Market Recap – Week ending April 21

Investors Watching Earnings Data; GDP, PCE Price Index Due This Week

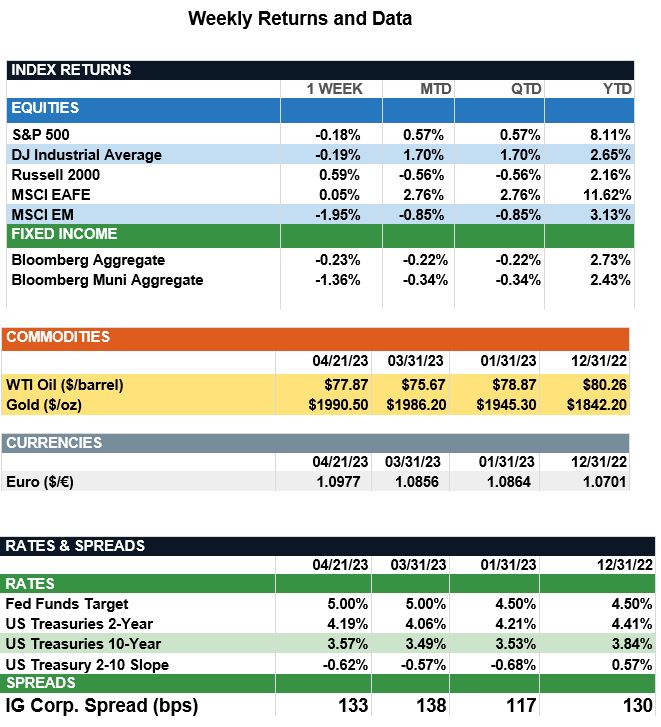

Overview: Global stocks were largely unchanged last week in quiet trade as investors digested a slew of corporate earnings and look ahead to the Federal Reserve meeting on May 2-3. In the U.S., the S&P 500 index finished lower by 0.2%, as according to Fed Watch data markets now are pricing in about a 90% probability of a 0.25% rate hike at the upcoming Fed meeting. In bonds, interest rates rose slightly with the 2-year and 10-year Treasury notes finishing the week at yields of 4.19% and 3.57%, respectively. Focus this week will continue on earnings with results from technology companies such as Alphabet, Meta, Amazon, and Microsoft highlighting a busy week of reports. So far, according to Factset, about 76% of S&P 500 companies with reported earnings through Friday have beat earnings estimates for the first quarter of 2023. At the same time, according to Refinitiv data, first-quarter earnings for S&P 500 companies are estimated to decline an overall 5.2%. As we now are about halfway through the earnings season, investors will continue to evaluate both earnings and forward guidance for corporate profits as recession concerns remain. Economic focus this week will be on first-quarter Gross Domestic Product (GDP) due to be reported on Thursday, April 27, where the consensus is for the economy to have expanded at an annualized rate of 2.0% for the first quarter. In addition, personal income and outlays will be reported on Friday. This report includes the PCE Price Index, the preferred measure of inflation for the Fed. The headline PCE Index is expected to fall to 4.2% in March, from 5.0% the prior month, as inflationary pressures continue to decline.

Update on Housing (from JP Morgan): Last month’s CPI report showed shelter prices growing at the slowest rate since November 2022 at 0.6% m/m. Despite still-elevated y/y growth of 8.2%, this reading was an encouraging sign the CPI measure is finally beginning to factor in the housing market slowdown that started last year. On the back of rising mortgage rates, construction activity cratered in 2H 2022, with housing starts falling by 40% and 14% annualized in 3Q22 and 4Q22, respectively. Most recently, March housing data has come in mixed, pointing toward a stabilizing housing market as opposed to an improving one after very positive February data. Housing starts dropped 0.8% m/m to 1.42M, slightly above forecasts, while building permits were down 8.8% m/m with both figures having risen more than 5% year-to-date. At the same time, mortgage applications continue to be weak as 30-year fixed mortgage rates remain elevated at 6.4% as of last Friday (but below last fall’s peak of 7.1%). However, mortgage rates may not need to decline significantly for housing demand to stabilize, as higher-for-longer rate expectations may be enough to convince potential buyers to enter the market. Looking ahead, the April NAHB survey increased to its highest level since September, signaling that builders are becoming more optimistic about home buyer activity. While a recession could lead to further declines in demand, the acute drag from housing activity on the economy seems to be behind us. For inflation, the lagged impact of last year’s housing contraction should continue to show up in softer shelter prices as the year goes on.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg, Factset, Refinitiv

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.