Market Recap – Week Ending March 22

Stocks Climb Higher; PCE Price Index on Friday

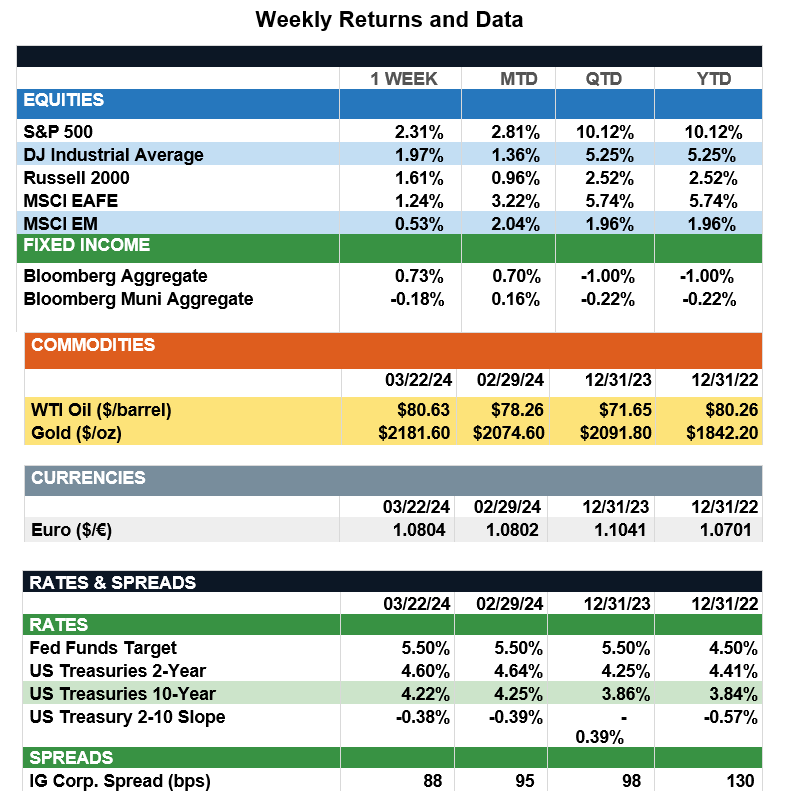

Overview: Stocks rose across the world last week as the Federal Reserve kept interest rates unchanged for the fifth consecutive meeting, and investor sentiment remained positive toward the ongoing technology rally in the markets. Here in the U.S., the S&P 500 index finished the week higher by 2.3% and the Nasdaq Composite rose 2.9% as markets are on track for a fifth consecutive month of positive returns. In bonds, interest rates fell as investors reacted positively to Fed data that showed an expectation of three rate cuts over the course of the year, which would result in a fed funds rate of 4.50%-4.75% at year-end if realized. Both 2-year and 10-year Treasury notes declined by about 10 basis points on the week to finish at yields of 4.60% and 4.22%, respectively. This week, markets will look for further insight into the path of inflation from the February personal income and consumption report, released Friday morning. The report contains the personal consumption expenditure data (PCE Price Index) that is the Fed’s preferred inflation gauge. Given the Good Friday holiday, market reaction to this data will be determined the following Monday as we begin April in the markets.

Update on Federal Reserve Projections (from JP Morgan): U.S. 10-year Treasury yields have increased 34 basis points year-to-date and have remained above 4% since early February. Yet over the same period, stocks have rallied 10%. At first glance, this dynamic may seem counterintuitive because high and rising interest rates are typically associated with weaker equity market performance. However, in today’s market, this relationship has deteriorated because investors have interpreted the rise in interest rates as a reflection of resilient economic activity, accompanied by expectations for robust profit growth. The market’s confidence was reinforced after last week’s FOMC meeting, as the committee’s updates to its Summary of Economic Projections (SEP) illustrated a rosier economic outlook. Real GDP growth projections were revised upward from below-trend growth rates in December. The year-end unemployment rate forecast was revised downward for 2024 and kept unchanged for 2025. Headline PCE projections were left unchanged at 2.4% for year-end 2024, but core PCE projections did increase slightly to 2.6%. Despite the increase in core PCE projections, in January headline and core PCE grew 2.4% and 2.8% y/y, respectively, highlighting we already are close to meeting the FOMC’s expectations. As such, the committee’s policy rate projections continued to signal three rate cuts this year but a downward revised three cuts in 2025 as the economy and labor market are expected to remain healthy. For equities, the key takeaway is that interest rates will likely stay higher for longer given the gradual pace of policy rate cuts laid out in the SEP. In an environment of higher rates and return-to-trend growth, quality will be key, particularly as valuations remain stretched and earnings estimates are downgraded. Investors should focus on attractively priced stocks with reliable revenue streams, prudent cost management, and low interest rate exposure.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg, CNBC

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.