Market Recap – Week Ending 03.18.22

Market Recap – Week ended March 18

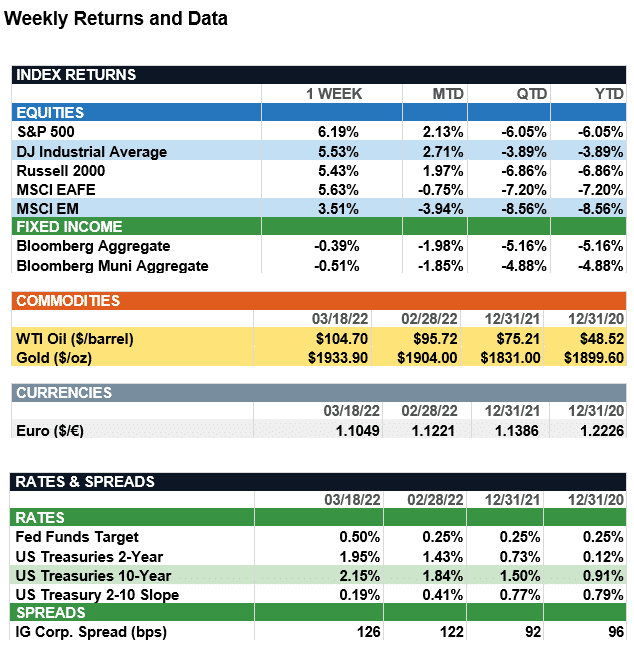

Overview: Stocks across the globe rallied last week as investors evaluated the latest Russia-Ukraine news and as the Federal Reserve began their cycle of interest rate increases. In the U.S., the S&P 500 index ended the week 6.2% higher, the strongest weekly gain since November 2020. Markets were encouraged by further progress of Russia-Ukraine peace talks and the easing of oil prices, which closed the week (WTI crude) at $104.70 per barrel, after trading above $123 per barrel the previous week. In the bond markets, 2-year and 10-year Treasury yields finished the week at 1.95% and 2.15%, respectively, as the Fed raised short-term rates by 25 basis points (0.25%), in line with expectations. On the inflation front, U.S. headline producer prices (PPI) rose 0.8% in February and 10.0% over the past year, in part reflecting the effects of surging commodities and gasoline prices.

Federal Reserve Update (from JP Morgan): Last week, the Federal Open Market Committee (FOMC) delivered on a very well-communicated 25 bps hike, raising its federal funds target range to 0.25%-0.50%. As an overnight lending rate for banks, the federal funds rate influences consumer and business borrowing costs including rates on mortgages, credit cards, savings accounts, loans, and corporate debt. When the Fed raises rates, they use it as a tool to tame hot consumer prices by making borrowing more expensive and saving more appealing.

As we head into the first rate hiking cycle since 2018, American investors should anticipate the following: First, investors should expect more tightening. The Fed made it clear it plans to hike rates more quickly and act nimbly regarding incoming data. Accordingly, the median FOMC member is now signaling a hawkish path ahead with six additional hikes expected this year. This would push up the Federal funds target range to 1.75- -2.00% by December 2022, a full percentage point higher relative to last December’s meeting. Upon conclusion of the Fed meeting on March 16, markets pulled forward their expectations for the implied policy rate at year-end to 1.99%, up from 1.83% just the day prior and from 0.82% at the start of the year. As we prepare for higher rates, investors should refocus their attention on valuations and opt for quality stocks with durable profits. In terms of fixed income, investors should anticipate Treasury yields will be biased higher as the Fed continues to remove policy accommodation against a backdrop of higher inflation, making active flexible bonds a good choice. And lastly, investors should recognize the path ahead is filled with uncertainty as markets recalibrate geopolitical risks, central bank moves, and continued COVID-19 woes, making it critical for investors to have well-diversified portfolios to navigate the volatility ahead.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.