Market Recap – Week Ending May 3

Stocks Move Higher; Positive First-Quarter Earnings Reports

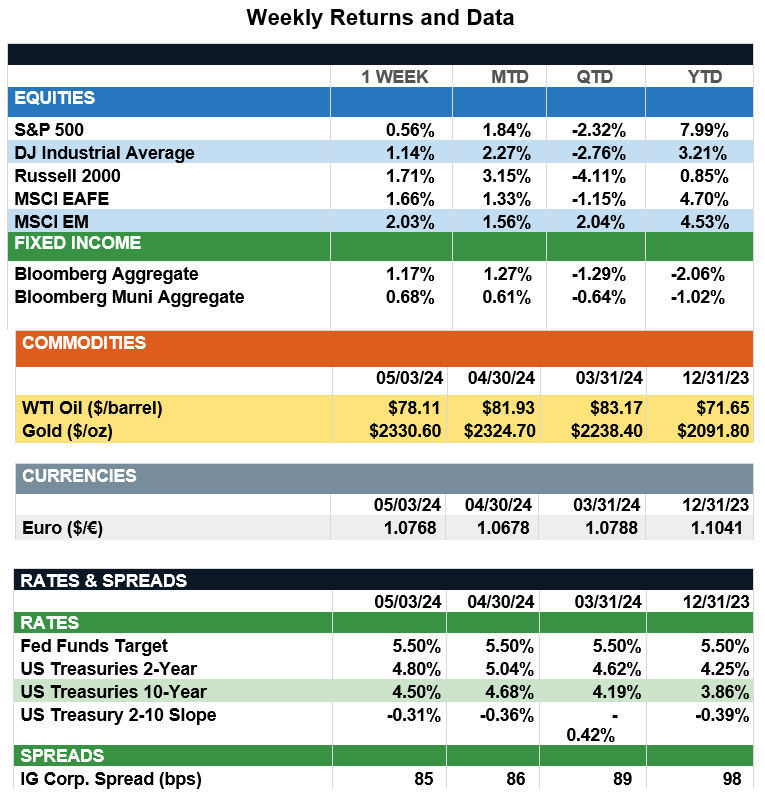

Overview: Stocks were higher around the world last week, led by emerging markets (MSCI EM) up 2.0%, and international developed (MSCI EAFE) higher by 1.7%. In the U.S., the S&P 500 index closed out April 4.0% lower, but recovered some of its losses last week, finishing the week 0.6% higher. Markets were buoyed on Friday by an employment report that showed the economy created 175,000 jobs in April, below expectations, and that wage inflation slowed from 4.1% to 3.9% on a year-over-year basis. In addition, the Federal Reserve left rates unchanged at its May meeting last week and announced it will start slowing the pace of their balance sheet reduction in June. Investors are encouraged by the prospect the Fed can engineer a soft landing of the economy while inflation continues on a downward trend. In the bond markets, the 2-Year and 10-Year U.S. Treasury yields finished lower at 4.80% and 4.50%, respectively, with Bloomberg taxable bond index up 1.2% on the week. With a relatively quiet economic calendar this week, focus will be on the final stages of the reporting of first-quarter earnings. Key companies set to report this week include Disney on Tuesday and Uber on Wednesday. According to Factset (as of May 3), 80% of S&P 500 companies have reported earnings for the first quarter, with 77% of these companies reporting beating earnings estimates. On a year-over-year basis, the S&P 500 is reporting its highest earnings growth rate since the second quarter of 2022, and both the percentage of S&P 500 companies reporting positive earnings surprises and the magnitude of earnings surprises are above their 10-year averages.

Update on Labor (from JP Morgan): Labor force participation rates in the U.S., Eurozone, and UK show each market is continuing to experience tightness with different underlying drivers. Remarkably, the U.S. has added 2.8 million jobs (1.8% growth) in the past year without a reacceleration in wage growth. In April, wages grew 3.9% y/y, the slowest pace since June 2021, and only 0.2% m/m. This is partly due to the strong recovery in participation rates in addition to a surge in immigration. In the Eurozone, the rebound in participation has been equally impressive. However, employment growth has been a less impressive 1.0% over the past year with less help from immigration. Finally, employment growth in the UK has been negative at 0.6%, due to less positive immigration trends and poor participation rates. During the pandemic, many decided they had saved enough to retire early or are experiencing long-term health issues that prevent them from working. In all three cases, inflation has continued to trend downward despite a tight labor market. While relatively weaker GDP growth in the Eurozone and UK may lead to more near-term policy easing, all three central banks should be able to cut rates by year-end. High-for-longer rates in the U.S. may prevent a dollar decline in the short run, but it could weaken once the Fed begins cutting rates, bolstering the dollar-denominated return from overseas assets. Consequently, while the April jobs report continues to show a healthy U.S. economy, investors should examine the opportunities that exist today in less buoyant, but also much less expensive, overseas markets.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg, Factset, CNBC

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.