Market Recap – Week ending Mar. 31

Positive End to First Quarter; Encouraging Inflation Data

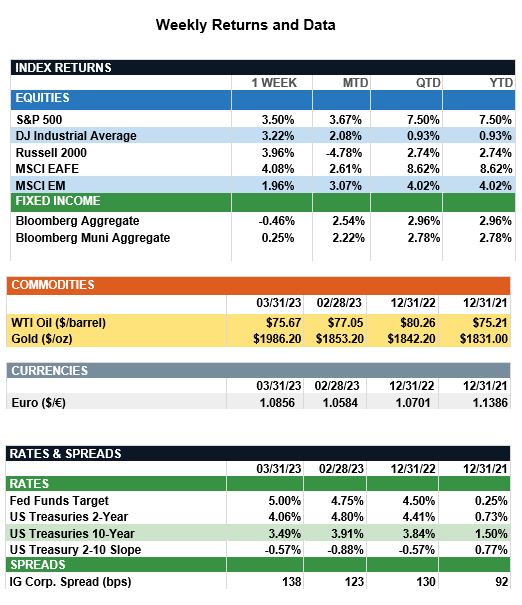

Overview: Stocks across the globe rose last week to finish a volatile first quarter in positive territory for the year. International developed stocks (MSCI EAFE) led the way, up 8.6%, followed in the U.S. by the S&P 500 Index, up 7.5%, and emerging markets (MSCI EM) which recorded a 4% return for the quarter. Bond returns were positive as well, with the Bloomberg taxable and municipal indices up 3% and 2.8%, respectively, for the quarter. Markets now expect the Federal Reserve to be close to the end of raising interest rates. Futures markets (Fed Watch data) now are expecting about a 60% chance of one more quarter-point (0.25%) rate hike at the Fed meeting in May, taking the terminal fed funds rate to a range of 5.00%-5.25%. Investors were encouraged on Friday by better-than-expected inflation data, as price pressures continue to trend downward. The February core personal consumption (PCE) price index, the Fed’s preferred measure of inflation, increased by 4.6% year-over-year, below consensus expectations. Importantly, core PCE services excluding housing had its smallest increase in February in nine months. This week, focus will be on the employment report to be released on Friday, where expectations are for 240,000 new jobs and unemployment to remain near a 50-year low of 3.6%. Key data from this jobs report will include a measure of wage inflation that is important to the Fed. This comes in the form of year-over-year average hourly earnings, which are expected to increase by 4.3%, down from 4.6% in February.

More on First Quarter Performance (from JP Morgan): Market volatility persisted during 1Q23, but several of 2022’s underperformers experienced a notable turnaround, highlighting investors’ willingness to look beyond near-term challenges and to front run a dovish shift in monetary policy. From a performance perspective, internationally developed market equities led the way, bolstered by cheaper relative valuations and surprisingly robust earnings. Well-capitalized European financials benefited from the return to a positive interest rate environment, while industrials were propped up by lower-than-feared energy costs. Emerging market equities also experienced gains, rising by 4%, as China’s reopening looks set to benefit from consumers tapping into excess savings amassed during lockdown. Turning to U.S. equities, large caps rose by 7.5% and small caps rose by 2.7%. This divergent performance can be attributed to the higher weight of financials and lower weight of technology in the small-cap index relative to the large-cap index. Amid the regional banking crisis, investors leaned into tech relative to financials, particularly as technology companies had already taken steps to optimize costs and defend margins. Turning to fixed income, the prospect of a dovish shift by the Fed in response to the banking crisis led yields to decline, with U.S. fixed income finishing the quarter up 3% and global high yield up 3.1%. Lastly, REITs edged up 1.5%, supported by a slight improvement in mortgage rates and modest declines in home prices; in contrast, commodities fell by 8%, primarily due to lower energy prices.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.