Market Recap – Week Ending 06.10.22

Market Recap - Week ended June 10

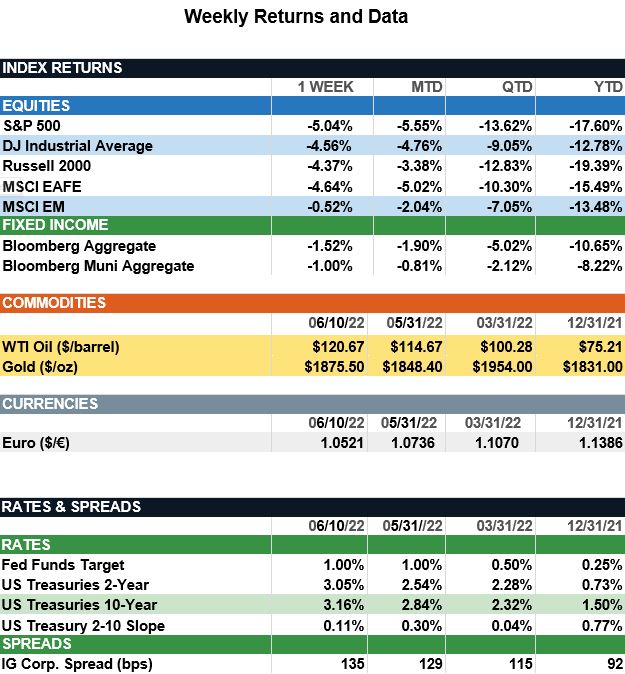

Overview: Stock market volatility continued last week as investors digested an above-consensus inflation report and upcoming monetary tightening by the Federal Reserve. Inflation and higher interest rates have been a drag on stock performance, with the S&P 500 index trading down 5.0% last week. U.S. headline consumer prices (CPI) increased 8.6% year-over-year in May, well above consensus expectations of 8.2%, and higher than April’s report of 8.3%. The increase was largely driven by housing and energy prices, and markets reacted by trading interest rates higher. In the U.S., the 10-year Treasury increased in yield by 20 basis points (0.20%) to finish the week at 3.16%. Market participants are anticipating the Federal Reserve will have to be more aggressive in raising short-rates to combat inflation. The focus this week will be on the Fed meeting Tuesday and Wednesday (June 14-15). Futures markets now are pricing in a 50-basis-point increase this week and a 75-basis-point increase at the Fed’s July meeting. The ending short funds rate now is expected to be around 3.25%, according to CME Fedwatch data.

Update on Inflation(from JP Morgan): Last Friday, the May CPI report showed inflation, as measured by the Consumer Price Index (CPI), increased 8.6% y/y. Core CPI, which excludes food and energy CPI, increased 6.0% y/y. Relative to April, Headline and Core CPI rose 1% and 0.6%, respectively. Prices continue to increase across all segments, but energy remains the biggest pain point; supply constraints and bans on Russian oil have pushed energy prices higher, with crude oil prices rising above $120/barrel last week. Given the backdrop of persistently high energy prices, it is no surprise that Energy is the only S&P 500 sector with positive year-to-date returns. This outperformance can largely be attributed to the sector’s ability to preserve profit margins. This week we highlight the “crack spread,” which is the difference between the purchase price of crude oil and the selling price of gasoline. Put differently, it is a proxy for tracking the short-term profit margins of refinery companies. The spread has trended above its three-year average since the start of the calendar year as higher oil prices, wages and transportation costs have led to an increase in the price of gasoline. Looking ahead, energy sector profitability will hinge on consumption, which has remained resilient for the time being. However, with growth slowing and the Fed becoming more hawkish, consumption may soften, particularly if unemployment rises and savings are depleted, but oil prices remain high.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s , Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.