Market Recap – Week ending Mar. 24

Stocks Higher, Bond Yields Volatile; PCE Data on Friday

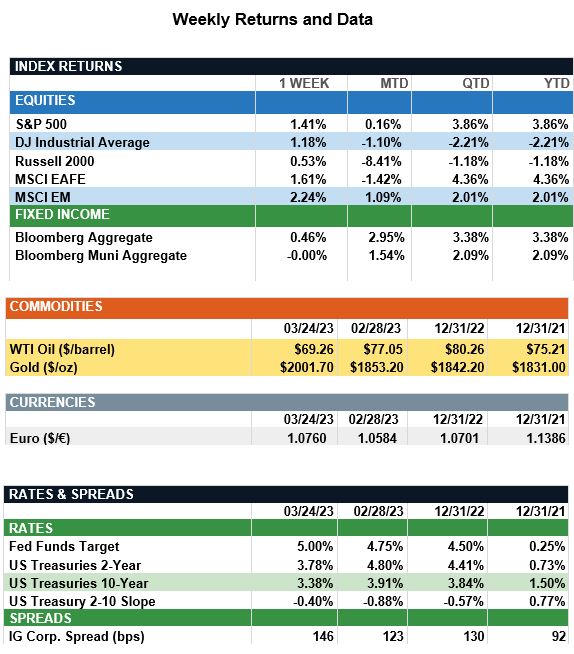

Overview: Global stocks were higher last week amidst rate hikes by both the Federal Reserve and Bank of England. In the U.S., the S&P 500 was higher by about 1.4% while international stocks, measured by the MSCI EAFE index, were higher by about 1.6%. As anticipated, the Federal Reserve raised the target for the federal funds rate by 0.25% (25 basis points), marking the ninth rate hike over the past year. Elsewhere, several central banks in the Euro area hiked interest rates despite stress in the banking sector. The Swiss National Bank hiked rates by 0.50%, while the Bank of England implemented a 0.25% hike. In the bond markets, yields remained volatile last week, with the 2-Year and 10-Year U.S. Treasury yields finishing the week at 3.78% and 3.38%, respectively. For perspective, the 2-year Treasury note has fallen in yield by more than 1% since the end of February, having ended February at a yield of 4.80%. For the time being, actions by global central banks and the U.S. government have helped ease worries surrounding recent turmoil in the banking sector. Looking forward to this week, investors will keep a close eye on the Personal Consumption Expenditures (PCE) price index due out Friday. Economists expect both the headline and core price index to show signs that inflation is continuing to slow.

Update on Interest Rates (from JP Morgan): March madness had a different connotation this year as investors faced market volatility and renewed uncertainties brought upon by a regional bank crisis. Last week, the March FOMC meeting revealed a cautious but steadfast Fed, with an additional 25bp rate hike but dovish forward guidance signaling a forthcoming end to the hiking cycle. Now, over a year into tightening, the Fed has raised rates by 4.75%, well into restrictive territory, and financial conditions have tightened meaningfully, with housing, manufacturing and markets all experiencing corrections in the past year. A further tightening in lending standards due to banking system pressures looks set to do the rest of the Fed’s job for them, dragging on economic growth and inflation but reducing the risk of further rate hikes.

While the odds of a U.S. recession have increased in light of all this, the risk outlook for the markets is becoming more balanced. Monetary policy should pose less of a headwind for stocks going forward. Economic data is moving in the right direction and the slowdown in inflation, wages and activity should become more pronounced in the coming months. Moreover, if the outlook worsens, the Fed could ease monetary policy, which could provide significant support to financial markets. Meanwhile, the investment landscape still presents opportunities. Bonds can provide portfolios with attractive income and some capital appreciation when the Fed eventually cuts rates. An emphasis on quality is important, but broadly speaking, equity markets tend to perform well in the 12 months following an end of a tightening cycle. By no means are we looking at clear skies yet, but calmer waters after a tumultuous March could provide support for balanced portfolios in the remainder of the year.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.