Market Recap – Week ending April 28

Fed Rate Hike Expected This Week; Mixed Economic Data

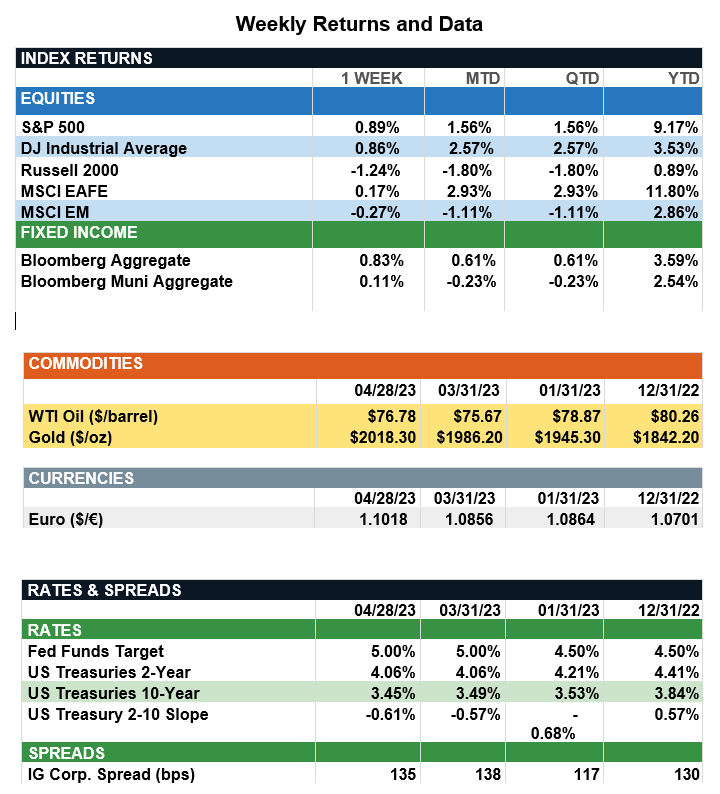

Overview: U.S. stocks finished the week higher in volatile trade last week as strong technology earnings helped the S&P 500 index to finish 0.9% higher for the week. For April, the S&P 500 index finished higher by 1.6%, and now is up about 9% for in 2023. International stocks also finished April in positive territory for the year. International developed (MSCI EAFE) stocks are up 11.8% and emerging markets (MSCI EM) are higher by 2.9% in total return through the first four months of the year. In the bond markets, both taxable and municipal indices are higher for the year, with the Bloomberg Aggregate (taxable) index up 3.6%, and Bloomberg Muni up 2.5% through April, as declining interest rates have fueled positive price performance for bonds. Markets begin May focused on the Federal Reserve meeting May 2-3, where the Fed is widely expected to raise the fed funds rate by 0.25% (25bp), to a target range of 5.00% to 5.25% (see update below). Markets recognize the Fed is facing the challenge of bringing down inflation without a dramatic growth slowdown, with data across the board showing growth has slowed. The latest example is U.S. real Gross Domestic Product (GDP), which rose 1.1% annualized in the first quarter, well below the consensus expectation of 2%. Though this GDP report was below expectations, a silver lining is consumer spending, where consumption increased by a robust 3.7% over the first quarter.

Update on Federal Funds Rate (from JP Morgan): At the March meeting, 17 of 18 FOMC participants believed the federal funds rate needs to be 25bps higher at the end of 2023 than its current target range of 4.75% to 5.00%. Going into this week’s meeting, the question is whether enough has changed over the last six weeks to convince a sufficient share of voting members to change their mind. Following early March’s regional bank stress, equity and bond market volatility has eased, while investors have gone from pricing in a 21% probability of a 25bps rate increase in May on March 13 to an 85% probability today. Economic data has been mixed, but the picture still broadly shows a resilient U.S. economy. Last week, 1Q GDP growth came in below consensus at a 1.1% annualized rate, with a sharp decline in inventory accumulation, continued contraction in housing and slowing business fixed investment, but strong 3.7% consumption growth. April’s business surveys continue to show a divergence between weakness in manufacturing and strength in services. Turning to the labor market, March’s jobs report showed job creation slowing but to a still strong 236,000, with ongoing moderation in wage growth for all workers to 4.2% year-over-year. Meanwhile, the Fed’s main inflation target, the headline PCE deflator, retreated to a year-over-year rate of 4.2% in March, down from a peak of 7.0% year-over-year last June. Still, with market volatility subsiding, real economic growth resilient and wages and inflation still elevated, it seems likely the Fed will deliver another 25bps hike this week. The question now is whether this will be the last one and, more importantly, when rate cuts might begin.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg. This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument. Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.