Market Recap – Week ending June 9

Key Economic Data, Fed Meeting This Week

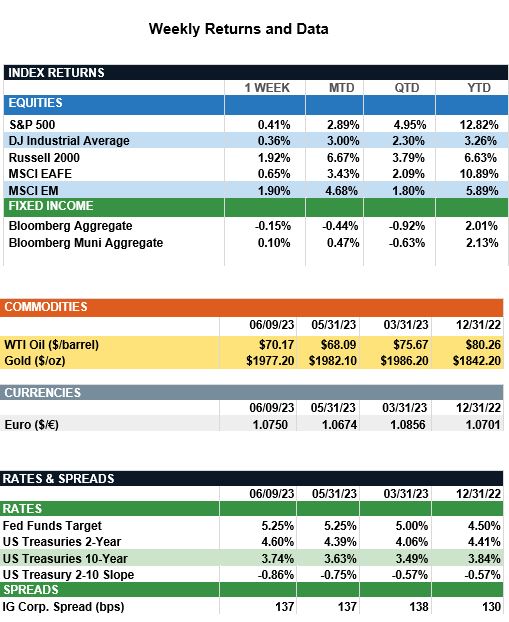

Overview: Stocks around the globe were higher last week, led by the 1.9% return of the emerging markets (MSCI EM) index. In the U.S., the S&P 500 index rose 0.4% in quiet trade as investors look forward to the Federal Reserve meeting this week. The broad-based S&P 500 index has risen for four consecutive weeks and now is about 20% higher in total return from its October 2022 lows. In the bond markets, yields were relatively unchanged last week with the 2-year and 10-year Treasury notes finishing the week at yields of 4.60% and 3.74%, respectively. Attention now turns to key economic data this week, beginning with consumer prices (CPI) Tuesday, and producer prices (PPI) Wednesday, followed by the Federal Reserve meeting on Wednesday, June 14, where the Fed is widely expected to leave the funds rate unchanged at the current level of 5.00%-5.25% at the conclusion of the meeting (more details below). On the inflation front, expectations are for the headline CPI number to fall from 4.9% in April to 4.1% in May, with core (ex-food and energy) inflation expected to decline from 5.5% to 5.3% over the period. As the Fed evaluates inflation and economic growth, they continue to monitor signs of continuing disinflation as input into their rate decisions for the balance of the year.

Update on the Federal Reserve (from JP Morgan): On Wednesday, the Fed should provide more clarity on the trajectory of rates after vacillation in market expectations over the past month. As of Friday, the federal funds futures market was pricing in a 28% probability of a hike in June and a 54% chance of a skip in June followed by a hike in July. Since the FOMC last met, expectations have oscillated due to resilient growth, moderating inflation, diminished threats from regional banking turmoil, a solution to the debt-ceiling standoff and mixed messages in the public pronouncements of Fed officials. Given a gradual slowdown in growth and inflation, and the fact we have yet to see the full effect of the cumulative 500bps of hikes so far, the Fed would be well advised to pause at this point. Nevertheless, another hike still is clearly on the table and, if the Fed doesn’t hike this week, Fed Chairman Jerome Powell will likely emphasize skipping a rate hike now does not necessarily imply the Fed is done raising rates. However, regardless of the Fed’s decision and messaging this week, we expect to see rate cuts within the next year that should improve the backdrop for investors across a broad range of assets.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.