Market Recap – Week ending May 12

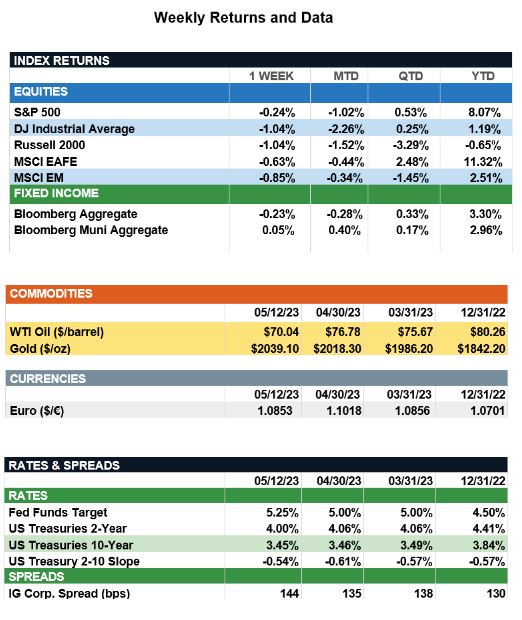

Overview: Stocks around the world were down marginally last week, as investors continue to evaluate the impact of the central bank tightening on growth and inflation. In the U.S., earnings releases and debt-ceiling talks continue to influence market returns and volatility with the S&P 500 index finishing the week down 0.2%. In the bond markets, yields have largely stabilized given the consensus of a pause in Federal Reserve tightening, with the 2-year and 10-year Treasury notes finishing the week at 4.00% and 3.45%, respectively. Bond yields have traded in a narrow range since the end of March, helping to add stability to the income markets. In economic data, core consumer prices (core CPI) were reported at 5.5% year-over-year in April, down from 5.6% in March. Key to the report was the downward trend continued in the housing and shelter sectors as pandemic rent concessions have diminished and growth in new rental pricing has slowed. Producer prices (PPI) slowed as well, with core PPI falling to 3.2% in April from 3.4% in March. Both the CPI and PPI reports show a continuing easing of pricing pressures, yet inflation still has a significant amount to decline before reaching the long-term Fed target of 2%. Looking forward to this week, markets will receive reports on retail sales, industrial production, and housing, all important inputs into the ongoing health of the economy, with more detail below.

Update on the Economy (from JP Morgan): Following the Federal Reserve’s (Fed’s) decision to raise the federal funds rate to a range of 5.00%-5.25%, investors scoured April’s CPI report and the 1Q Senior Loan Officer Survey in an attempt to get a sense of the Fed’s next steps. Although the survey showed only a slight increase in the share of domestic banks reporting tighter lending standards, there is more to this than meets the eye. Banks have been incrementally tightening lending standards over the past year, and well before stress in the banking system began to emerge. While the share of banks tightening has not eclipsed pandemic levels, demand for commercial loans has fallen below levels seen during the depths of the pandemic. This has been particularly true among the regional banks, which have increased lending costs amidst an uncertain economic outlook and recent deposit flight. The silver lining, however, is tighter lending standards weigh on economic growth by depressing credit demand, and typically lead inflation to decelerate with a lag of 4-6 quarters. As such, the full impact of the tighter credit conditions is yet to be felt, but the April CPI report suggested inflation is cooling, with year-over-year headline CPI moderating for the 10th consecutive month. Furthermore, after stripping out the volatile energy and lagging shelter components, services prices registered an increase of 0.11% on the month; this was the smallest increase since July 2022 and suggests even some of the sticky components are beginning to turn over. Looking ahead, further deceleration in inflation seems likely. However, the lagged impact of extremely tight monetary policy will begin to be felt more acutely and has raised the risk of recession later this year. As the growth/inflation mix begins to shift, it seems likely the Fed’s resolve to keep rates higher for longer will be tested.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.