Market Recap – Week Ending 04.14.22

Market Recap – Week ended April 14

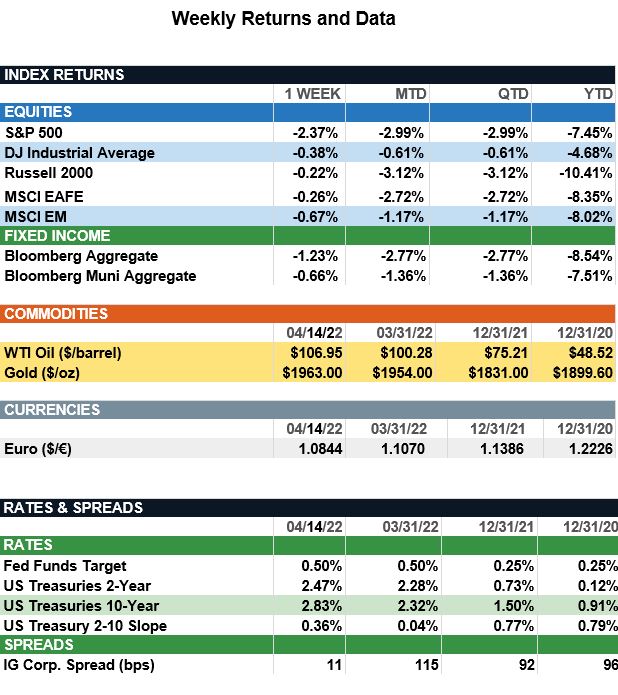

Overview: Stocks were lower last week as investors continue to monitor inflation and interest rates. Last week, markets digested two important inflation readings – the Consumer Price Index (CPI) and producer prices (PPI). CPI came in at 8.5%, in line with expectations, while PPI reported at 11.2% year-over-year, the highest on record. There was some good news as core CPI (ex-food and energy) was 6.5%, below the forecast of 6.6%, giving some hope that inflation may have peaked.

All eyes are now on the Federal Reserve policy. As the Fed signals monetary tightening to fight inflation, markets now are pricing in a 90% chance of a 50 bp tightening at the next Fed meeting on May 4-5, with an expectation of a 2.50% funds-rate by the end of this year. Early on Monday, April 18, the 10-year Treasury yield reached the highest level since late 2018, trading as high as 2.87%. For reference, the 10-year yield began the year at 1.50% and was as low as 1.71% at the beginning of March. As investors look for signs of the effects of inflation and interest rates on the economy, key data this week will be housing numbers (Tuesday and Wednesday) and the purchaser’s managers (PMI) report on Friday.

Update of Inflation (from JP Morgan): While consumer prices were certainly very hot in March (Headline CPI +1.2% m/m, +8.5% y/y), they were no worse than feared. The Russian invasion of Ukraine continued to weigh heavily on energy (+11.0% m/m) and food (+1.0% m/m) prices. Together, they were responsible for 82% of the m/m increase and 40% of the y/y increase. Excluding food and energy, core CPI (+0.3% m/m, +6.5% y/y) moderated by more than expected and saw its slowest monthly gain since September 2021. Price gains in durable goods like used vehicles (-3.8% m/m) showed early signs of easing. Despite this, core services (+0.6% m/m) remained sticky as owners’ equivalent rent rose 0.4% m/m and re-opening sectors such as transportation (+2.0% m/m), lodging (+3.3% m/m) and airlines (+10.7% m/m) stayed hot. Though the March CPI print was modestly encouraging, inflation still remains extremely firm. It continues to weigh heavily on business sentiment and will be an important theme to watch as 1Q earnings roll in. According to the National Federation of Independent Business small business’ optimism index, inflation now trumps quality of labor as the single-most important problem business owners face with 72% of firms saying they are being forced to raise their selling prices. All and all, March’s CPI report still warrants an aggressive Fed action in the months ahead to cool down consumer prices. Accordingly, the market is pricing in a 90%+ likelihood of a 50 bps hike in May and more than eight hikes by year end. Looking ahead, if this is peak inflation and we begin to see softening prints alongside signs that rate hikes are slowing economic activity, that should take some pressure off the Fed. But for now, make sure portfolios are poised to take on rate hikes by opting for high-quality stocks with strong dividend potential, high-quality and shorter-duration bonds for portfolio ballast and alternatives for diversification.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.