Market Recap – Week Ending August 5

Market Recap - Week Ending August 5

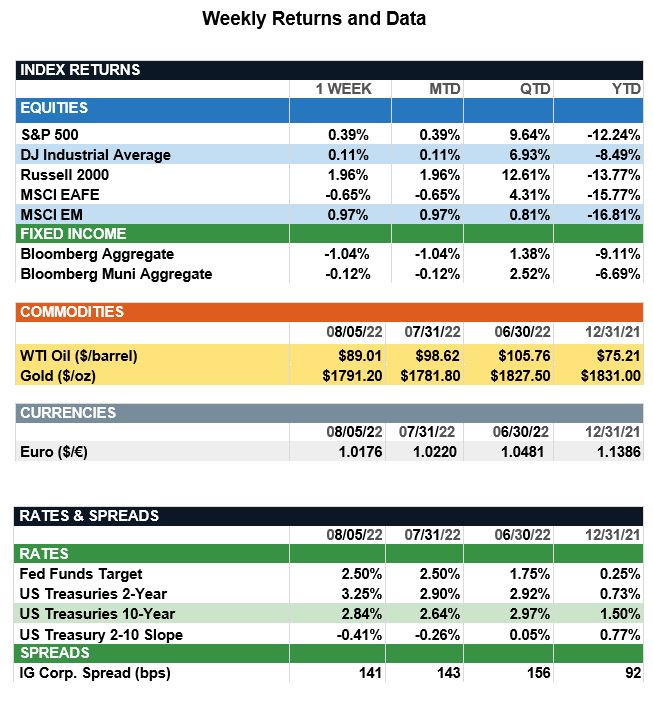

Overview: Stocks finished close to unchanged last week in a choppy trade week as investors faced rising U.S.-China tensions and the prospect of continued rate hikes from the Federal Reserve. In the U.S., the S&P 500 index finished the week 0.4% higher while international stocks (MSCI EAFE) were lower by 0.7%. Bond yields were sharply higher on the week, as a strong jobs report eased recession fears but suggested the Fed will need to continue to raise short-term funds rates. According to Fed Watch data, futures markets now are pricing in about a 70% probability of a 0.75% (75 basis point) rate hike at the Fed meeting next month. On the week, the 2-year and 10-year Treasury notes rose in yield 0.35% and 0.20%, respectively, as markets adjusted to expectations of higher short-term rates. In economic data, the employment report for July showed nonfarm payrolls in the U.S. rose 528,000 in July, more than double consensus expectations. Meanwhile, the unemployment rate dropped from 3.6%o 3.5%, a pre-pandemic low. This week, focus will be on the consumer prices (CPI) report due out Wednesday, where the expectations are for headline CPI to be 8.7% year-over-year for July, down from 9.1% in the previous month.

Update on the Labor Market (from JP Morgan): Following a series of disappointing economic data releases, including a second-consecutive negative quarter of GDP growth, the July jobs report blew past expectations and underscored the economy still has strong demand for labor and tight supply, which is pushing wages higher. Notably, the labor market now has hit two milestones, having recovered all the payroll jobs lost in the pandemic recession and achieving the lowest unemployment rate (3.46% to two decimals) since May 1969. Job gains were very widespread across industries with the bulk of gains in services. Surprisingly, job growth also accelerated in cyclical sectors such as construction and manufacturing, where activity data has weakened recently. Wages rose a strong 0.5% for all workers with slight upward revisions to recent months, suggesting employees continue to have considerable bargaining power. Apart from this report, there still are signs in the economy that the huge excess demand for labor is easing. JOLTS job openings have fallen in recent months and unemployment claims have been slowly rising since the middle of March. Moreover, the economy still is facing plenty of drags on growth in the second half of the year. Still, the booming jobs report does provide strong support to Fed Chairman Jerome Powell’s assertion the economy is not currently in recession, and we will need to see a softening in inflation data over the next few CPI reports (which we expect to happen) for the Fed to dial back its aggressive rate-hiking path.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.