Market Recap – Week Ending 05.27.22

Market Recap – Week ended May 27

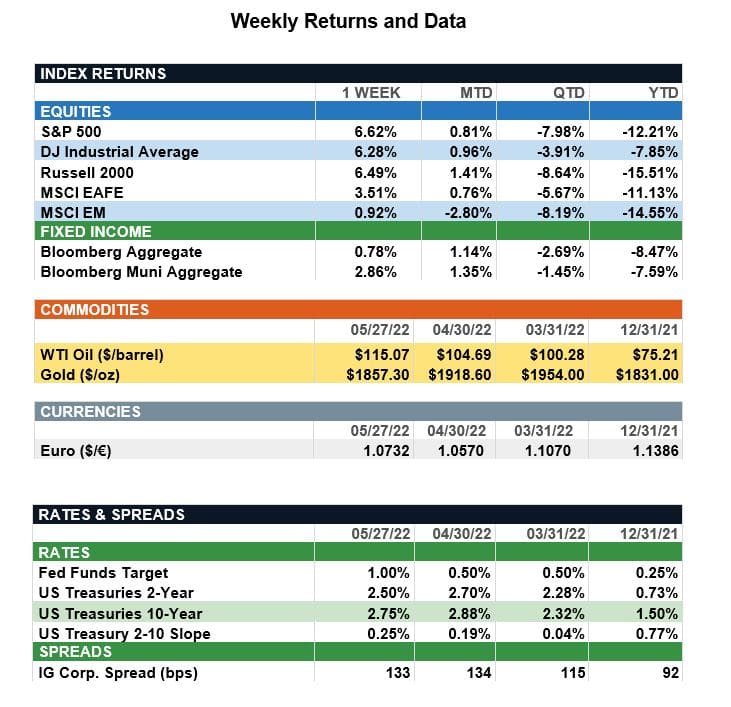

Overview: U.S. stocks ended a seven-week stretch of declines last week as some positive retail earnings helped investor sentiment. Meanwhile, the Federal Reserve released the minutes from their last meeting, which indicated further rate hikes to slow inflation. The Fed has indicated it may raise rates by 50 basis points (0.5%) for at least the next two meetings, as the central bank focuses on slowing the economy and bringing down inflation. Futures markets now are pricing in a total of about 2% further rate hikes over the remainder of 2022, with the ending short-term funds rate expected to be around 2.75%. Stocks across the globe finished in positive territory last week, with the S&P 500 index leading the way, up 6.6%. International developed stocks (MSCI EAFE) were up 3.5% for the week, buoyed by the announcement of stimulus plans by the United Kingdom. In commodities, oil prices rose on expectations of increased demand in the U.S. for the summer season, and the European Union’s resolve to ban Russian oil imports. Benchmark WTI crude oil finished the week at $115 per barrel, up from $76 per barrel at the start of 2022. In bonds, yields were lower on the week, with the 2-year and 10-year Treasury notes finishing the week at a yield of 2.50% and 2.75%, respectively. In economic data, the Federal Reserve’s preferred measure of inflation, core personal consumption expenditures (PCE index), rose 4.9% year-over-year in April, down from 5.2% in March. The elevated, yet improving, PCE index gives investors hope that price pressures could be peaking, and inflation may gradually improve over the remainder of the year.

Update on Manufacturing and Services (from JP Morgan): As illustrated by the Flash Purchasing Manager’s Index (PMI), growth stayed resilient in May, as lackluster manufacturing prints were offset by strong services showing. The U.S. headline composite index came in at 53.8 (vs. 56.0 in April), the eurozone at 54.9 (vs. 55.8), the UK at 51.8 (vs. 58.2) and Japan at 51.4 (vs. 51.1). Compared to April, the headline prints did cool a bit, but nonetheless remained expansionary. On the manufacturing side, input prices stayed elevated with the rate of cost inflation at manufacturers now sitting just a stone’s throw away from its all-time high. This should come as no surprise as we already have been seeing this messaging on the corporate side in 1Q earnings reports. The surge in prices continues to be driven by upticks in the prices for raw materials, as well as higher interest rates, fuel costs and higher transportation fees. On the services front, optimism among service sector firms strengthened with many anticipating that staffing and material shortages should begin to ease in 2H22. The loosening of COVID-19 restrictions continues to serve as a tailwind for overall growth, providing a boost to recreation activities and tourism. This was particularly true in the eurozone, which saw its second-strongest services expansion in the last eight months. While the post-pandemic growth momentum is beginning to moderate, we do not think it is coming to a screeching halt. As markets recalibrate to the evolving economic environment, expect continued volatility, and reduce risk levels accordingly by adding quality to portfolios through core bonds like investment-grade credit and defensive equity sectors like health care. Later in 2022, we should see support for earnings and the potential for better returns as uncertainty dissipates.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.