Market Recap – Week ending July 14

Stocks Higher as CPI Falls; Earnings Reports This Week

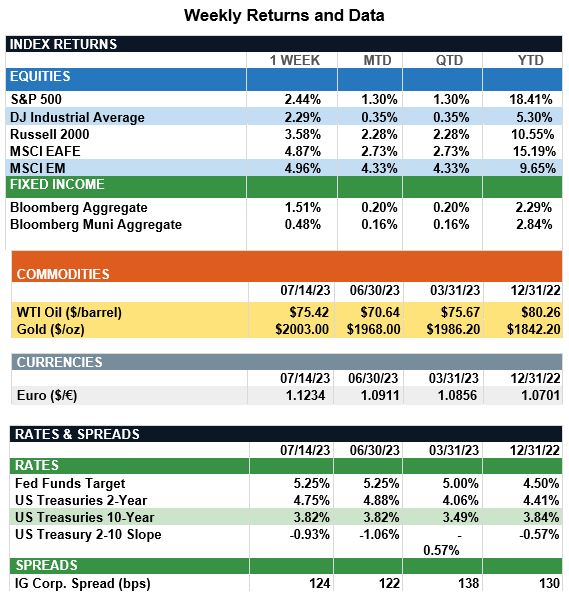

Overview: Stocks were higher around the world last week, led by emerging markets (MSCI EM) and international developed (MSCI EAFE), which rose by 4.9% and 5.0%, respectively. International stocks were aided by a weaker dollar, as the U.S. dollar depreciated 2.4% against a basket of currencies, recording a 15-month low. In the U.S., the S&P 500 index was up 2.4% as investors were encouraged by the continuation of a decline in consumer prices. U.S. core CPI fell from 5.3% in May to 4.8% in June on a year-over-year basis, led by declines in airfares, used car prices, and shelter prices. Bond markets gained as well, as improving inflation expectations led to lower yields on the week. For the week, the U.S. 2-year yield fell 0.18% to 4.75%, and the 10-year followed suit, lower in yield by 0.23% to finish the week at 3.82%. In other economic data, consumer sentiment rose for the second consecutive, reaching its highest level since September 2021. Meanwhile, the University of Michigan’s Consumer Sentiment index reported long-run inflation expectations at 3.1%, in line with market expectations. This week, earnings for the second quarter heat up, with reports from big financial institutions such as Morgan Stanley, Goldman Sachs, and Bank of America on the docket. Results also are due from the likes of Tesla, Netflix, and United Airlines, as investors evaluate corporate profits expected to decline more than 7% from a year ago, according to Factset.

Update on Global Inflation (from JP Morgan): June’s CPI report showed gathering disinflation with headline CPI rising 0.2% m/m and 3.1% y/y on a seasonally adjusted basis, well below peak inflation of 8.9% y/y a year ago. This trend is not unique to the U.S.; the OECD reported softening inflation in most major economies to 6.5% y/y in May, the lowest level for global inflation since December 2021. Overall, prices continue to soften although progress among countries remains uneven. In good news, core goods began easing late last year due to supply chain improvements, and energy followed suit as countries used strategic reserves and increased supply to compensate for Russia’s lack of production. Emerging markets, where some central banks took action early on, have had more success in bringing down core inflation and could see rate cuts this year. On the other hand, some countries in developed markets (particularly Italy) continue to battle food inflation while the rest wait for core inflation to drop further. In particular, core services prices have been slower to ease due to tight labor market conditions globally. Prices for labor-intensive services, such as medical care and education, may be softened through further monetary tightening, but others, like transportation, may stay elevated with higher rates. Those experiencing structural challenges, like the U.K. with very sticky inflation and China facing potential deflation, likely will need to fight longer to get inflation on the right path. Despite a few outliers, the global disinflation trend continues to take shape. However, with some central banks reaching the end of hiking cycles and others only beginning, investors need to pay attention to how diverging global monetary policy can affect currency dynamics and therefore international returns.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.