Market Recap – Week ending Aug. 4

S&P 500 Positive Streak Ends; CPI Report This Week

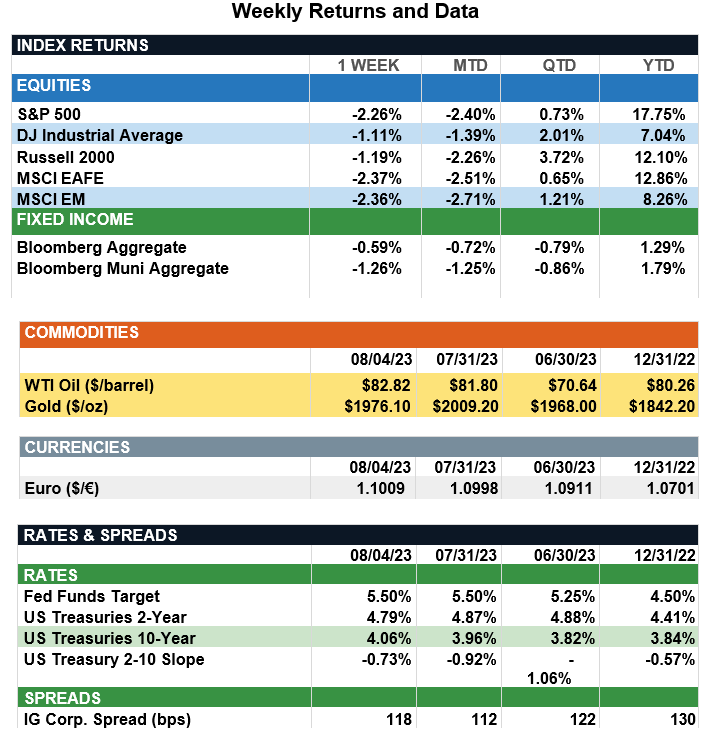

Overview: Stocks were lower across the globe last week as markets reacted to the downgrade of the United States’ long-term credit rating to AA+ from AAA by the rating agency Fitch. In the U.S., the S&P 500 ended a three-week streak of positive returns and finished the week lower by 2.3%. In the bond markets, yields rose in response to the credit downgrade with the 10-year Treasury finishing the week at a yield of 4.06%, its highest level in nine months. Oil prices rose, as well, as strong demand and tightening supply sent the benchmark WTI crude price to $82.82 per barrel, the highest level since May 2023. A bright spot for the markets has been earnings. With 84% of S&P 500 companies reporting second-quarter earnings through Aug. 4, 79% of companies have reported earnings above consensus expectations (Factset). In economic data, the monthly employment report from the Bureau of Labor showed the U.S. economy created 187,000 new jobs in July, below the consensus expectation for a 200,000 increase but the 31st consecutive month of job increases for the economy. The unemployment rate declined from 3.6% to 3.5%, near a historic low. This week, the market focus will be on the consumer prices (CPI) report due out on Thursday, Aug. 10. Expectations are for headline CPI to rise modestly from 3.0% to 3.3% annualized, with the core CPI expected to remain at 4.8%.

Update on Employment (from JP Morgan): Last week's employment report painted a nuanced picture of the labor market. While job openings and payroll gains came in below expectations, wage growth surprised slightly to the upside. This prompts the question: Will wages revert to their previous easing trend? The answer may hinge on how corporations react to the evolving macroeconomic environment. As the 2Q23 earnings season draws to a close, a trend emerged – more than 70% of companies have beaten earnings estimates despite softer revenues. In the face of input cost inflation, companies had been raising prices in an effort to pass along these costs and defend margins. However, the landscape is shifting. As inflation eases further, companies will see pricing power wane, and therefore be forced to embrace layoffs and cost-cutting to protect margins. This dynamic should support softer wage growth and ensure continued moderation in the labor market more broadly. IT already has seen significant moderation in wage growth due to layoffs last year. Other service-related industries also have seen wages cool. However, the impact on goods-producing industries and trade, transport, and utilities could well lag due to still-high job opening rates and more unionization. Considering Federal Reserve Chairman Jerome Powell’s recent comment, the FOMC may not need to wait for inflation to return to 2% to cut rates, a less robust environment for wages should allow the Fed to pause, and eventually cut, rates next year. Importantly, although the path to a soft landing is increasingly visible, history reminds us that soft landings are rare. What remains certain is the timeline to add duration has been extended given the recent back-up in rates; investors should take advantage of this and embrace higher-quality sectors of the fixed-income universe as they prepare for lower inflation and softer growth next year.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.