Market Recap – Week Ending 04.08.22

Market Recap – Week ended April 8

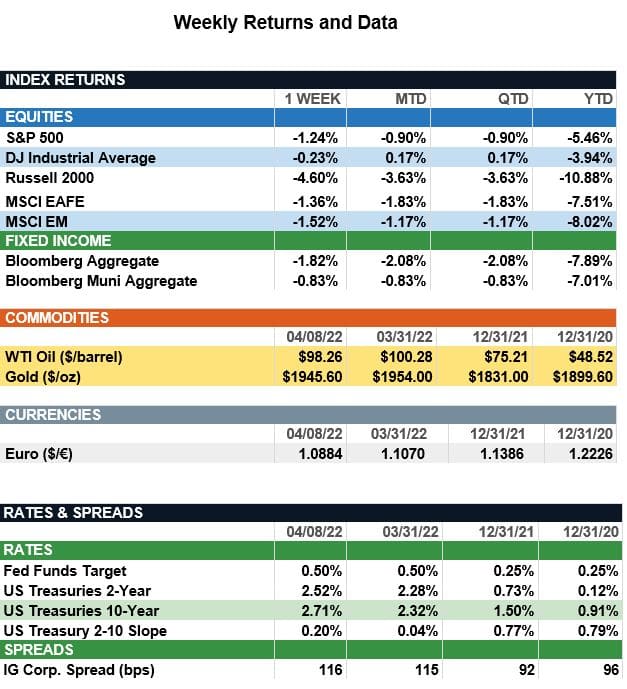

Overview: Stocks worldwide were lower last week, with the S&P 500 index down 1.2% on the week. In the U.S., investors focused on the release of the March FOMC meeting minutes, which indicated more aggressive monetary tightening from the Federal Reserve. In addition to hiking short-rates, the minutes indicated the potential for a monthly $95 billion reduction in the Fed’s balance sheet beginning in May. In bonds, the 10-year Treasury yield ended the week 0.34% higher at 2.71%. The yield on the 10-year Treasury has increased from a level of 1.50% at the beginning of the year. Meanwhile, the 2-year Treasury finished the week at a yield of 2.52%. Thus, the spread between the yield curve for 2-year and 10-year Treasuries is now a positive 0.19%, reducing concerns of an inverted curve predicting a recession.

In economic news, the U.S. Purchasing Managers’ Index (PMI) reported a level of 58.3 in March, ending three monthly declines. The PMI provides advanced insight into the services sector, which gives investors a better understanding of business conditions and the economic backdrop of various markets, and the stronger number reflects continued re-openings since the impacts of COVID-19 as the service economy strengthens. This week, focus will be on consumer prices (CPI) reported Tuesday, where the consensus is for headline CPI to rise 8.4% on a year-over-year basis.

Commodity Prices and the War (from JP Morgan): Apart from the horrific direct human impacts of the Russian invasion of Ukraine, its indirect effect of boosting commodity prices in general and food prices, in particular, will have serious consequences for consumers globally. Russia and Ukraine together account for nearly 30% of global wheat exports and 18% of corn. Russia also is a leading exporter of fertilizer, which could have important implications for a broad range of crops. The USDA recently revised its annual forecast for “food at home” inflation to a range of 5.5%-6.5% by the end of 2022, after prices already rose by a record 6.8% y/y in February. Food inflation is regressive since lower-income households spend more on food as a share of total spending than higher-income households. These households may have some relief though, as recent wage gains have been highest for the lowest-paid workers. We believe wage growth will prove to be sticky while food and energy inflation should prove more transitory. Therefore, it may be that lower-income households eventually will be left in a better position, with stronger wage growth as food and energy inflation fades. However, while lower-income households in the U.S. may have some protection, the same cannot be said for low-income households globally. While food accounts for 12% of consumer spending in the U.S., it accounts for 40% in sub-Saharan Africa, for instance. Tragically, some of the heaviest economic impacts of the war will fall on the poorest populations globally, until hostilities subside or global agricultural production expands to fill this supply gap.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.