Market Recap – Week Ending July 22

Market Recap – Week ending July 22

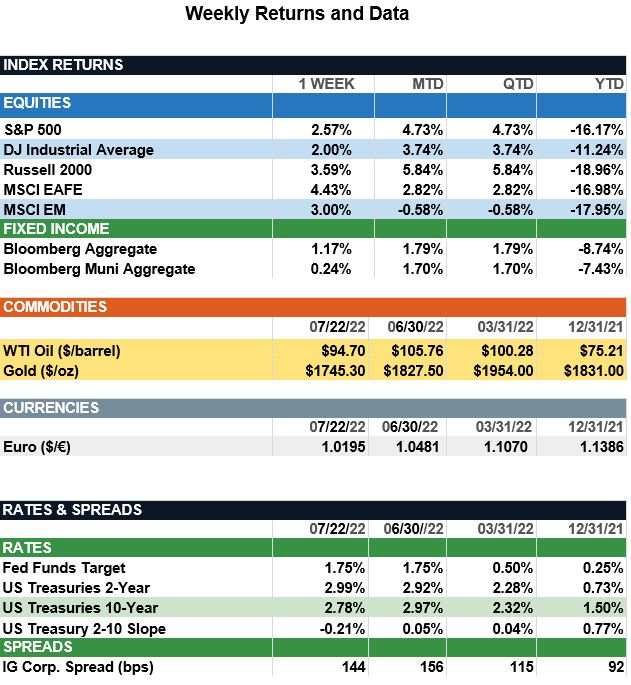

Overview: Global stocks ended last week in positive territory, as better-than-expected corporate earnings in the U.S. aided consumer optimism despite economic and interest-rate pressures. In the U.S., the S&P 500 rose 2.6%, while international developed stocks (MSCI EAFE) and emerging markets (MSCI EM) were up 4.4% and 3.0%, respectively. In bonds, U.S. Treasury yields fell last week as investors assessed ongoing expectations for Federal Reserve policy, economic growth, and inflation. The 10-Year U.S. Treasury yield was lower by 15 basis points (0.15%) on the week, ending at 2.78%, and the 2-Year yield fell a similar amount to 2.99%. In economic news, the European Central Bank (ECB) surprised the market with a 50-basis-point rate hike and unveiled details of a new financial protection program. Attention this week in the U.S. will be on the July 26-27 Federal Reserve meeting, where the Fed is widely expected to raise short rates by 75 basis points and continue guidance to aggressively fight inflation. The first look at second-quarter Gross Domestic Product (GDP) will come on Thursday, with the consensus expectation for a 0.5% growth rate, after the -1.6% reading from the first quarter of 2022.

Update on Earnings (from JP Morgan): Despite the higher costs and decline in consumer sentiment, 2Q22 operating margins have remained resilient and currently are sitting at 12.8%, above the historical average of 9.9%. With 22.9% of the market reporting, our current estimate for Q2 2022 S&P 500 operating earnings per share (EPS) is $54.28 ($46.59 ex-financials). If realized, this would represent y/y growth of 4.3% and q/q growth of 10.0%. At the sector level, estimates are pointing toward sizeable growth in earnings among the energy, materials and industrials sectors. This is unsurprising given all three sectors are highly cyclical and directly benefit from the surge in prices we saw in 1H22. Last week, we had a glimpse into how earnings within industrials may fare, with U.S. airlines releasing earnings. Results were positive, as many airlines beat profit estimates on the back of stronger-than-expected demand even amid higher ticket prices and an uptick in flight disruptions. Additionally, while guidance for 2022 was revised downward for the industry, management teams noted they still expect to record a profit in the coming quarters. Unlike its cyclical counterparts, financials are having a tough quarter, with operating earnings projected to contract 39% y/y. The decline can be primarily attributed to a build-up of loan loss reserves, a fall in investment banking activity and a slowdown in mortgage fees. These pressures have been partially offset by solid net interest income growth, higher card spending and strong trading revenue. Despite these higher costs and decline in consumer sentiment, 2Q22 operating margins have remained resilient at 12.8%, above their long-run average of 9.9%. While many companies are yet to report, this could be a signal that corporate profits may not be as weak as recent headlines suggest.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.