Market Recap – Week Ending 06.24.22

Market Recap - Week Ending June 24

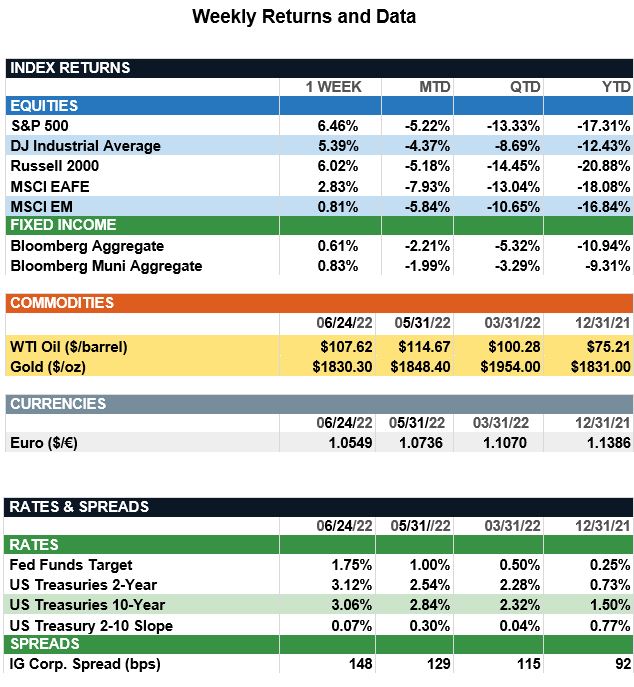

Overview: After three consecutive weeks of declines, stocks regained positive momentum last week. In the U.S., the S&P 500 index finished the week higher by 6.5%, as investors continue to monitor the effects of inflation and monetary policy on the economy. In testimony before Congress, Federal Reserve Chair Jerome Powell reiterated the Fed’s commitment to fighting inflation, while acknowledging the challenge of achieving a soft landing in the U.S. as the economy slows. On the inflation front, the personal income and outlays report scheduled to be released on Thursday will be closely watched for any signs U.S. inflation may have peaked. The report includes the Personal Consumption Expenditures (PCE) Price Index, which is the Fed’s preferred gauge for tracking inflation. The latest report for the prior month showed core PCE inflation at 4.9%; expectations for May are 4.8%. In bonds, both taxable and municipal markets recorded positive returns of 0.6% and 0.8% respectively, as Treasury yields fell. The 2-year and 10-year Treasury yields finished the week at 3.06% and 3.12%.

Economic Update (from JP Morgan): As investors mull the increasing odds of a U.S. recession, data out last week confirmed a recent weakening in the economy. The June flash PMIs showed larger-than-anticipated declines in the headline measures with many key details deteriorating. In the manufacturing survey, the headline composite fell from 57.0 in May to 52.4, with a sharp weakening in the important measures tied to new orders and output. The services sector also showed signs of softness, with the headline composite declining from 53.4 in May to 51.6, and the measure of new business dropping 7.5pts – the largest decline since the onset of the pandemic. With consumer sentiment at a record low level, these data show the economy is now seeing the impact of higher commodity prices and higher interest rates on demand. However, there are few signs of weakening in the labor market so far with initial jobless claims edging down to 229,000 over the past week. For investors, the unusual juxtaposition of pent-up demand for goods and services and excess demand for labor with a clear softening in retail sales and consumer confidence makes it very challenging to conclude if we are on the brink of a recession. However, if we are, there’s no reason to expect it will be nearly as severe as the last two. Moreover, since the economy spends the majority of the time in expansion, for long-term investors it is ultimately more important to be well-positioned for expansions than to try to tactically trade around recessions.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.