Market Recap – Week Ending 03.25.22

Market Recap – Week ended March 25

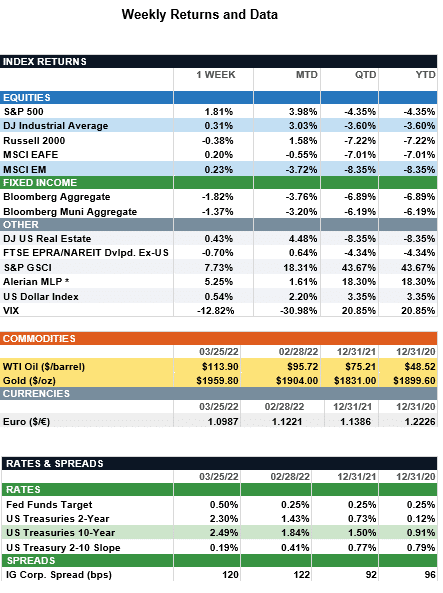

Overview: Stocks across the globe were generally higher last week as geopolitical concerns continued to fuel volatility in the markets. In the U.S., the S&P 500 index was up for a second consecutive week, closing 1.8% higher. In the bond markets, yields moved higher with the 2-year and 10-year Treasuries finishing the week at 2.30% and 2.49%, respectively. Yields rose on oil price concerns and indications of a labor market strength as workers rejoin the workforce and layoffs remain low. U.S. jobless claims were reported at a 50-year low of 187,000 for the past week, below consensus and down from 214,000 the week before. Record-low claims may signal a robust labor market that may continue to contribute to pressures on wage inflation. The Federal Reserve has indicated it will consider more aggressive rate hikes if needed, and the fight against inflation will continue to be top-of-mind for investors. As of now, futures markets are pricing in about a 70% chance of a 50-basis point (0.50%) hike in the May meeting of the Fed, with about nine total quarter-point hikes expected for 2022. This would result in an ending short-term funds rate of about 2.50% at the end of the year, still low by historical standards.

Global Economic Update (from JP Morgan): Prior to the Russian invasion of Ukraine, economic signals were encouraging through February as the Omicron wave retreated and supply chains began to improve. Looking at March flash PMIs, the relaxation of pandemic restrictions helped business activity weather the initial shock from the war. Headline PMIs were surprisingly resilient with growth gaining momentum despite hot inflation and geopolitical uncertainty. The U.S. marched further into expansion at 58.5 (+2.6pt m/m), while Japan saw a meaningful move back toward expansion, jumping 3.5pt m/m to 49.3. Despite closer geographic and economic ties to the conflict, Eurozone and UK growth held its ground at 54.5 and 59.7 respectively.

Beneath the strong headline prints, a common theme was surging costs. In March, already elevated input costs were boosted by a barrage of sanctions that impacted commodities and energy markets and further constrained supply chains. In Europe, average input prices saw a new peak of 81.6 (+9.5% m/m), notching their fastest ever monthly ascent. Japan’s input costs remained elevated, edging down 0.1pt from their record high last month. In the U.S., input costs rose 1.3pt but stayed below last December’s peak. While this rise in manufacturing prices will inevitably pass through to consumers and delay peak inflation, it should not completely deteriorate the growth outlook. It is important to remember the U.S. and Europe are coming into this with very good fundamentals and strong consumer balance sheets. Additionally, several European countries have announced fiscal measures to further offset rising costs. While growth may be clipped by higher inflation in the near term, investors should not be dissuaded, but rather stay in the market and take a diversified approach, seeking the balance between value vs. growth and international vs. domestic.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.