Market Recap – Week ending Mar. 17

Stocks Mixed in Volatile Trade; Fed Meeting This Week

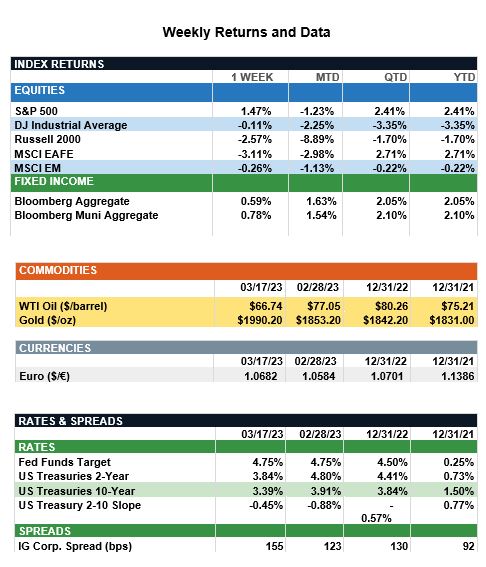

Overview: Global stocks were mixed in volatile trade last week, driven by concerns over the impact of rising interest rates on the banking sector. The creation of a Bank Term Funding Program (BTFP) by the Federal Reserve to support banks by making additional funds available through loans, along with support from the FDIC, helped ease concerns about systemic risks to the banking system with the S&P 500 index finishing the week 1.5% higher. In Europe, UBS agreed to buy the troubled Credit Suisse bank for three billion Swiss francs, or $3.2 billion, with the combined bank to have $5 trillion in assets. In addition, the Fed announced it had joined with other central banks in a joint liquidity operation, agreeing to increase the frequency of their U.S. dollar swap line arrangements from weekly to daily. In the bond markets, yields fell sharply, with the 2-Year and 10-Year U.S. Treasury yields finishing the week at 3.84% and 3.39%, respectively. For perspective, the 2-year Treasury note has fallen in yield by almost 1% since ending February at a yield of 4.80%. In economic news, the February Consumer Price Index (CPI) year-over-year headline rate fell to 6.0%, continuing to trend down from its peak of 9.1% in June of last year. Markets now focus this week on the Federal Reserve’s March 21-22 meeting where futures markets (FedWatch data) now are pricing in about a 70% chance of a 25-basis-point hike at the conclusion of the meeting, with the other 30% betting the Fed will keep the funds rate at the current 4.50% - 4.75% level, given the turmoil in the banking system.

Update on the Equity Markets (from JP Morgan): Last week was a volatile ride, as markets digested news of Silicon Valley Bank’s failure, the government’s response, and concerns regarding several other banks. Investors now are questioning what this means for their equity portfolios. Last week, the focus shifted toward quality and safety, leading large-cap stocks to outperform small cap, with the S&P 500 and Russell 2000 indexes finishing 1.5% higher and 2.6% lower, respectively. This can be explained by small cap’s larger exposure to financials at 18.5%, compared to large cap at 10.5%. Moreover, within financials, banks account for the majority of small cap’s weighting compared to just 31% of large cap’s weighting. While small cap underperformed large cap by 86% over the past 15 years, leaving valuations at very discounted levels, large cap continues to look favorable in the current environment given its greater exposure to defensive sectors. Additionally, the current net profit margin for the Russell 2000 is 4.6%, starkly lower than the S&P 500’s 12.3%, reflecting small cap’s increased vulnerability to elevated costs. When it comes to style, growth outperformed value last week by 5.8% due to its lower weighting to financials and a pivot back to tech as Fed tightening expectations softened. Value most likely will face further headwinds in the near term due to its exposure to bank stocks. However, investors should look past short-term volatility and focus less on which style to overweight and more on prudent company selection as valuation gaps have narrowed significantly in the past year. While macroeconomic uncertainty and higher interest rates pose challenges for all companies, investors can best weather the storm by emphasizing quality within different market caps and styles.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.