Market Recap - Week Ended June 3

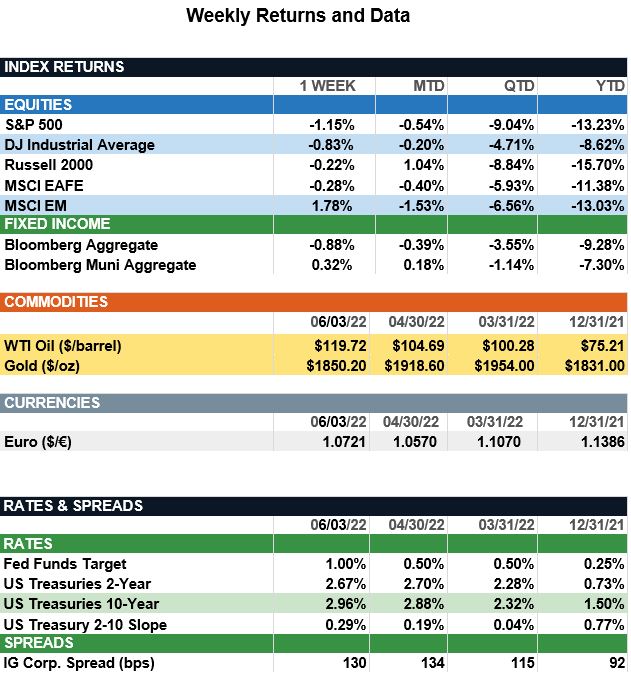

Overview: Global stock returns were mixed last week as volatility continues in the markets. Emerging market stocks (MSCI EM) finished the week 1.8% higher, while in the U.S. the S&P 500 index was down 1.1% for the week. In the bond markets, the new month started with a rise in 10-year Treasury yields as investors remain concerned over additional interest-rate hikes and persistent inflation. Focus is now on the Federal Reserve meeting next Tuesday and Wednesday, June 14-15, where the Fed is expected to raise short rates 50 basis points (0.50%) at the conclusion of their meeting. Futures markets are now pricing in a total of about 2% further rate hikes over the remainder of 2022, with the ending short-term funds rate expected to be around 2.75%. In economic news, the labor market continues to remain strong. Last Friday’s jobs report showed the addition of 390,000 new jobs in May, the 17th consecutive monthly gain. The unemployment rate remained at 3.6%, unchanged over the past three months. Trading this week began with positive news regarding China, with Beijing easing COVID-19 restrictions and announcing the easing of curbs on U.S.-listed technology firms. Upcoming focus this week will be on the consumer price report (CPI) due out on Friday, where headline inflation is expected to ease to 8.2% from an 8.3% reading the prior month. Although still elevated, a lower CPI reading may boost investor hopes that inflation has peaked.

Update on Employment (from JP Morgan): In an environment dominated by fears of recession or runaway inflation, the May Jobs report offers investors some comfort the economy can find a soft-landing path to avoid both. Businesses added a solid 390K non-farm jobs in May, thanks in part to a tick higher in labor force participation and labor supply flexibility. The unemployment rate also stayed at 3.6% for the third consecutive month, signaling the labor market is at least tightening more slowly. Notably, the labor force seems to be adjusting to a more normal economy as it adds jobs where most needed – construction, leisure and hospitality, and education – and sheds jobs where less needed – retail employment, as consumers switch spending from goods to services. The demand side of the labor equation is still running hot but shows its first signs of moderation, with JOLTS job openings falling from its record peak of 11.9K to 11.4K in April. Anecdotally, companies also seem to be positioning to reduce hiring efforts, with mentions of “layoffs” ticking higher in 1Q22 earnings call transcripts. However, economic data continue to show record-high hiring efforts and record-low layoffs pointing to a very tight labor market, with Challenger data showing companies announced 20.7K layoffs compared to 612.7K hiring announcements in May. Over the next few months, we expect job gains will continue to moderate as the pace of decline in unemployment reaches a floor slightly below its current 3.6% level. However, the Fed would welcome a cooling off in the labor market and, combined with a moderation in wage growth, such data may suggest the economy can find its footing on a path of slow and steady growth with low inflation, so long as the Fed has the patience to allow it.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s , Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.