Market Recap – Week ending June 23

Stocks See End to Five-Week Streak; PCE Price Report This Week

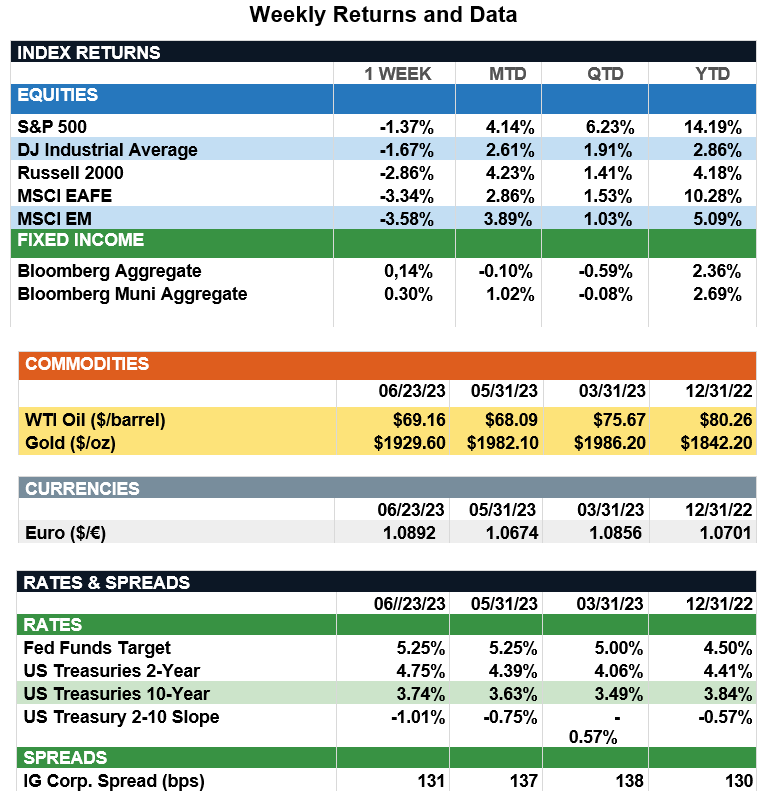

Overview: Stocks were lower last week, ending a five-week winning streak, as markets begin the last week of trading for the quarter and the month of June. In the U.S., the S&P 500 index was down 1.4% as investors brace for potentially higher interest rates from the Federal Reserve. At last week’s policy report to Congress, Fed Chair Jerome Powell noted getting inflation down to 2% “has a long way to go”, and he reiterated the Fed will continue to make its decisions “meeting by meeting.” According to the CME FedWatch tool, futures markets are currently pricing in about a 70% chance of a 25-basis-point rate hike at the upcoming July 25-26 meeting, which would move the funds rate to a range of 5.25%-5.50%. In the bond markets, interest rates were steady last week, with the 2-year and 10-year Treasury notes finishing the week at yields of 4.75% and 3.74%, respectively. Taxable and municipal bond indices inched higher on the week, and both are on track to return about 2.5% in total return over the first half of 2023. Looking forward, the final week of June is a light one for economics reports and corporate earnings. Key earnings reports will come from Walgreens on Tuesday, and Nike on Friday. Key inflation data will be reported on Friday in the form of the personal income and outlays data. Included in this report is the headline PCE Price Index, the preferred inflation gauge for the Fed, is expected to fall from 4.4% to 3.8% year-over-year, with the core PCE projected to remain steady at 4.7% annualized. Investors will also be keeping an eye on Europe and oil prices. as uncertainty around the Wagner Group rebellion in Russia will likely keep the markets on edge

Update on Economic Activity (from JP Morgan): Last week, investors parsed a slew of forward-looking data as they work to gauge the probability of a near-term recession. The Conference Board Leading Economic Index (LEI), a bellwether of economic health, took center stage and revealed a continued divergence between the economy and financial markets. The fall in the LEI index in May marked its 14th consecutive month of decline. This resulted in a six-month change of -4.3%; although not perfect, a negative reading on the LEI has been a decent signal of softer economic activity on the horizon. A closer look at the components of the index reveals consumer expectations for business conditions emerged as the largest negative contributor, followed closely by the yield curve spread. The yield curve now is as inverted as it was during the regional banking crisis, indicating elevated risk to the economy. Credit conditions aren’t expected to improve anytime soon either, as banks, particularly smaller ones, still face the risk of losing deposits and an increase in losses on their portfolio of securities as interest rates remain elevated for longer. On the flip side, building permits provided the largest positive contribution last month, spurred by a record-low supply of existing homes. However, the sustainability of this uptick can be questioned given challenges around housing affordability. With the Federal Reserve’s revised dot plot indicating two more rate hikes before the end of the year, the risk a policy error triggers a recession is looming on the horizon. As such, we continue to believe investors should focus on quality assets across both equities and fixed income, while maintaining a short-to-intermediate stance from a duration perspective.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.