Market Recap – Week Ending 07.01.22

Market Recap - Week Ending July 1

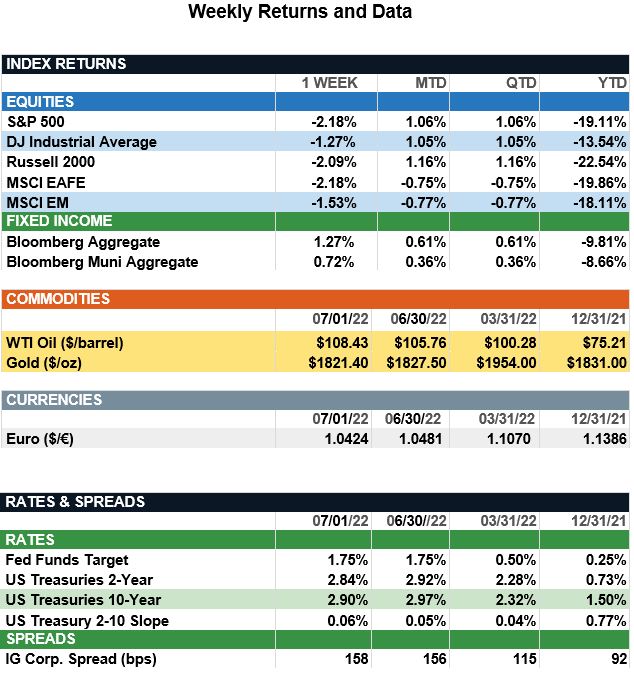

Overview: Stocks traded lower last week as concerns around economic growth remain in focus. In the U.S., the S&P 500 index fell 2.2% last week as consumer confidence fell and personal spending rose by less than consensus, pointing to decreased consumer spending as recession fears increase. On the inflation front, the core personal consumption (PCE price index) decreased to 4.7% annualized. This was the third consecutive monthly decline as investors look for signs of easing inflation. In bonds, 2-year and 10-year Treasury yields fell to 2.84% and 2.90%, respectively, leading to a solid return for taxable bonds of 1.3% for the week as inflation came in below expectations. This week, key jobs data will be reported on Friday, July 8, with new jobs projected to increase by 270,000 in June (down from 390,000 in May) and with the unemployment rate expected to remain at 3.6%.

Recap of Returns (from JP Morgan): Stock-bond correlations remained positive in 2Q22, as both equities and fixed income delivered negative returns through the end of the second quarter. Tighter monetary policy from the Federal Reserve, along with persistently high inflation, continued supply-chain bottlenecks, and the conflict in Ukraine, hurt investors across both asset classes. In contrast, commodities finished 1H22 up 18.4% due to the surge in food and energy prices. U.S. fixed income markets declined 10.3% as the Federal Reserve hiked rates by 75 basis points at its June meeting in response to the higher-than-expected inflation. Similarly, global high yield struggled during the first six months of the year, with the sector down 16.9% as corporate credit quality weakened amidst rising costs and a potential pullback in demand. Turning to equities, U.S. large and small caps decreased 20.0% and 23.4%, respectively, in 1H22 due to higher interest rates normalizing multiples and a slowdown in profit growth. In international markets, EM and DM equity decreased 17.5% and 19.3%, respectively. The conflict in Ukraine continues to weigh more heavily on the developed European markets with the region seeing significantly higher energy prices in addition to tighter monetary policy from the ECB and Bank of England. As we enter the back half of 2022, for bond investors the move higher in Treasury rates and the widening in credit spreads has led to some of the most attractive yield levels in recent history. For equity investors, the S&P 500 forward P/E ratio is now below its long-term average – potentially representing an attractive buying opportunity. However, investors should remain selective and look at companies that will be able to preserve profitability in the current macro environment, as earnings growth looks set to be the key driver of returns going forward.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.