Market Recap – Week ending May 5

U.S. Stocks Lower; CPI Report on Wednesday

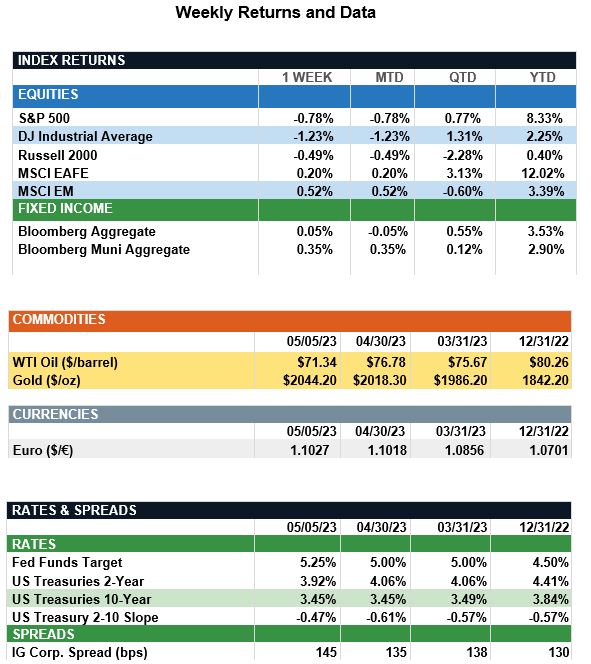

Overview: U.S. stocks finished the week lower in volatile trade last week as the Federal Reserve and European Central Bank delivered further interest-rate hikes. For the week, the S&P 500 finished about 0.78% lower, while the Dow Jones Industrial Average was lower by about 1.23%. International developed (MSCI EAFE) stocks managed to finish the week in positive territory, higher by 0.20%. For the year, international developed stocks now have rallied more than 12%. In emerging markets, the MSCI EM index was higher by 0.52% last week, buoyed by strength in Asian markets such as India and China. It was a mixed week for bonds, with the Bloomberg Aggregate (taxable) index lower by 0.05% while the Bloomberg Muni index was higher by 0.35%. On the heels of last week’s Federal Reserve meeting, investors will keep a close eye on CPI inflation report due Wednesday. Economists are expecting core inflation to show a year-over-year increase of 5.5%, modestly lower than last month’s reading of 5.6%. Futures markets no longer are pricing in any additional rate hikes from the Federal Reserve for the remainder of the year; however, a higher-than-expected inflation print could be expected to drive a significant amount of volatility in both stocks and bonds.

Update on the Economy (from JP Morgan): Last week, the Federal Reserve delivered what many expect to be the last interest-rate hike of this cycle, bringing the federal funds rate to a range of 5.00-5.25%. With the Fed now potentially on pause, at least for a while, investors are shifting their focus away from the risk of further Fed tightening and toward the risk of recession, as the fallout from the regional banking crisis casts a shadow on the economic outlook. Recent data have shown a loss of economic momentum, with declining job openings, tightening lending conditions and surveys indicating lower business spending and hiring plans. Yet, despite expectations for a slowdown, the April Jobs report showed better-than-expected payroll gains, a decrease in unemployment and an uptick in wage growth. The report overall was strong, though large downward revisions to the prior two months added a layer of softness to the recent trend. Still, while layoff announcements and unemployment claims have been rising in recent months, excess demand for workers has seemingly been enough to absorb those layoffs so far and keep unemployment at bay. Wage growth continues to be too high for the Fed’s comfort, but while wages may have bounced last month, compared to a year ago they still are steadily declining. Moreover, as the worsening economic outlook induces businesses to cut back on spending and hold off on hiring plans, it’s difficult to imagine wage growth can increase sustainably from here. Because of this, and the expected toll credit tightening will have on growth in the coming months, we still expect the Fed to stay on pause in June and potentially pivot to easing monetary policy in response to recession later this year.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.