Market Recap – Week Ending 05.13.22

Market Recap – Week ended May 13

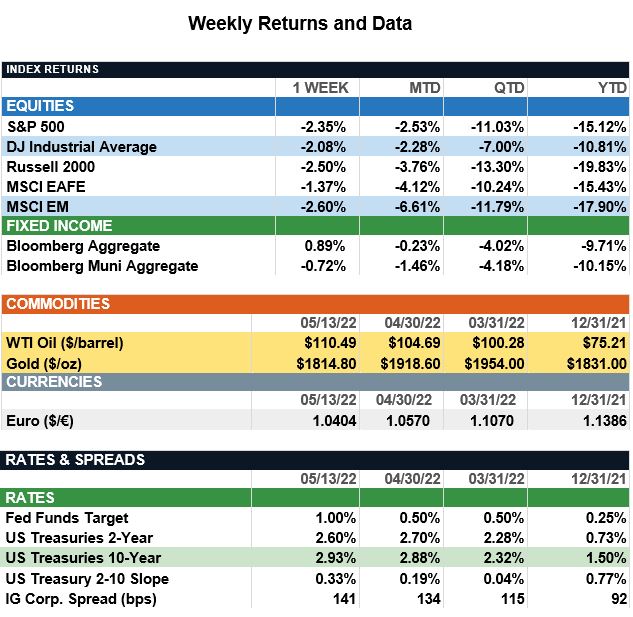

Overview: Stocks across the globe were lower last week, as markets continue to be challenged by a global economic slowdown given the COVID-19 lockdowns in China, the Russia-Ukraine war, and persistent inflation. In the U.S., the S&P 500 index was 2.4% lower on the week. On the inflation front, headline consumer prices (CPI) increased by 8.3% year-over-year in April, above expectations of 8.1%. As inflation continues to be a concern, investors looking for safety drove yields lower with the 10-year Treasury finishing the week 19 basis points lower (0.19%) at 2.93%. As detailed in the section below, the Federal Reserve likely will continue meaningful rate hikes with markets now expecting 50 basis point hikes (0.50%) at each of the next two Fed meetings.

Update on Inflation (from JP Morgan): Last week, investors’ hopes for signs of cooling U.S. inflation were dashed as the April CPI report showed inflation still running hot. High inflation is clearly weighing on consumer confidence and offers little hope the Fed will deviate from its projected aggressive path of rate hikes. Both headline CPI and core CPI came in above expectations at 0.3% m/m and 0.6% m/m, respectively. While declines in energy prices led to a moderation in headline CPI, core inflation accelerated as air fares, new vehicle prices and shelter costs rose solidly. Consumer sentiment also fell to a new 11-year low as persistent inflation and weakness in equity markets likely hurt confidence.

In response to these economic releases, markets saw another volatile week in what already has been a particularly volatile year. Higher interest rates, the war in Ukraine and persistent inflation have spared few asset classes from the selloff and while bonds typically provide ballast when equities head downward, a benchmark 60/40 stock-bond portfolio is down 14% year-to-date. It likely will take several inflation reports to determine whether prices are cooling enough for the Fed to dial back on tightening, and thus calm investor worries. However, while market volatility may continue, the selloff has brought stock valuations down to much more reasonable levels, while earnings estimates have remained resilient. Further, history suggests periods of gloom may be among the best times to buy equities. Indeed, following eight rather obvious troughs in consumer sentiment over the last 50 years, subsequent 12-month S&P 500 returns averaged almost 25%. Because of this, investors would be wise to keep their emotions in check and invest based on the logic of current valuations and long-term prospects rather than negative emotion in this difficult time.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.