Market Recap - Week Ending 7.28.23

Stocks Rally After Earnings Reports, GDP News

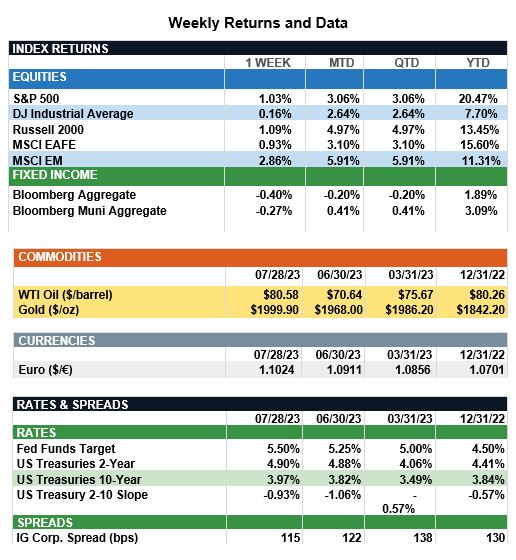

Overview: Global stocks rose last week as investors anticipate the end of tightening cycles in both the U.S. and Europe. In the U.S., as widely expected, the Federal Open Market Committee (FOMC) increased the federal funds rate to a range of 5.25%-5.50%, the highest level in more than 20 years (see details below). Market participants now are hopeful rate hikes are done for this cycle, as Federal Reserve Chair Jerome Powell mentioned in the ensuing news conference the Fed would prefer a “careful pace” going forward. Here in the U.S., the S&P 500 index finished the week 1.0% higher as markets rallied on better-than-expected earnings and a strong gross domestic product (GDP) report. U.S. second-quarter GDP rose 2.4%, driven by stronger-than-expected consumption and increased business investment. In the bond markets, yields rose, with the 10-year Treasury ending the week 0.13% higher at a yield of 3.97%. Looking ahead, any further rate hikes will be data-dependent, and growth and inflation numbers will be closely monitored. There was good news last week on the inflation front as the core PCE Index fell to 4.1% in June from 4.6% in May. As JP Morgan notes in the following section, the next Fed meeting will not occur until later in September, with data such as the July and August consumer price index (CPI) reports critical to monitoring the ongoing progress in reducing inflation.

Update on the Economy and Inflation (from JP Morgan): At their July meeting, the Fed hiked rates by 25bps, as widely expected, to a range of 5.25%-5.50% and delivered somewhat dovish messaging. While statement language kept the door open for further rate hikes, commentary from Fed Chairman Powell emphasized continued data dependency in policy decisions. In reviewing such data, last week’s releases painted a fairly rosy picture of an economy showing resiliency in economic growth and labor markets even as inflation declines further. The first estimate of 2Q23 GDP showed the economy grew at a better-than-expected 2.4% annualized rate, reflecting strength in consumption and the best pace of business fixed investment since 1Q22, rising 7.7%. PCE data also confirmed further progress on disinflation. Chairman Powell’s focus measure of inflation, core services ex-housing PCE, rose a modest 0.24% in June, a notable downshift from the 0.44% average rate in the previous three months. Elsewhere, unemployment claims remain low and strong durable goods orders point to continued consumer and business demand. Going forward, the Fed is likely to focus on inflation, with the July and August CPI reports playing a decisive role in their September decision. Powell also made specific mention of the Employment Cost Index (ECI), which may offer a clearer picture of wage gains relative to the BLS report, as it tracks the same jobs over time. The ECI rose 1.0% in the second quarter, marking the slowest quarterly pace in two years. Mounting evidence of a sustained disinflation trend could potentially give the Fed confidence to pause rate hikes in September. Meanwhile, investors are increasingly looking beyond incremental Fed tightening, with markets appearing relatively unfazed by the Fed meeting last week.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.