Market Recap – Week ending Aug. 11

Global Stocks Lower; CPI Below Consensus Expectations

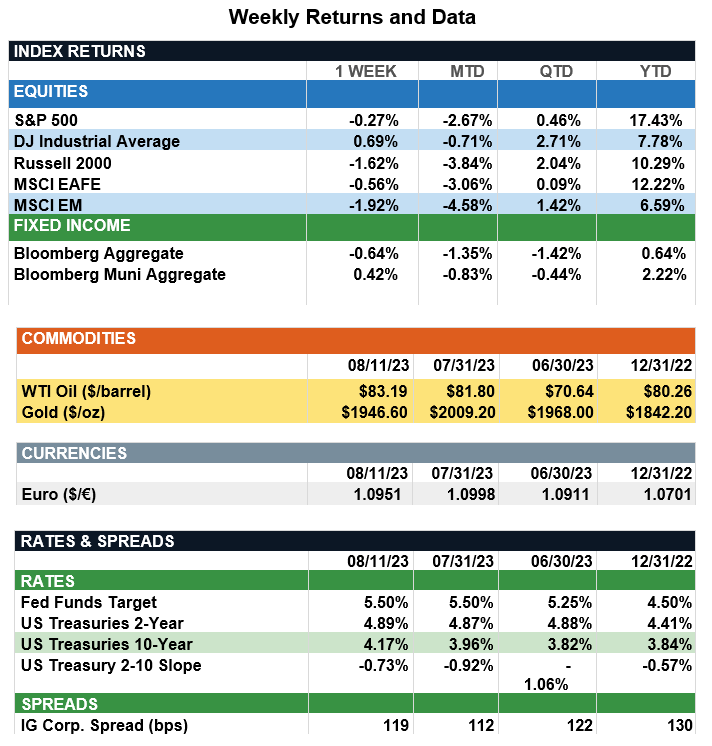

Overview: Global stocks were marginally lower last week as optimism over disinflation was offset by worries the economy may not be slowing at the Federal Reserve’s desired pace. To wit, the latest estimate from the Atlanta Fed’s GDPNow metric forecasts a growth of 4.1% for third-quarter GDP, reflecting such factors as ongoing labor strength and an increase in estimated domestic income growth. For the week, the S&P 500 index was down 0.3% as interest rates rose, with the 2-year and 10-year Treasury notes finishing the week at 4.89% and 4.17%, respectively. On the inflation front, year-over-year headline and core consumer prices (CPI) figures were 3.2% and 4.7%, respectively, each below consensus expectations. The CPI report showed continued disinflation in the markets, especially with the core inflation showing a decline. An ongoing concern for the Fed is shelter costs, which contributed to virtually all of the increase in July CPI. With an off month in August, the Fed will be carefully evaluating economic data between now and the next policy announcement on Sept. 20. There is good reason to believe the full impact of higher interest rates have yet to flow through the economy, and in our view, it would take a sharp reversal in the current disinflationary trends for the Fed to move forward with any further rate increases.

Update on Valuations and Returns (from JP Morgan): As of last Friday’s market close, the top 10 stocks in the S&P 500 accounted for 90% of the index’s year-to-date gains. While market breath has been narrow, and returns have been highly concentrated, the rally has broadened out relative to May when the S&P 500’s 10 largest names accounted for all of the year-to-date gains. This decline in concentration can be attributed to surprisingly resilient economic data, which in turn has fueled better-than-expected profit growth and stock market performance. In fact, with the 2Q23 earnings season coming to a close, profits have surprised to the upside with particular strength in the consumer sectors, construction, travel and streaming/gaming. With that being said, the recent broadening has been moderate, at best, and mega-cap tech stock valuations remain stretched. The top 10 stocks currently account for more than 30% of the index, which is down from the peak levels we saw in April/May but still extremely high relative to the last 25 years. Importantly, and in contrast to their weight in the index, the earnings contribution of these top 10 stocks is sitting near its pre-COVID level, but well below the pandemic era highs. Despite this misalignment in weights and earnings, the VIX has remained at historically low levels, which has been aided by the market becoming increasingly confident in a soft landing. Whether this performance is sustainable hinges on inflation. Any further stickiness in core CPI may push the Fed to maintain a hawkish stance, thereby increasing the odds of a recession. In such a scenario, we would likely see earnings revised lower, leaving the market, where valuations are already stretched, particularly vulnerable. As such, investors should take advantage of historically wide valuation dispersion, and focus on low beta stocks characterized by stable cash flows and solid balance sheets.

Sources: JP Morgan Asset Management, Goldman Sachs Asset Management, Barron’s, Bloomberg

This communication is for informational purposes only. It is not intended as investment advice or an offer or solicitation for the purchase or sale of any financial instrument.

Indices are unmanaged, represent past performance, do not incur fees or expenses, and cannot be invested into directly. Past performance is no guarantee of future results.