Market Recap – Week Ending 04.01.22

Market Recap – Week ended April 1

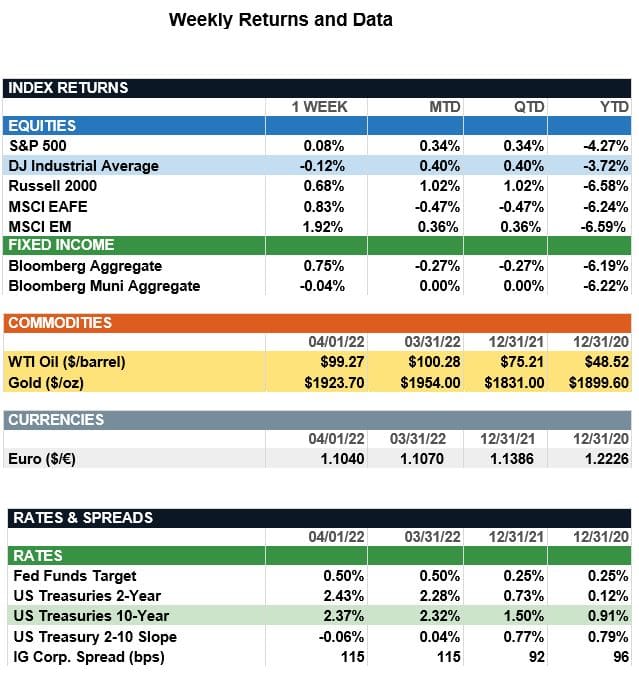

Overview: International stock traded higher last week, led by emerging markets (MSCI EM) up 1.9%, and developed stocks (MSCI EAFE) trading 0.8% higher. In the U.S., the S&P 500 index was up a marginal 0.1%, as inflation concerns continued and investors weighed developments in Ukraine. In the bond markets, the 10-year Treasury ended the week 0.12% lower in yield to finish the week at 2.37%, while the 2-year Treasury rose in yield to 2.43%. The short-maturity part of the Treasury curve now is pricing in accelerated Federal Reserve tightening, with a total of nine more one-quarter-point hikes expected by the end of 2022. This has led to an inverted curve between the 2-year and 10-year Treasury yields, often signaling a recession. While acknowledging an inverted yield curve has historically been a harbinger of recession, the time lag between an inverted curve and a recession has ranged from 7-35 months (Goldman Sachs) while the S&P 500 index has continued to produce positive returns on average. In addition, it is our view that quantitative easing, where the Fed has purchased longer-term bonds from the market, has artificially held down yields at the long end of the curve. In economic news, the final estimate for U.S. GDP for the fourth quarter of 2021 was lowered to 6.9%, resulting in full-year GDP growth of 5.7%. This reflected the fastest calendar-year growth in almost 40 years. Inflation continues to run hot, with U.S. core personal consumption expenditures (PCE index) increasing 5.4% in March, the highest level since 1983, and well above the Fed’s long-term target of 2%. The labor market continues to be strong, with nonfarm payrolls reporting 431,000 new jobs for the past month, with the unemployment rate falling to a pandemic low of 3.6%. The report marks the 15th consecutive month of workforce expansion.

Update on Returns (from JP Morgan): Asset class returns in 1Q22 were impacted by heightened geopolitical tensions, tighter monetary policy, and divergence in COVID-19 policies across regions. In terms of performance, commodities led the way with a 1Q22 return of 25.5%, as import bans on Russian oil along with only a gradual improvement in supply chains have boosted energy, food, and raw materials prices. Equities, overall, had a difficult quarter due to higher rates challenging valuations, and fears that inflation may put a dent in consumer spending and earnings. Within equities, large caps finished the first quarter down 4.6%, while their small-cap peers ended the period down 7.5%. Similarly, higher interest rates have begun to cool a hot real estate market, with REITs declining 5.3% in 1Q22. However, at the industry level, we did see positive performances among lodging/resorts (+6.9%) and offices (+2.8%), as they continue to benefit from the cyclical rebound and easing of economic restrictions.”

Moving to international markets, DM equity and EM equity decreased 5.8% and 6.9%, respectively, in 1Q22. The conflict in Ukraine weighed heavily on European markets, with the region’s growth estimates cut significantly in the wake of the Russian invasion of Ukraine. Additionally, emerging markets, particularly China, have suffered, as governments continued to impose COVID-19 lockdowns. Turning to bonds, U.S. fixed income markets declined 5.9% over the first three months of 2022, as the Federal Reserve moved forward with hiking interest rates and markets anticipated further tightening through year-end. Lastly, global high yield decreased 5.7% due to the flight to quality stemming from the Russia-Ukraine conflict and continued downgrades and defaults in the Chinese property sector.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.