Market Recap – Week ending May 19

Positive Week for Stocks; 1Q 2023 Earnings Have Surprised

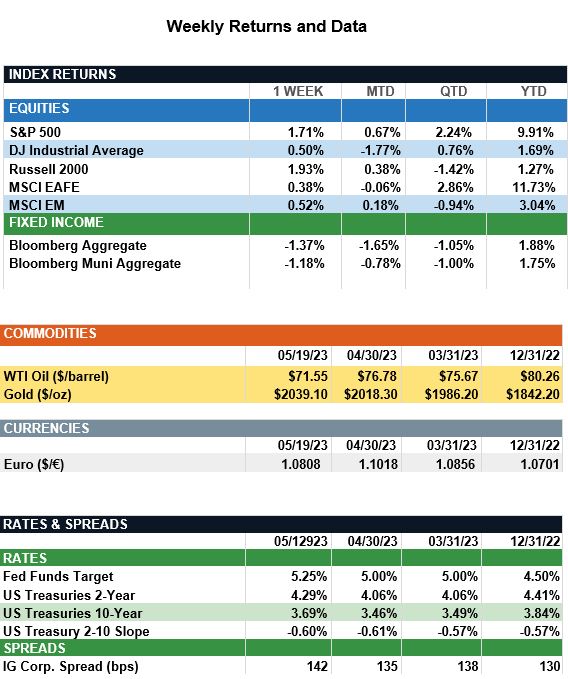

Overview: U.S. stocks led global indices higher last week, as optimism for a resolution of the debt ceiling helped fuel a mid-week rally. Here in the U.S., the S&P 500 index ended the week higher by 1.7%. International stocks finished in positive territory as well, as earnings in Europe exceeded expectations. International developed stocks (MSCI EAFE) and emerging markets (MSCI EM) were up 0.4% and 0.5%, respectively, for the week. In the bond markets, returns were negative for the week as Treasury yields rose in response to stronger-than-expected manufacturing and industrial production data. The 2-Year and 10-Year U.S. Treasury yields closed the week higher at 4.29% and 3.69%, respectively, both higher by about 0.25% over the month of May. In economic data, retail sales increased 0.4% in April as consumer spending remains fairly robust. Industrial production increased 0.5% in April, above expectations, and housing starts increased by 2.2% in April as both single-family and multi-family starts increased. Markets will continue to monitor declining inflation along with signs of ongoing economic growth to determine whether the Federal Reserve will pause rate hikes at the upcoming Fed meeting in June. According to FedWatch data, markets now are pricing in about an 80% chance that rates remain at the current 5.00%-5.25% level at the June 14 Fed meeting, with the expectation the Fed will begin to ease rates as early as September of this year.

Update on Earnings (from JP Morgan): Despite slower economic growth, 1Q23 S&P 500 earnings have surprised to the upside as economic momentum at the beginning of the year supported an expansion in profit margins. With more than 90% of the S&P 500’s market cap having reported, profit margins currently stand at 11.8%, a level of profitability that had been eclipsed only once in the pre-pandemic period. Earnings continue to find support in consumer spending, which accelerated to a q/q gain of 3.7% (SAAR) in 1Q23 due to increases in both goods and services. The strength in services demand has particularly buoyed earnings with the travel and food services-related industries within consumer discretionary and industrials recording significant growth in profits. Additionally, while the decrease in private inventory investment dragged on real GDP growth in 1Q23, this was a positive for earnings as it confirms companies are successfully working their way through bloated inventories. Elsewhere, higher interest rates drove an increase in net interest margins in the financials’ sector, which despite the ongoing turmoil with regional banks had a strong earnings season. Lastly, the cost side of the profit story also has improved. Many of the large tech companies, which are among the index’s largest constituents, now are focused on managing headcount and optimizing capital expenditures with both initiatives providing downside protection to earnings. Year-to-date, gains in the equity market have been driven by multiple growth due to the market’s expectations for rate cuts by the end of the year. However, looking ahead, if such expectations prove to be too dovish, any further gains in equities will be dependent on earnings.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.