Market Recap – Week ending April 14

Markets React Positively to CPI Data; Earnings Reports Beating Estimates

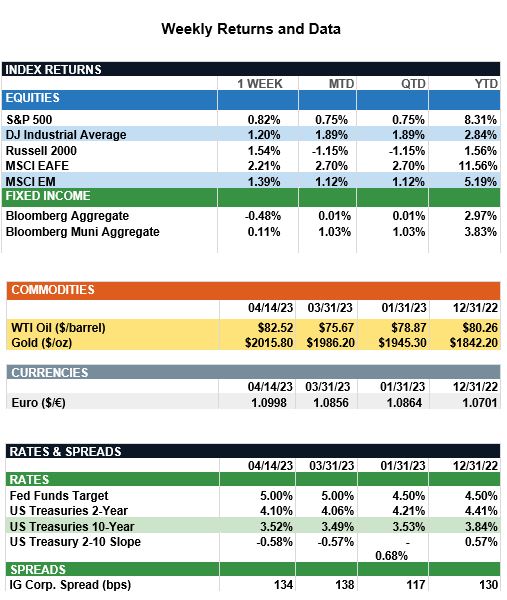

Overview: Stocks rose across the major world indices last week, led by international developed (MSCI EAFE) up 2.4%, and emerging markets (MSIC EM) higher by 1.4%. In the U.S., the S&P 500 index rose 0.8%. Markets reacted positively to a decline in Consumer Prices Index (CPI) headline inflation and began the evaluation of first-quarter earnings releases with the initial focus on the financial sector. On the earnings front, consensus estimates are for a 7% decline in first-quarter earnings for S&P 500 companies as investors have braced for a weak earnings season. Yet data from Bank of America suggests this earnings season may already be better than expected with 90% of the companies that reported during the first week beating their first-quarter estimates. U.S. inflation showed signs of easing in March with headline CPI reported at 5.0% year-over-year, below consensus expectations and significantly lower than the 6.0% reading the prior month. A significant decline came from housing/shelter inflation as higher existing rents originated last year reset lower. Turning to the Federal Reserve, minutes from the latest Fed meeting showed the committee now expects a mild recession later this year with GDP growth for the year expected to be around 0.4% for 2023. The initial estimate of first-quarter growth will come April 27 with the forecast from the Atlanta Fed (GDPNow model) showing a latest estimate of 2.5% GDP growth for the quarter. Markets are now pricing in one more 0.25% (25 bp) rate hike at the Fed meeting in May, with the peak funds rate now expected to be 5.00% - 5.25%.

Update on Earnings (from JP Morgan): The 1Q 2023 earnings season is underway with the large U.S. banks releasing results last Friday. Current analyst estimates are tracking operating earnings per share (EPS) of $49.54 ($39.73 ex-financials), representing y/y growth of 0.4% and a q/q decline of 1.6%. This estimate reflects slowing demand offsetting the benefits of easing macro headwinds. Despite improved global supply chains and moderating cost pressures, increased recession risk and weak consumer sentiment weighed on demand, and a persistently strong dollar likely limited foreign sales. At the sector level, these estimates suggest a change in leadership. The boost from the energy sector looks set to fade due to normalizing commodity prices. The current estimate of 7.6% y/y earnings growth for the sector represents a sharp deceleration compared to recent quarters. In other cyclical sectors, materials earnings likely will contract, while resilient demand for air travel and commercial services should support industrials. The tide also may turn for financials as moderating loan loss provisions should contribute to positive earnings growth. That said, slowing loan growth, moderating net interest margins and weak M&A activity remain headwinds. The growth sectors are facing headwinds of their own, as falling hardware demand and less advertising and discretionary spending should weigh on information technology and communication services, respectively. Lastly, persistent demand for services and core goods should support both consumer sectors with consumer discretionary specifically benefiting from China’s reopening as well as strength in travel and lodging. As the U.S. economy appears to be edging closer to a recession, current earnings estimates remain too high. While the prospect of lower interest rates has supported equity markets so far this year, volatility may pick up as earnings estimates are revised down.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg, Bank of America

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.