Market Recap – Week ending July 7

Stocks, Bonds Have Negative Week; CPI Report on Wednesday

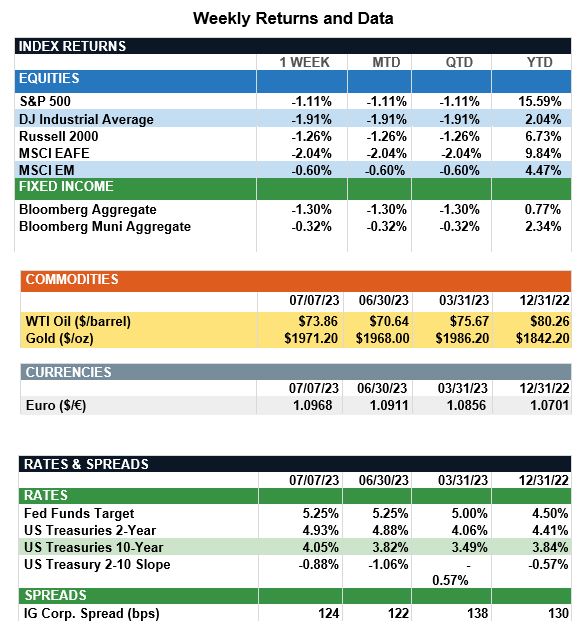

Overview: Both stocks and bonds recorded negative returns last week as investors continue to evaluate the global economic outlook. In the U.S., the ADP employment data reported an increase of 497,000 jobs in June, well above the consensus estimate of 235,000. The strong labor market has reinforced the viewpoint the Federal Reserve may have to continue to hike rates, and futures markets now are pricing in about a 90% chance of a 25-basis-point hike at the upcoming July 25-26 meeting. Notes from the June FOMC meeting reinforced this notion, referring to “unacceptably high” inflation and suggesting short rates may stay higher for longer than previously thought. On the week, the S&P 500 index fell 1.1%, and higher yields across the Treasury curve led to negative returns for bonds with the Bloomberg Aggregate index down 1.3% on the week. In economic news, the June FOMC minutes revealed Fed committee members continue to expect a U.S. recession in the latter part of 2023 or early in 2024, while stating avoiding a recession is “almost as likely as the mild recession baseline.” The Fed will continue to consider data in determining the upcoming path for interest rates, and Wednesday’s Consumer Price Index (CPI) report will be a key metric. In the upcoming report, headline inflation is expected to fall from 4.0% to 3.1% on a year-over-year basis, with core CPI (ex-food and energy) projected to decline from 5.3% to 5.0% in June on an annualized basis.

Update on Labor Markets (from JP Morgan): The U.S. economy has proven to be more resilient in the first half of 2023 (1H23) than many expected, as strength in the labor market has helped support consumption. But how much momentum does that labor market have? This week, we look to quantify labor market momentum in one number by analyzing seven key indicators: private payrolls, average hourly earnings, the U.S. Composite PMI Employment Index, the Conference Board Labor Differential Index, initial jobless claims, job openings and the unemployment rate. While the labor market remains a bright spot despite higher interest rates, it seems this part of the economy is beginning to come off the boil. Last week’s data confirmed that, while still tight by historical standards, the labor market is beginning to cool. After surging last month, JOLTS job openings fell to 9.8M, bringing the ratio of openings to unemployed workers to 1.6, its lowest level since October 2021. In contrast to this weakening signal, the quits-to-layoffs ratio rose to 2.58 on the back of rising quits. While still elevated, this is 23% below last year’s peak. Elsewhere, nonfarm payrolls rose by 209K in June, falling short of expectations and slowing compared to May. The details were a bit mixed; a tick down in the unemployment rate to 3.6% and tick up in wage growth to 4.4% highlighted continued strength, but a material downward revision to job growth in April and May, and the slowest pace of private employment gains since 2020, confirmed momentum is fading. Looking ahead, the labor market should continue to normalize, and payroll growth should moderate as labor demand cools. While this week’s data did little to change expectations for the July FOMC meeting, an increasingly balanced labor market implies slower wage growth, which should allow inflation to keep drifting lower and reduce pressure on the Fed to maintain its hawkish messaging.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.