Market Recap – Week Ending March 15

Stocks Lower, Bond Yields Rise; Federal Reserve Meeting This Week

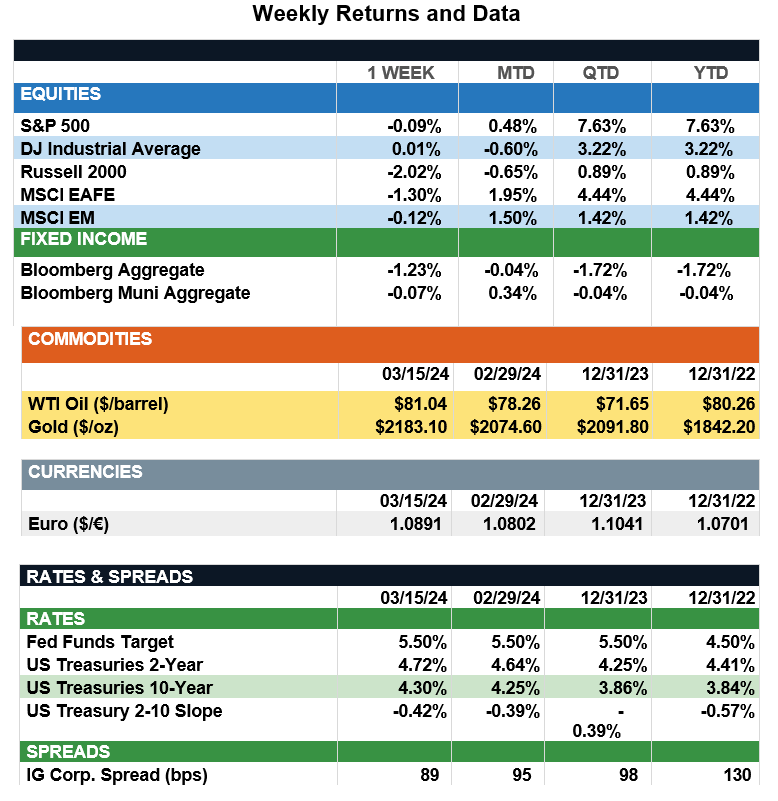

Overview: Stocks around the world were marginally lower last week and bond yields rose as consumer price (CPI) and producer price (PPI) inflation reports showed above-consensus expectations for February. Inflation concerns have pressured stocks recently, with the S&P 500 index recording its second consecutive weekly return, down 0.1%. Core CPI fell to 3.8%, less than the 3.9% expected, and core PPI also surprised to the upside. These hotter-than-expected inflation reports have added to concerns the Federal Reserve may wait longer before considering cutting rates. In bonds, 2-year and 10-year yields both rose more than 20 basis points (0.20%) on the week, to levels of 4.72% and 4.30%, respectively, translating to a negative return of about 1.2% for the Bloomberg Aggregate Index. This week, investors will focus on the Federal Reserve policy meeting March 19-20, where markets will receive updated growth and interest-rate projections from Fed members. According to the Chicago Mercantile (CME) FedWatch tool, futures markets currently are pricing in a near certainty the Fed will leave benchmark interest rates unchanged at the meeting this week. Investors now are expecting about a 50/50 chance of a rate cut at the upcoming June meeting, with an expectation of about three rate cuts over the remainder of 2024. If realized, this would result in a funds rate range of 4.50%-4.75% by year-end 2024.

Update on Economic Growth (from JP Morgan): After the U.S. economy’s impressive 4% annualized growth in the second half of 2023, investors are searching for clues as to whether this strong momentum will persist into 2024. For much of this quarter, the closely watched Atlanta Fed GDPNow model has forecasted growth of at or above 3%. However, after last week’s retail sales report, estimates were revised meaningfully lower. Retail sales rose 0.6% m/m in February, marking the fastest gain since September, but sales for January and December were revised down by 0.5% and 0.3%, respectively. Spending at gas stations rose 0.9%, reflecting higher gasoline prices, while spending at auto dealers and building material suppliers only partially recovered last month’s losses. Importantly, control group retail sales, which are used to calculate GDP and exclude gasoline, autos, building materials and food services, looked bleak, remaining unchanged after a 0.3% decline in January. With control group sales now tracking negative through the first two months of the year, the Atlanta Fed nowcast for 1Q real personal consumption fell from 3.4% to 2.2%, dragging the latest GDPNow estimate for 1Q24 growth down to 2.3%. Overall, consumer momentum appears to be fading after an impressive 2023. However, as falling inflation and rising real wages offset dwindling excess savings, even moderate consumption growth could carry the U.S. economy to a soft landing this year. In this environment, stocks could grind higher while bond yields remain relatively stable, although a well-diversified portfolio may best protect against any unforeseen threats that could emerge.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg, CNBC

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.