) data for February, where headline inflation is expected to fall from 6.4% to 6.0%.

Update on the Labor Markets (from JP Morgan): Despite many layoff announcements, the recent unemployment rate and job openings figures, 3.6% and 10.8m, respectively, continued to signal tightness in the labor market. Beneath the surface, there actually is less strength than meets the eye with wages failing to keep pace with inflation the past 23 months. With that said, in his Congressional testimony last week Federal Reserve Chair Jerome Powell mentioned the need for wage growth to continue decelerating in order to gain confidence that core services inflation, excluding housing, is finally showing signs of softening. Wage growth is a critical data point given its relationship with core services prices. Statistical analysis shows wage growth has a more discernable impact on core services inflation than the unemployment rate. On Friday, we saw average hourly earnings for production and nonsupervisory employees increase 0.2% month-over-month in February and 4.6% year-over-year. This is the second-slowest monthly wage growth we have seen since March 2021. While trending in the right direction, in the long run wage growth closer to 3.5% would be required to achieve and sustain the Fed’s 2% inflation target. A wider mosaic of labor market statistics shows a broad deceleration, but compensation growth remains at elevated levels. As a result, the Fed is signaling it is likely to take rates higher and keep them there for longer than previously expected. While the bond market now is better pricing in this path for rates, the equity market may see some volatility ahead given the increased odds the Fed goes too far and ends up pushing the economy into recession.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.