Market Recap - Week Ending 7.21.23

Stocks Mixed; GDP Data, Fed Meeting This Week

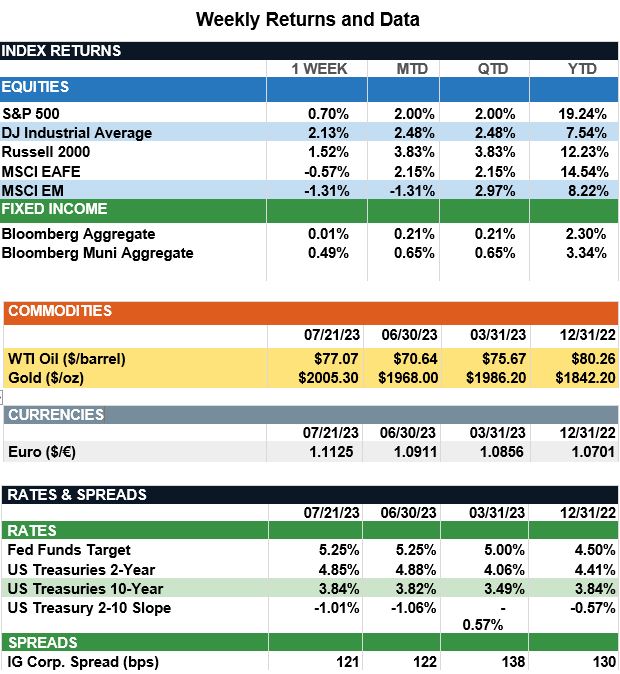

Overview: Stocks around the globe were mixed last week, as international developed stocks (MSCI EAFE) and emerging markets (MSCI EM) fell by 0.5% and 1.3%, respectively, for the week. In the U.S., the S&P 500 index ended the week 0.7% higher as investors were encouraged by a strong start to second-quarter earnings, notably in the financial sector. In bonds, the 2-year Treasury note finished 10 basis points higher in yield at 4.85%, and markets look forward to nearly universal expectations of a 0.25% rate hike at the Federal Reserve meeting ending Wednesday. The expected hike would move the funds rate to a range of 5.25% - 5.50%, with investors expecting this to be the end of the tightening cycle after the meeting this week. After the Fed meeting, focus this week will turn to the first read on second-quarter Gross Domestic Product (GDP). The consensus for GDP is currently 1.5% annualized, following the 2.0% level of the first quarter of 2023. More inflation data will come on Friday, July 28, as personal income and outlays are reported. This report includes the PCE Price Index, a key measure of inflation for the Fed. The headline PCE Price index is expected to fall from 3.8% in June to 3.0% in July, with the core PCE consensus moving from 4.6% to 4.2% for the month.

Update on the Federal Reserve (from JP Morgan): In recent weeks, markets absorbed a lot of news pertaining to both sides of the Fed’s mandate, full employment and inflation. In June, payroll job growth declined, the unemployment rate ticked down from 3.7% to 3.6% and wage growth remained at 4.4% y/y, neither adding to, nor diminishing, fears of wage inflation. Meanwhile, June retail sales data added to a picture of a resilient economy, which we expect to be confirmed by this week’s second-quarter GDP release. The other part of the Fed’s mandate, inflation, continues to decelerate, with June headline and core CPI at 3.0% and 4.8% y/y, respectively. Similarly, Federal Reserve Chair Jerome Powell’s preferred measure, super-core inflation, fell to its lowest level since September 2021. While both parts of the Fed’s mandate continue to trend in the right direction, we expect the Fed to hike another 25bps on Wednesday. The market clearly agrees and is pricing in a 96% probability of a hike. Regardless, the end of the Fed hiking cycle looks closer than it did earlier this year, as the market expects no further hikes for the remainder of the year assuming we get a hike Wednesday. However, the market appears too pessimistic in its outlook for rate cuts with only one full cut expected in 1Q24 and a cumulative 125bps for the year. The Fed often raises rates on an escalator, before being forced to take an elevator down, with rates falling on average 275bps within the first year of cuts. As rates move lower, the investment climate becomes more appealing for all long-term asset classes. Investors may want to extend fixed-income duration as expectations for policy rates in 2024 and 2025 may be too high given a softening in growth momentum and rapid decline in inflation.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.